Community hub

Recent from talks

Contribute something

Nothing was collected or created yet.

Average variable cost

View on Wikipedia

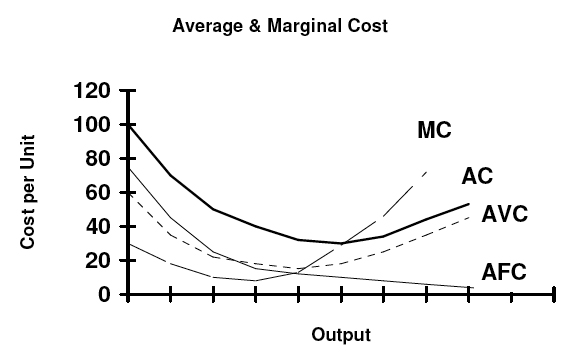

In economics, average variable cost (AVC) is a firm's variable costs (VC; labour, electricity, etc.) divided by the quantity of output produced (Q):

Average variable cost plus average fixed cost equals average total cost (ATC):

A firm would choose to shut down if the price of its output is below average variable cost at the profit-maximizing level of output (or, more generally if it sells at multiple prices, its average revenue is less than AVC). Producing anything would not generate revenue significant enough to offset the associated variable costs; producing some output would add losses (additional costs in excess of revenues) to the costs inevitably being incurred (the fixed costs). By not producing, the firm loses only the fixed costs.

As a result, the firm's short-run supply curve has output of 0 when the price is below the minimum AVC and jumps to output such that for higher prices, where denotes marginal cost.[1]

See also

[edit]References

[edit]- ^ Mankiw, N. Gregory (2001) Principles of Microeconomics, 2e, ch 14, p. 298.

This economics-related article is a stub. You can help Wikipedia by expanding it. |

Average variable cost

View on GrokipediaCore Concepts

Definition

Average variable cost (AVC) is a key concept in microeconomics that measures the variable cost incurred per unit of output produced by a firm, particularly in the short run where some inputs are fixed. It focuses exclusively on costs that fluctuate with production levels, excluding fixed costs such as rent or machinery depreciation. AVC provides insight into the efficiency of variable resource utilization and serves as a benchmark for assessing production scalability.[1] Variable costs, which form the basis of AVC, include expenses directly tied to output volume, such as wages for labor, raw materials, and energy consumption. These costs rise as production increases because more variable inputs are required to generate additional units. In contrast, fixed costs remain unchanged regardless of output. By isolating variable elements, AVC highlights how changes in production affect per-unit expenses from adjustable resources.[2] The formula for average variable cost is derived by dividing total variable cost (TVC) by the quantity of output (Q): This expression quantifies the average expense attributable to variable inputs per unit produced. For instance, if a firm incurs $400 in variable costs to produce 80 units, the AVC is $5 per unit. Understanding AVC is essential for firms to evaluate whether expanding output justifies the additional variable expenses.[1][3]Distinction from Other Costs

Average variable cost (AVC) represents the variable cost per unit of output, calculated as total variable cost divided by the quantity produced, and it specifically excludes fixed costs that do not fluctuate with production levels.[4] This distinction is crucial in short-run economic analysis, where variable costs include expenses like labor and materials that vary directly with output volume, while fixed costs—such as rent or machinery depreciation—remain constant regardless of production quantity.[1] For instance, in a bakery operation, variable costs might encompass flour and wages for additional bakers, but AVC ignores invariant elements like oven rental fees.[5] In contrast to average fixed cost (AFC), which is total fixed cost divided by quantity and declines as output increases due to spreading fixed expenses over more units, AVC often exhibits a U-shaped curve with respect to output, initially falling due to efficiencies in variable input utilization before rising because of diminishing marginal returns to those inputs.[6] AFC, being inversely related to output, approaches zero at high production levels, whereas AVC reflects the per-unit burden of scalable resources and often exhibits a U-shaped curve, initially falling due to efficiencies before rising from inefficiencies.[4] This separation allows firms to isolate the impact of output changes on flexible costs alone. Average total cost (ATC), defined as total cost per unit or the sum of AVC and AFC, incorporates both variable and fixed components, providing a broader measure of overall production efficiency.[1] Unlike AVC, which focuses solely on variable elements and thus lies below ATC on cost curves, ATC declines more gradually at low outputs due to falling AFC but eventually mirrors AVC's shape as fixed costs become negligible.[6] For example, if a firm's AVC is $5 per unit at 100 units of output, but AFC adds $1, then ATC equals $6, highlighting how AVC understates total per-unit expenses.[5] Marginal cost (MC), the additional cost of producing one more unit (change in total cost divided by change in quantity), differs from AVC as it measures incremental changes rather than averages, often intersecting AVC at its minimum point.[1] In the short run, MC equals the change in variable cost per unit since fixed costs do not affect increments, but while AVC averages past variable costs, MC signals future cost trends and drives decisions on output expansion.[6] This relationship underscores that when MC exceeds AVC, the average rises, but below it, AVC falls, aiding in optimizing production levels.[4]Mathematical Formulation

Formula Derivation

The average variable cost (AVC) is derived from the foundational concepts of total variable cost (TVC) and output quantity in the short run, where certain inputs like capital are fixed while others, such as labor, vary with production levels. TVC represents the sum of expenditures on variable inputs required to produce a given quantity of output . Assuming labor is the sole variable input with wage rate , TVC is expressed as , where is the quantity of labor needed to achieve output based on the production function.[7] To obtain AVC, divide TVC by the output quantity: This simplifies by recognizing that the average product of labor (APL) is , the output per unit of labor. Rearranging yields: Thus, AVC is the wage rate divided by the average product of the variable input, reflecting the inverse relationship between productivity and per-unit variable costs. This derivation assumes cost minimization, where the firm employs labor up to the point where the marginal product aligns with input prices, but the core formula holds for any short-run production scenario with variable labor costs. In more general cases with multiple variable inputs, TVC aggregates costs across all such inputs, and AVC remains , though the APL linkage applies primarily to single-input models.[7]Numerical Example

Consider a hypothetical bakery, Bob's Bakery, where fixed costs consist of a daily oven rental fee of $40, while variable costs include labor and ingredients that vary with the number of loaves produced. This example illustrates how average variable cost (AVC) is computed as total variable cost (TVC) divided by the quantity of output (Q).[5] The following table presents data for two output levels, showing the relevant costs and the resulting AVC calculations:| Quantity (Q, loaves per day) | Total Variable Cost (TVC, $) | Average Variable Cost (AVC = TVC / Q, $ per loaf) |

|---|---|---|

| 100 | 500 | 5.00 |

| 150 | 700 | 4.67 |