Community hub

Recent from talks

Knowledge base stats:

Talk channels stats:

Members stats:

European Union value added tax

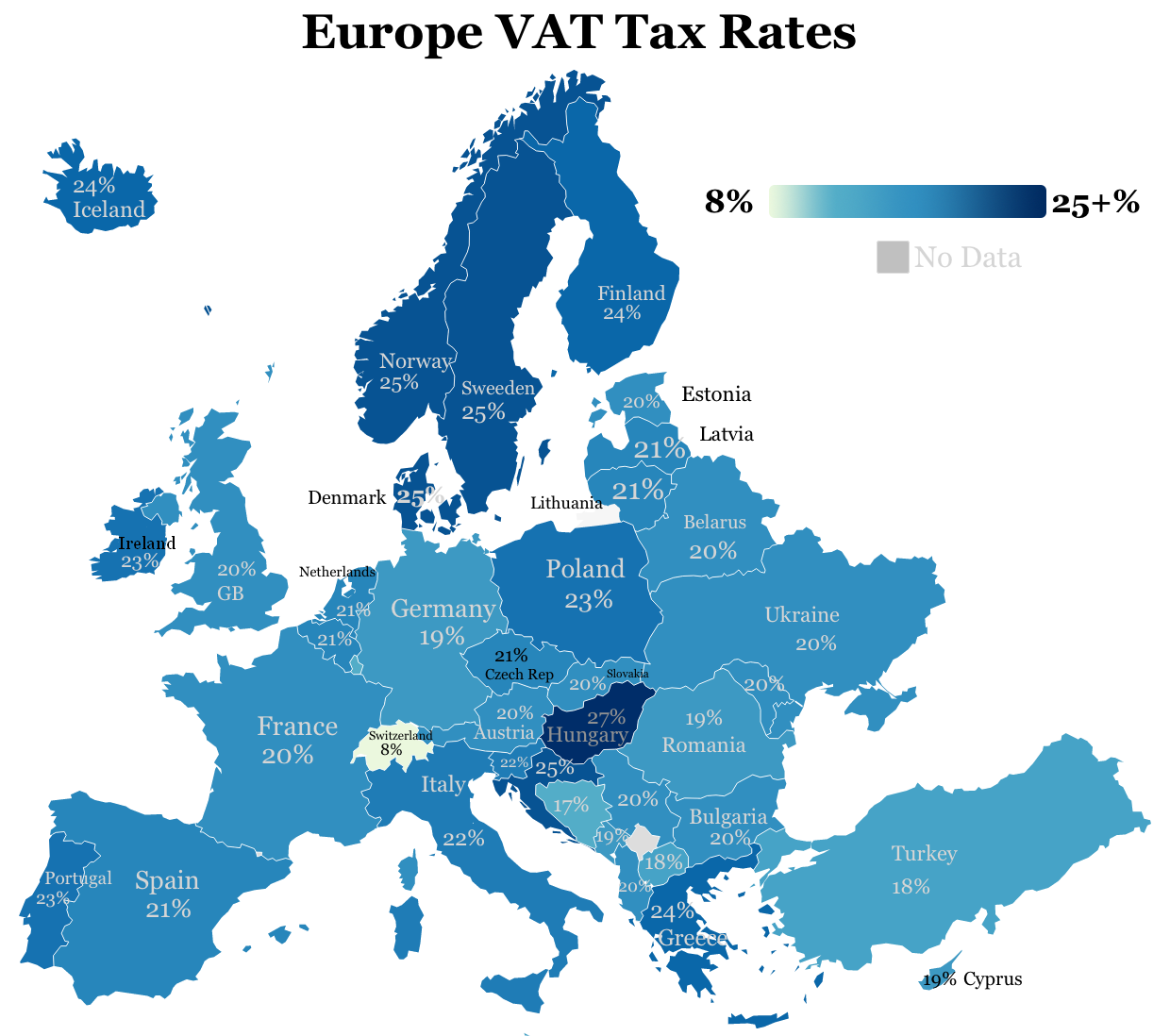

The European Union value-added tax (or EU VAT) is a value added tax on goods and services within the European Union (EU). The EU's institutions do not collect the tax, but EU member states are each required to adopt in national legislation a value added tax that complies with the EU VAT code. Different rates of VAT apply in different EU member states, ranging from 17% in Luxembourg to 27% in Hungary. The total VAT collected by member states is used as part of the calculation to determine what each state contributes to the EU's budget.

