Community hub

Recent from talks

Contribute something to knowledge base

Content stats: 0 posts, 0 articles, 1 media, 0 notes

Members stats: 0 subscribers, 0 contributors, 0 moderators, 0 supporters

Subscribers

Supporters

Contributors

Moderators

Hub AI

Loss aversion AI simulator

(@Loss aversion_simulator)

Hub AI

Loss aversion AI simulator

(@Loss aversion_simulator)

Loss aversion

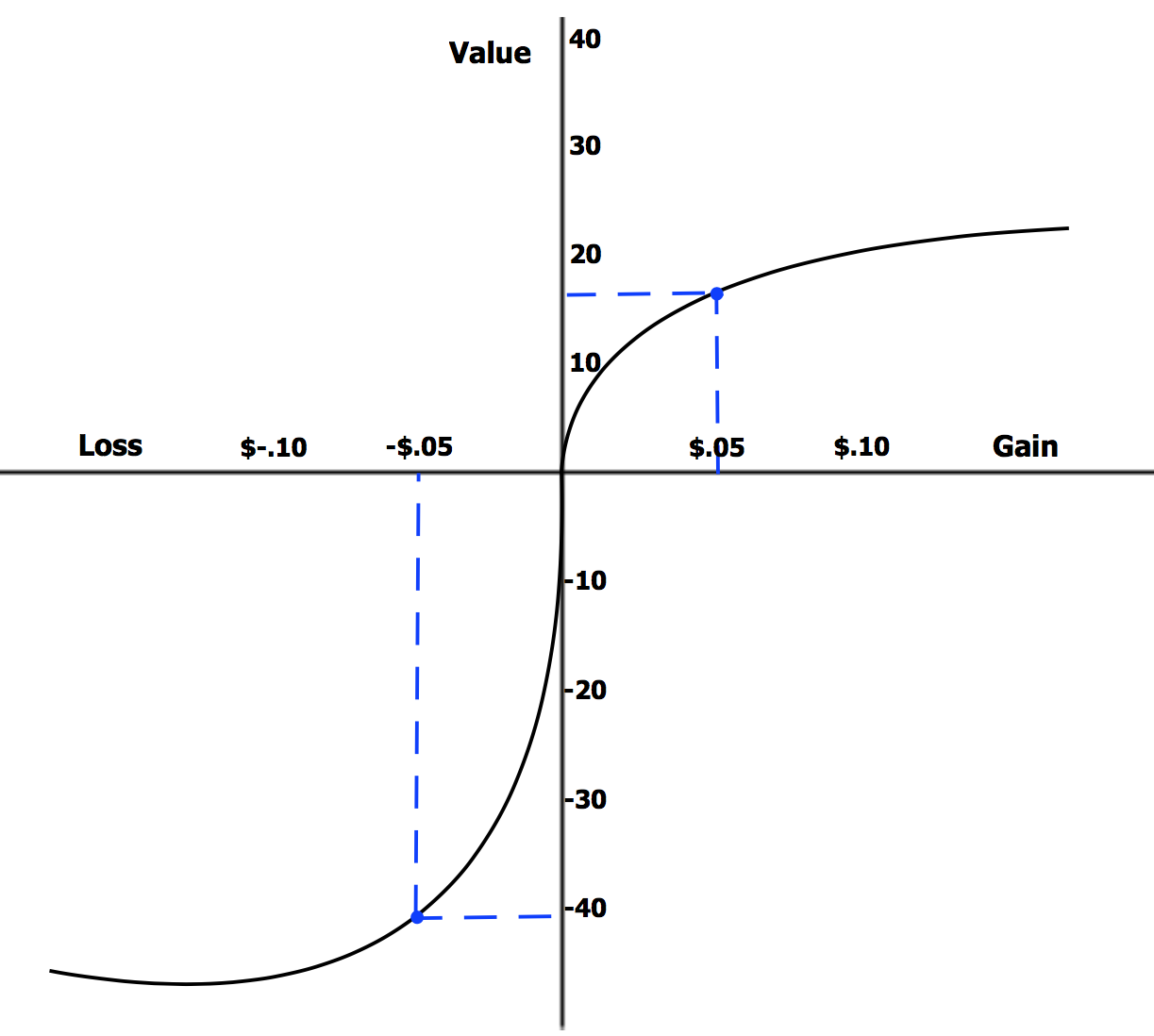

In cognitive science and behavioral economics, loss aversion refers to a cognitive bias in which the same situation is perceived as worse if it is framed as a loss, rather than a gain. It should not be confused with risk aversion, which describes the rational behavior of valuing an uncertain outcome at less than its expected value.

