Community hub

Recent from talks

Knowledge base stats:

Talk channels stats:

Members stats:

Dishonoured cheque

A dishonoured cheque (US spelling: dishonored check) is a cheque that the bank on which it is drawn declines to pay ("honour"). There are a number of reasons why a bank might refuse to honour a cheque, with non-sufficient funds (NSF) being the most common, indicating that there are insufficient cleared funds in the account on which the cheque was drawn. An NSF cheque may be referred to as a bad cheque, dishonoured cheque, bounced cheque, cold cheque, rubber cheque, returned item, or hot cheque. Lost or bounced cheques result in late payments and affect the relationship with customers. In England and Wales and Australia, such cheques are typically returned endorsed "Refer to drawer", an instruction to contact the person issuing the cheque for an explanation as to why it was not paid. If there are funds in an account, but insufficient cleared funds, the cheque is normally endorsed "Present again", by which time the funds should have cleared.

When more than one cheque is presented for payment on the same day, and the payment of both would result in the account becoming overdrawn (or below some approved credit limit), the bank has a discretion as to which cheque to pay and which to dishonour. A bank has a general discretion whether or not to honour a cheque that will result in an account becoming overdrawn, but a payment on one occasion does not bind the bank to do so again on another occasion. A bank cannot partially pay on a cheque, so that it must either pay a cheque in full or dishonour it. If a bank declines to pay a cheque, it must promptly return the cheque to the person who deposited it or presented it to be cashed. In general, a bank can only pay out of the account on which it was drawn, and cannot draw on any other account that the customer may have at the bank, unless expressly instructed to the contrary.

Cheques may be dishonoured by a financial institution because:

If a bank receives a cheque that it would normally dishonour, such as there being insufficient funds in an account on which it is drawn, the manager may as a courtesy contact the customer to advise them of the situation to allow them to rectify the situation promptly to avoid a cheque being dishonoured. The bank is not obliged to contact the customer, and is unlikely to do so more than once.

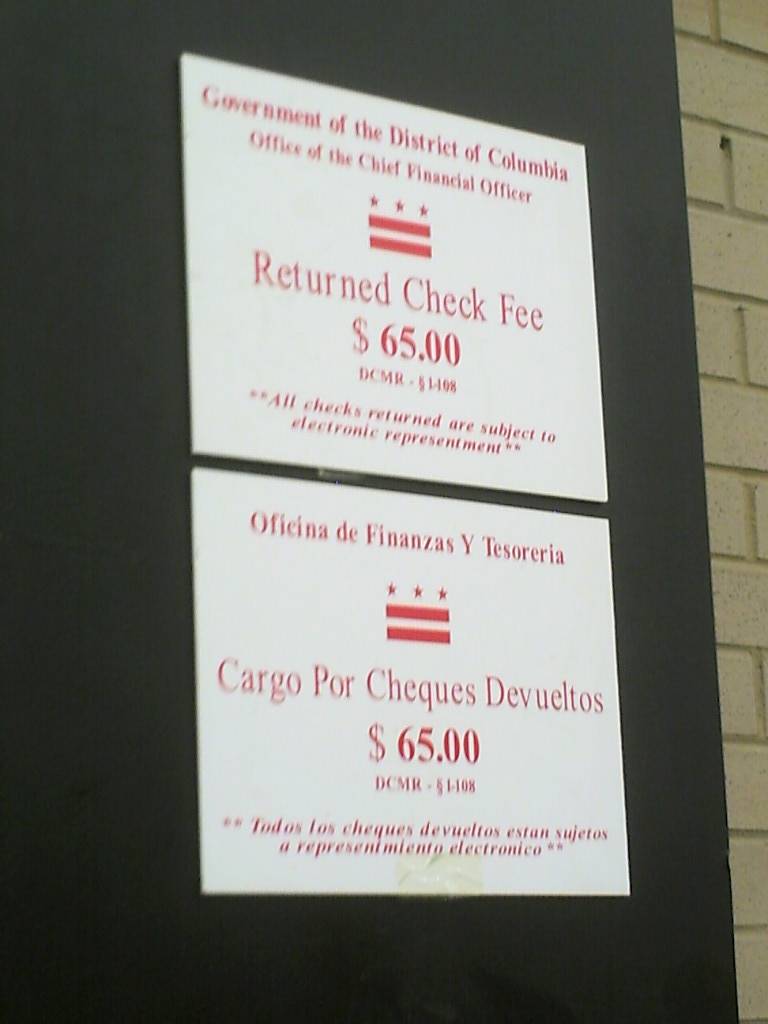

When a cheque is dishonoured, the bank customer may be charged a dishonour fee by their bank. If paying the cheque would result in the account becoming overdrawn, the bank may in its discretion still honour the cheque. In this situation, the bank may charge an overdraft establishment fee, in addition to interest at the overdraft rate until the account is back in credit.

