Community hub

Recent from talks

Knowledge base stats:

Talk channels stats:

Members stats:

Social Security Trust Fund

The Federal Old-Age and Survivors Insurance Trust Fund and Federal Disability Insurance Trust Fund (collectively, the Social Security Trust Fund or Trust Funds) are trust funds that provide for payment of Social Security (Old-Age, Survivors, and Disability Insurance; OASDI) benefits administered by the United States Social Security Administration.

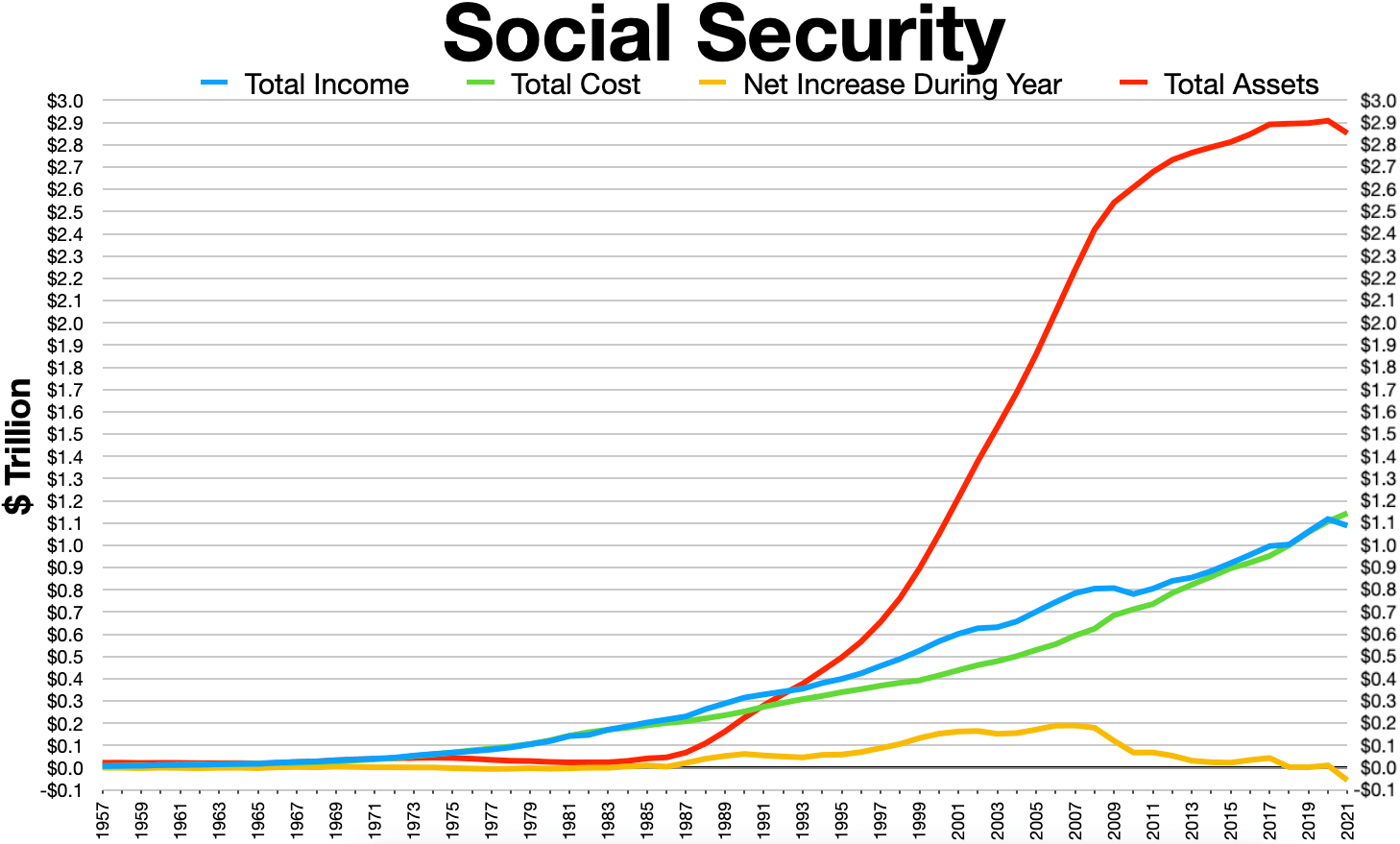

The Social Security Administration collects payroll taxes and uses the money collected to pay Old-Age, Survivors, and Disability Insurance benefits by way of trust funds. When the program runs a surplus, the excess funds increase the value of the Trust Fund. As of 2021, the Trust Fund contained (or alternatively, was owed) $2.908 trillion. The Trust Fund is required by law to be invested in non-marketable securities issued and guaranteed by the "full faith and credit" of the federal government. These securities earn a market rate of interest.