When defined in terms of the pseudo-utility function as in cumulative prospect theory (CPT), the left-hand of the function increases much more steeply than gains, thus being more "painful" than the satisfaction from a comparable gain. Empirically, losses tend to be treated as if they were twice as large as an equivalent gain. Loss aversion was first proposed by Amos Tversky and Daniel Kahneman as an important component of prospect theory.

In 1979, Daniel Kahneman and his associate Amos Tversky originally coined the term "loss aversion" in their initial proposal of prospect theory as an alternative descriptive model of decision making under risk. "The response to losses is stronger than the response to corresponding gains" is Kahneman's definition of loss aversion.

After the first 1979 proposal in the prospect theory framework paper, Tversky and Kahneman used loss aversion for a paper in 1991 about a consumer choice theory that incorporates reference dependence, loss aversion, and diminishing sensitivity. Compared to the original paper above that discusses loss aversion in risky choices, Tversky and Kahneman (1991) discuss loss aversion in riskless choices, for instance, not wanting to trade or even sell something that is already in our possession. Here, "losses loom larger than gains" correspondingly reflects how outcomes below the reference level (e.g. what we do not own) loom larger than those above the reference level (e.g. what we own), showing people's tendency to value losses more than gains relative to a reference point. Additionally, the paper supported loss aversion with the endowment effect theory and status quo bias theory. Loss aversion was popular in explaining many phenomena in traditional choice theory. In 1980, loss aversion was used in Thaler (1980) regarding endowment effect. Loss aversion was also used to support the status quo bias in 1988, and the equity premium puzzle in 1995. In the 2000s, behavioural finance was an area with frequent application of this theory, including on asset prices and individual stock returns.

In marketing, the use of trial periods and rebates tries to take advantage of the buyer's tendency to value the good more after the buyer incorporates it in the status quo. In past behavioral economics studies, users participate up until the threat of loss equals any incurred gains. Methods established by Botond Kőszegi and Matthew Rabin in experimental economics illustrates the role of expectation, wherein an individual's belief about an outcome can create an instance of loss aversion, whether or not a tangible change of state has occurred.

Whether a transaction is framed as a loss or as a gain is important to this calculation. The same change in price framed differently, for example as a $5 discount or as a $5 surcharge avoided, has a significant effect on consumer behavior. Although traditional economists consider this "endowment effect", and all other effects of loss aversion, to be completely irrational, it is important to the fields of marketing and behavioral finance. Users in behavioral and experimental economics studies decided to cease participation in iterative money-making games when the threat of loss was close to the expenditure of effort, even when the user stood to further their gains. Loss aversion coupled with myopia has been shown to explain macroeconomic phenomena, such as the equity premium puzzle. Loss aversion to kinship is an explanation for aversion to inheritance tax.

Loss aversion is part of prospect theory, a cornerstone in behavioral economics. The theory explored numerous behavioral biases leading to sub-optimal decisions making. Kahneman and Tversky found that people are biased in their real estimation of probability of events happening. They tend to over-weight both low and high probabilities and under-weight medium probabilities.

One example is which option is more attractive between option A ($1,500 with a probability of 33%, $1,400 with a probability of 66%, and $0 with a probability of 1%) and option B (a guaranteed $920). Prospect theory and loss aversion suggests that most people would choose option B as they prefer the guaranteed $920 since there is a probability of winning $0, even though it is only 1%. This demonstrates that people think in terms of expected utility relative to a reference point (i.e. current wealth) as opposed to absolute payoffs. When choices are framed as risky (i.e. risk losing 1 out of 10 lives vs the opportunity to save 9 out of 10 lives), individuals tend to be loss-averse as they weigh losses more heavily than comparable gains.