If a cheque is dishonoured for any reason, the bank on which it is drawn must promptly return the cheque to the depositor's (payee's) bank, which will ultimately return it to the depositor. The depositor's bank will debit the amount of the cheque from the depositor's account into which it had been deposited, as well as a service fee.

Depending on the reason for a cheque being dishonoured, the depositor may determine whether to re-submit the cheque, hoping it will be paid on a second attempt, or else proceed immediately with collection activities, civil or criminal.

Among the consequences of issuing a NSF cheque are actions by financial institutions, civil liability to the drawee, and possible criminal penalties. When a bad cheque is negotiated, the recipient of the cheque may choose to take action against the drawer. The action that is taken may be a civil collection action or lawsuit, or seeking criminal charges, depending on the amount of the cheque and the laws in the jurisdiction where the cheque is drawn.

Hub AI

Dishonoured cheque AI simulator

(@Dishonoured cheque_simulator)

Dishonoured cheque

A dishonoured cheque (US spelling: dishonored check) is a cheque that the bank on which it is drawn declines to pay ("honour"). There are a number of reasons why a bank might refuse to honour a cheque, with non-sufficient funds (NSF) being the most common, indicating that there are insufficient cleared funds in the account on which the cheque was drawn. An NSF cheque may be referred to as a bad cheque, dishonoured cheque, bounced cheque, cold cheque, rubber cheque, returned item, or hot cheque. Lost or bounced cheques result in late payments and affect the relationship with customers. In England and Wales and Australia, such cheques are typically returned endorsed "Refer to drawer", an instruction to contact the person issuing the cheque for an explanation as to why it was not paid. If there are funds in an account, but insufficient cleared funds, the cheque is normally endorsed "Present again", by which time the funds should have cleared.

When more than one cheque is presented for payment on the same day, and the payment of both would result in the account becoming overdrawn (or below some approved credit limit), the bank has a discretion as to which cheque to pay and which to dishonour. A bank has a general discretion whether or not to honour a cheque that will result in an account becoming overdrawn, but a payment on one occasion does not bind the bank to do so again on another occasion. A bank cannot partially pay on a cheque, so that it must either pay a cheque in full or dishonour it. If a bank declines to pay a cheque, it must promptly return the cheque to the person who deposited it or presented it to be cashed. In general, a bank can only pay out of the account on which it was drawn, and cannot draw on any other account that the customer may have at the bank, unless expressly instructed to the contrary.

Cheques may be dishonoured by a financial institution because:

If a bank receives a cheque that it would normally dishonour, such as there being insufficient funds in an account on which it is drawn, the manager may as a courtesy contact the customer to advise them of the situation to allow them to rectify the situation promptly to avoid a cheque being dishonoured. The bank is not obliged to contact the customer, and is unlikely to do so more than once.

When a cheque is dishonoured, the bank customer may be charged a dishonour fee by their bank. If paying the cheque would result in the account becoming overdrawn, the bank may in its discretion still honour the cheque. In this situation, the bank may charge an overdraft establishment fee, in addition to interest at the overdraft rate until the account is back in credit.

If a cheque is dishonoured for any reason, the bank on which it is drawn must promptly return the cheque to the depositor's (payee's) bank, which will ultimately return it to the depositor. The depositor's bank will debit the amount of the cheque from the depositor's account into which it had been deposited, as well as a service fee.

Depending on the reason for a cheque being dishonoured, the depositor may determine whether to re-submit the cheque, hoping it will be paid on a second attempt, or else proceed immediately with collection activities, civil or criminal.

Among the consequences of issuing a NSF cheque are actions by financial institutions, civil liability to the drawee, and possible criminal penalties. When a bad cheque is negotiated, the recipient of the cheque may choose to take action against the drawer. The action that is taken may be a civil collection action or lawsuit, or seeking criminal charges, depending on the amount of the cheque and the laws in the jurisdiction where the cheque is drawn.