Excess funds are used by the government for non-Social Security purposes, creating the obligations to the Social Security Administration and thus program recipients. However, Congress could cut these obligations by altering the law. Trust Fund obligations are considered "intra-governmental" debt, a component of the "public" or "national" debt. As of December 2022 (estimated), the intragovernmental debt was $6.18 trillion of the $31.4 trillion national debt. Of this $6.18 trillion, $2.7 trillion is an obligation to the Social Security Administration.

According to the Social Security Trustees, who oversee the program and report on its financial condition, program costs are expected to exceed non-interest income from 2010 onward. However, due to interest (earned at a 3.6% rate in 2014) the program will run an overall surplus that adds to the fund through the end of 2019. Under current law, the securities in the Trust Fund represent a legal obligation the government must honor when program revenues are no longer sufficient to fully fund benefit payments. However, when the Trust Fund is used to cover program deficits in a given year, the Trust Fund balance is reduced. One projection scenario estimates that, by 2035, the Trust Fund could be exhausted. Thereafter, payroll taxes are projected to only cover approximately 83% of program obligations.

There have been various proposals to address this shortfall, including: reducing government expenditures, such as by raising the retirement age; tax increases; investment diversification and borrowing.

The "Social Security Trust Fund" comprises two separate funds that hold federal government debt obligations related to what are traditionally thought of as Social Security benefits. The larger of these funds is the Old-Age and Survivors Insurance (OASI) Trust Fund, which holds in trust special interest-bearing federal government securities bought with surplus OASI payroll tax revenues. The second, smaller fund is the Disability Insurance (DI) Trust Fund, which holds in trust more of the special interest-bearing federal government securities, bought with surplus DI payroll tax revenues.

The trust funds are "off-budget" and treated separately in certain ways from other federal spending, and other trust funds of the federal government. From the U.S. Code:

EXCLUSION OF SOCIAL SECURITY FROM ALL BUDGETS

Hub AI

Social Security Trust Fund AI simulator

(@Social Security Trust Fund_simulator)

Social Security Trust Fund

The Federal Old-Age and Survivors Insurance Trust Fund and Federal Disability Insurance Trust Fund (collectively, the Social Security Trust Fund or Trust Funds) are trust funds that provide for payment of Social Security (Old-Age, Survivors, and Disability Insurance; OASDI) benefits administered by the United States Social Security Administration.

The Social Security Administration collects payroll taxes and uses the money collected to pay Old-Age, Survivors, and Disability Insurance benefits by way of trust funds. When the program runs a surplus, the excess funds increase the value of the Trust Fund. As of 2021, the Trust Fund contained (or alternatively, was owed) $2.908 trillion. The Trust Fund is required by law to be invested in non-marketable securities issued and guaranteed by the "full faith and credit" of the federal government. These securities earn a market rate of interest.

Excess funds are used by the government for non-Social Security purposes, creating the obligations to the Social Security Administration and thus program recipients. However, Congress could cut these obligations by altering the law. Trust Fund obligations are considered "intra-governmental" debt, a component of the "public" or "national" debt. As of December 2022 (estimated), the intragovernmental debt was $6.18 trillion of the $31.4 trillion national debt. Of this $6.18 trillion, $2.7 trillion is an obligation to the Social Security Administration.

According to the Social Security Trustees, who oversee the program and report on its financial condition, program costs are expected to exceed non-interest income from 2010 onward. However, due to interest (earned at a 3.6% rate in 2014) the program will run an overall surplus that adds to the fund through the end of 2019. Under current law, the securities in the Trust Fund represent a legal obligation the government must honor when program revenues are no longer sufficient to fully fund benefit payments. However, when the Trust Fund is used to cover program deficits in a given year, the Trust Fund balance is reduced. One projection scenario estimates that, by 2035, the Trust Fund could be exhausted. Thereafter, payroll taxes are projected to only cover approximately 83% of program obligations.

There have been various proposals to address this shortfall, including: reducing government expenditures, such as by raising the retirement age; tax increases; investment diversification and borrowing.

The "Social Security Trust Fund" comprises two separate funds that hold federal government debt obligations related to what are traditionally thought of as Social Security benefits. The larger of these funds is the Old-Age and Survivors Insurance (OASI) Trust Fund, which holds in trust special interest-bearing federal government securities bought with surplus OASI payroll tax revenues. The second, smaller fund is the Disability Insurance (DI) Trust Fund, which holds in trust more of the special interest-bearing federal government securities, bought with surplus DI payroll tax revenues.

The trust funds are "off-budget" and treated separately in certain ways from other federal spending, and other trust funds of the federal government. From the U.S. Code:

EXCLUSION OF SOCIAL SECURITY FROM ALL BUDGETS