Community hub

Recent from talks

Contribute something

Nothing was collected or created yet.

Boleto

View on Wikipedia

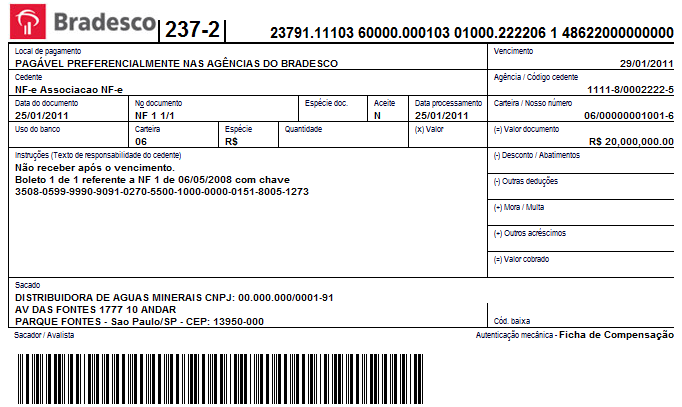

Boleto bancário, simply referred to as boleto (English: bank ticket) is a payment method in Brazil regulated by Febraban (Brazilian Banks Federation).

A boleto, which can be considered a proforma invoice, can be paid at ATMs, branch facilities, and internet banking of any bank, post office, lottery agent and some supermarkets until its due date. After the due date it can only be paid at the issuer bank facilities.[1] A boleto can only be collected by an authorized collector agent in the Brazilian territory.[citation needed]

Open source projects like BoletoPHP allow the merchandisers to generate unregistered boletos bancários without communicating with a bank.[2]

Initially, boletos could only be paid at bank branches, but nowadays it is possible to pay them through ATMs, lottery shops, supermarkets, or with the help of a computer or smartphone via internet banking. Some boletos may contain instructions from the issuer that allow payment even after the set due date, with possible penalty or interest charges for late payment, but these conditions are specific to each issued boleto.

See also

[edit]References

[edit]- ^ "Boleto Bancário for Beginners". The Brazil Business. September 10, 2012.

- ^ "Online Payment for E-Commerce in Brazil - Tech in Brazil". techinbrazil.com.

External links

[edit]

This finance-related article is a stub. You can help Wikipedia by adding missing information. |