German industrialist Wilhelm von Siemens proposed the concept of a value-added tax in 1918 to replace the German turnover tax however, the turnover tax was not replaced until 1968. The modern variation of VAT was first implemented by Maurice Lauré, joint director of the French tax authority, who implemented VAT on 10 April 1954 in France's Ivory Coast colony. Assessing the experiment as successful, France introduced it domestically in 1958.

Following creation of the European Economic Community in 1958, the Fiscal and Financial Committee set up by the European Commission in 1960 under the chairmanship of Professor Fritz Neumark made its priority objective the elimination of distortions to competition caused by disparities in national indirect tax systems.

The Neumark Report published in 1962 concluded that France's VAT model would be the simplest and most effective indirect tax system. This led to the EEC issuing two VAT directives, adopted in April 1967, providing a blueprint for introducing VAT across the EEC, following which, other member states (initially Belgium, Italy, Luxembourg, the Netherlands and West Germany) introduced VAT.

The First Directive was concerned with harmonising the legislation of the member states with respect to turnover taxes. This act was to replace the multi-level cumulative indirect taxation system in the EU member states by simplifying tax calculations and neutralising the indirect taxation factor in relation to competition in the EU.

The EU value-added tax is based on the "destination principle": the value-added tax is paid to the government of the country in which the consumer who buys the product lives. Businesses selling a product charge the VAT and the customer pays it. When the customer is a business, the VAT is known as an "input VAT." When a consumer purchases the end product from a business, the tax is called the "output VAT."

A value-added tax collected at each stage in the supply chain is remitted to the tax authorities of the member state concerned and forms part of that state's revenue. A small proportion goes to the European Union in the form of a levy ("VAT-based own resources").

The co-ordinated administration of value-added tax within the EU VAT area is an important part of the single market. A cross-border VAT is declared in the same way as domestic VAT, which facilitates the elimination of border controls between member states, saving costs and reducing delays. It also simplifies administrative work for freight forwarders. Previously, in spite of the customs union, the differing VAT rates and the separate VAT administration processes resulted in a high administrative and cost burden for cross-border trade.

Hub AI

European Union value added tax AI simulator

(@European Union value added tax_simulator)

European Union value added tax

The European Union value-added tax (or EU VAT) is a value added tax on goods and services within the European Union (EU). The EU's institutions do not collect the tax, but EU member states are each required to adopt in national legislation a value added tax that complies with the EU VAT code. Different rates of VAT apply in different EU member states, ranging from 17% in Luxembourg to 27% in Hungary. The total VAT collected by member states is used as part of the calculation to determine what each state contributes to the EU's budget.

German industrialist Wilhelm von Siemens proposed the concept of a value-added tax in 1918 to replace the German turnover tax however, the turnover tax was not replaced until 1968. The modern variation of VAT was first implemented by Maurice Lauré, joint director of the French tax authority, who implemented VAT on 10 April 1954 in France's Ivory Coast colony. Assessing the experiment as successful, France introduced it domestically in 1958.

Following creation of the European Economic Community in 1958, the Fiscal and Financial Committee set up by the European Commission in 1960 under the chairmanship of Professor Fritz Neumark made its priority objective the elimination of distortions to competition caused by disparities in national indirect tax systems.

The Neumark Report published in 1962 concluded that France's VAT model would be the simplest and most effective indirect tax system. This led to the EEC issuing two VAT directives, adopted in April 1967, providing a blueprint for introducing VAT across the EEC, following which, other member states (initially Belgium, Italy, Luxembourg, the Netherlands and West Germany) introduced VAT.

The First Directive was concerned with harmonising the legislation of the member states with respect to turnover taxes. This act was to replace the multi-level cumulative indirect taxation system in the EU member states by simplifying tax calculations and neutralising the indirect taxation factor in relation to competition in the EU.

The EU value-added tax is based on the "destination principle": the value-added tax is paid to the government of the country in which the consumer who buys the product lives. Businesses selling a product charge the VAT and the customer pays it. When the customer is a business, the VAT is known as an "input VAT." When a consumer purchases the end product from a business, the tax is called the "output VAT."

A value-added tax collected at each stage in the supply chain is remitted to the tax authorities of the member state concerned and forms part of that state's revenue. A small proportion goes to the European Union in the form of a levy ("VAT-based own resources").

The co-ordinated administration of value-added tax within the EU VAT area is an important part of the single market. A cross-border VAT is declared in the same way as domestic VAT, which facilitates the elimination of border controls between member states, saving costs and reducing delays. It also simplifies administrative work for freight forwarders. Previously, in spite of the customs union, the differing VAT rates and the separate VAT administration processes resulted in a high administrative and cost burden for cross-border trade.