Loss aversion

In cognitive science and behavioral economics, loss aversion refers to a cognitive bias in which the same situation is perceived as worse if it is framed as a loss, rather than a gain. It should not be confused with risk aversion, which describes the rational behavior of valuing an uncertain outcome at less than its expected value.

When defined in terms of the pseudo-utility function as in cumulative prospect theory (CPT), the left-hand of the function increases much more steeply than gains, thus being more "painful" than the satisfaction from a comparable gain. Empirically, losses tend to be treated as if they were twice as large as an equivalent gain. Loss aversion was first proposed by Amos Tversky and Daniel Kahneman as an important component of prospect theory.

In 1979, Daniel Kahneman and his associate Amos Tversky originally coined the term "loss aversion" in their initial proposal of prospect theory as an alternative descriptive model of decision making under risk. "The response to losses is stronger than the response to corresponding gains" is Kahneman's definition of loss aversion.

After the first 1979 proposal in the prospect theory framework paper, Tversky and Kahneman used loss aversion for a paper in 1991 about a consumer choice theory that incorporates reference dependence, loss aversion, and diminishing sensitivity. Compared to the original paper above that discusses loss aversion in risky choices, Tversky and Kahneman (1991) discuss loss aversion in riskless choices, for instance, not wanting to trade or even sell something that is already in our possession. Here, "losses loom larger than gains" correspondingly reflects how outcomes below the reference level (e.g. what we do not own) loom larger than those above the reference level (e.g. what we own), showing people's tendency to value losses more than gains relative to a reference point. Additionally, the paper supported loss aversion with the endowment effect theory and status quo bias theory. Loss aversion was popular in explaining many phenomena in traditional choice theory. In 1980, loss aversion was used in Thaler (1980) regarding endowment effect. Loss aversion was also used to support the status quo bias in 1988, and the equity premium puzzle in 1995. In the 2000s, behavioural finance was an area with frequent application of this theory, including on asset prices and individual stock returns.

In marketing, the use of trial periods and rebates tries to take advantage of the buyer's tendency to value the good more after the buyer incorporates it in the status quo. In past behavioral economics studies, users participate up until the threat of loss equals any incurred gains. Methods established by Botond Kőszegi and Matthew Rabin in experimental economics illustrates the role of expectation, wherein an individual's belief about an outcome can create an instance of loss aversion, whether or not a tangible change of state has occurred.

Whether a transaction is framed as a loss or as a gain is important to this calculation. The same change in price framed differently, for example as a $5 discount or as a $5 surcharge avoided, has a significant effect on consumer behavior. Although traditional economists consider this "endowment effect", and all other effects of loss aversion, to be completely irrational, it is important to the fields of marketing and behavioral finance. Users in behavioral and experimental economics studies decided to cease participation in iterative money-making games when the threat of loss was close to the expenditure of effort, even when the user stood to further their gains. Loss aversion coupled with myopia has been shown to explain macroeconomic phenomena, such as the equity premium puzzle. Loss aversion to kinship is an explanation for aversion to inheritance tax.

Loss aversion is part of prospect theory, a cornerstone in behavioral economics. The theory explored numerous behavioral biases leading to sub-optimal decisions making. Kahneman and Tversky found that people are biased in their real estimation of probability of events happening. They tend to over-weight both low and high probabilities and under-weight medium probabilities.

One example is which option is more attractive between option A ($1,500 with a probability of 33%, $1,400 with a probability of 66%, and $0 with a probability of 1%) and option B (a guaranteed $920). Prospect theory and loss aversion suggests that most people would choose option B as they prefer the guaranteed $920 since there is a probability of winning $0, even though it is only 1%. This demonstrates that people think in terms of expected utility relative to a reference point (i.e. current wealth) as opposed to absolute payoffs. When choices are framed as risky (i.e. risk losing 1 out of 10 lives vs the opportunity to save 9 out of 10 lives), individuals tend to be loss-averse as they weigh losses more heavily than comparable gains.

Recent media

Recent media