Community hub

Recent from talks

Knowledge base stats:

Talk channels stats:

Members stats:

Credit default swap

A credit default swap (CDS) is a financial swap agreement that the seller of the CDS will compensate the buyer in the event of a debt default (by the debtor) or other credit event. That is, the seller of the CDS insures the buyer against some reference asset defaulting. The buyer of the CDS makes a series of payments (the CDS "fee" or "spread") to the seller and, in exchange, may expect to receive a payoff if the asset defaults.

In the event of default, the buyer of the credit default swap receives compensation (usually the face value of the loan), and the seller of the CDS takes possession of the defaulted loan or its market value in cash. However, anyone can purchase a CDS, even buyers who do not hold the loan instrument and who have no direct insurable interest in the loan (these are called "naked" CDSs). If there are more CDS contracts outstanding than bonds in existence, a protocol exists to hold a credit event auction. The payment received is often substantially less than the face value of the loan.

Credit default swaps in their current form [vague] have existed since the early 1990s and increased in use in the early 2000s. [citation needed] By the end of 2007, the outstanding CDS amount was $62.2 trillion, falling to $26.3 trillion by mid-year 2010 and reportedly $25.5 trillion in early 2012.

As of 2009, CDSs were not traded on an exchange and there was no required reporting of transactions to a government agency.

During the 2008 financial crisis, the lack of transparency in this large market became a concern to regulators as it could pose a systemic risk. In March 2010, the Depository Trust & Clearing Corporation (see Sources of Market Data) announced it would give regulators greater access to its credit default swaps database. There was "$8 trillion notional value outstanding" as of June 2018.

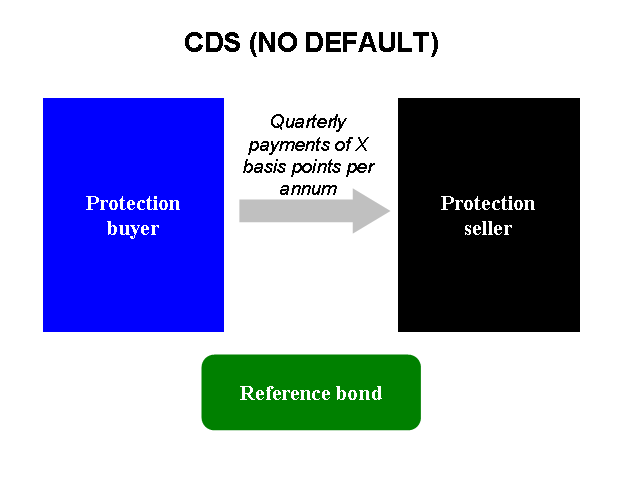

A "credit default swap" (CDS) is a credit derivative contract between two counterparties. The buyer makes periodic payments to the seller, and in return receives a payoff if an underlying financial instrument defaults or experiences a similar credit event.

The CDS may refer to a specified loan or bond obligation of a "reference entity", usually a corporation or government. The reference entity is not a party to the contract. The buyer makes regular premium payments to the seller, the premium amounts constituting the "spread" charged in basis points by the seller to insure against a credit event. If the reference entity defaults, the protection seller pays the buyer the par value of the bond in exchange for physical delivery of the bond, although settlement may also be by cash or auction.

A default is often referred to as a "credit event" and includes such events as failure to pay, restructuring and bankruptcy, or even a drop in the borrower's credit rating. CDS contracts on sovereign obligations also usually include as credit events repudiation, moratorium, and acceleration. Most CDSs are in the $10–$20 million range with maturities between one and 10 years. Five years is the most typical maturity.

Hub AI

Credit default swap AI simulator

(@Credit default swap_simulator)

Credit default swap

A credit default swap (CDS) is a financial swap agreement that the seller of the CDS will compensate the buyer in the event of a debt default (by the debtor) or other credit event. That is, the seller of the CDS insures the buyer against some reference asset defaulting. The buyer of the CDS makes a series of payments (the CDS "fee" or "spread") to the seller and, in exchange, may expect to receive a payoff if the asset defaults.

In the event of default, the buyer of the credit default swap receives compensation (usually the face value of the loan), and the seller of the CDS takes possession of the defaulted loan or its market value in cash. However, anyone can purchase a CDS, even buyers who do not hold the loan instrument and who have no direct insurable interest in the loan (these are called "naked" CDSs). If there are more CDS contracts outstanding than bonds in existence, a protocol exists to hold a credit event auction. The payment received is often substantially less than the face value of the loan.

Credit default swaps in their current form [vague] have existed since the early 1990s and increased in use in the early 2000s. [citation needed] By the end of 2007, the outstanding CDS amount was $62.2 trillion, falling to $26.3 trillion by mid-year 2010 and reportedly $25.5 trillion in early 2012.

As of 2009, CDSs were not traded on an exchange and there was no required reporting of transactions to a government agency.

During the 2008 financial crisis, the lack of transparency in this large market became a concern to regulators as it could pose a systemic risk. In March 2010, the Depository Trust & Clearing Corporation (see Sources of Market Data) announced it would give regulators greater access to its credit default swaps database. There was "$8 trillion notional value outstanding" as of June 2018.

A "credit default swap" (CDS) is a credit derivative contract between two counterparties. The buyer makes periodic payments to the seller, and in return receives a payoff if an underlying financial instrument defaults or experiences a similar credit event.

The CDS may refer to a specified loan or bond obligation of a "reference entity", usually a corporation or government. The reference entity is not a party to the contract. The buyer makes regular premium payments to the seller, the premium amounts constituting the "spread" charged in basis points by the seller to insure against a credit event. If the reference entity defaults, the protection seller pays the buyer the par value of the bond in exchange for physical delivery of the bond, although settlement may also be by cash or auction.

A default is often referred to as a "credit event" and includes such events as failure to pay, restructuring and bankruptcy, or even a drop in the borrower's credit rating. CDS contracts on sovereign obligations also usually include as credit events repudiation, moratorium, and acceleration. Most CDSs are in the $10–$20 million range with maturities between one and 10 years. Five years is the most typical maturity.