Recent from talks

Discounting

Knowledge base stats:

Talk channels stats:

Members stats:

Discounting

In finance, discounting is a mechanism in which a debtor obtains the right to delay payments to a creditor, for a defined period of time, in exchange for a charge or fee. Essentially, the party that owes money in the present purchases the right to delay the payment until some future date. This transaction is based on the fact that most people prefer current interest to delayed interest because of mortality effects, impatience effects, and salience effects. The discount, or charge, is the difference between the original amount owed in the present and the amount that has to be paid in the future to settle the debt.

The discount is usually associated with a discount rate, which is also called the discount yield. The discount yield is the proportional share of the initial amount owed (initial liability) that must be paid to delay payment for 1 year.

Since a person can earn a return on money invested over some period of time, most economic and financial models assume the discount yield is the same as the rate of return the person could receive by investing this money elsewhere (in assets of similar risk) over the given period of time covered by the delay in payment. The concept is associated with the opportunity cost of not having use of the money for the period of time covered by the delay in payment. The relationship between the discount yield and the rate of return on other financial assets is usually discussed in economic and financial theories involving the inter-relation between various market prices, and the achievement of Pareto optimality through the operations in the capitalistic price mechanism, as well as in the discussion of the efficient (financial) market hypothesis. The person delaying the payment of the current liability is essentially compensating the person to whom he/she owes money for the lost revenue that could be earned from an investment during the time period covered by the delay in payment. Accordingly, it is the relevant "discount yield" that determines the "discount", and not the other way around.

As indicated, the rate of return is usually calculated in accordance to an annual return on investment. Since an investor earns a return on the original principal amount of the investment as well as on any prior period investment income, investment earnings are "compounded" as time advances. Therefore, considering the fact that the "discount" must match the benefits obtained from a similar investment asset, the "discount yield" must be used within the same compounding mechanism to negotiate an increase in the size of the "discount" whenever the time period of the payment is delayed or extended. The "discount rate" is the rate at which the "discount" must grow as the delay in payment is extended. This fact is directly tied into the time value of money and its calculations.

The "time value of money" indicates there is a difference between the "future value" of a payment and the "present value" of the same payment. The rate of return on investment should be the dominant factor in evaluating the market's assessment of the difference between the future value and the present value of a payment; and it is the market's assessment that counts the most. Therefore, the "discount yield", which is predetermined by a related return on investment that is found in the different markets in the financial sector, is what is used within the time-value-of-money calculations to determine the "discount" required to delay payment of a financial liability for a given period of time.

If we consider the value of the original payment presently due to be P, and the debtor wants to delay the payment for t years, then a market rate of return denoted r on a similar investment asset means the future value of P is , and the discount can be calculated as

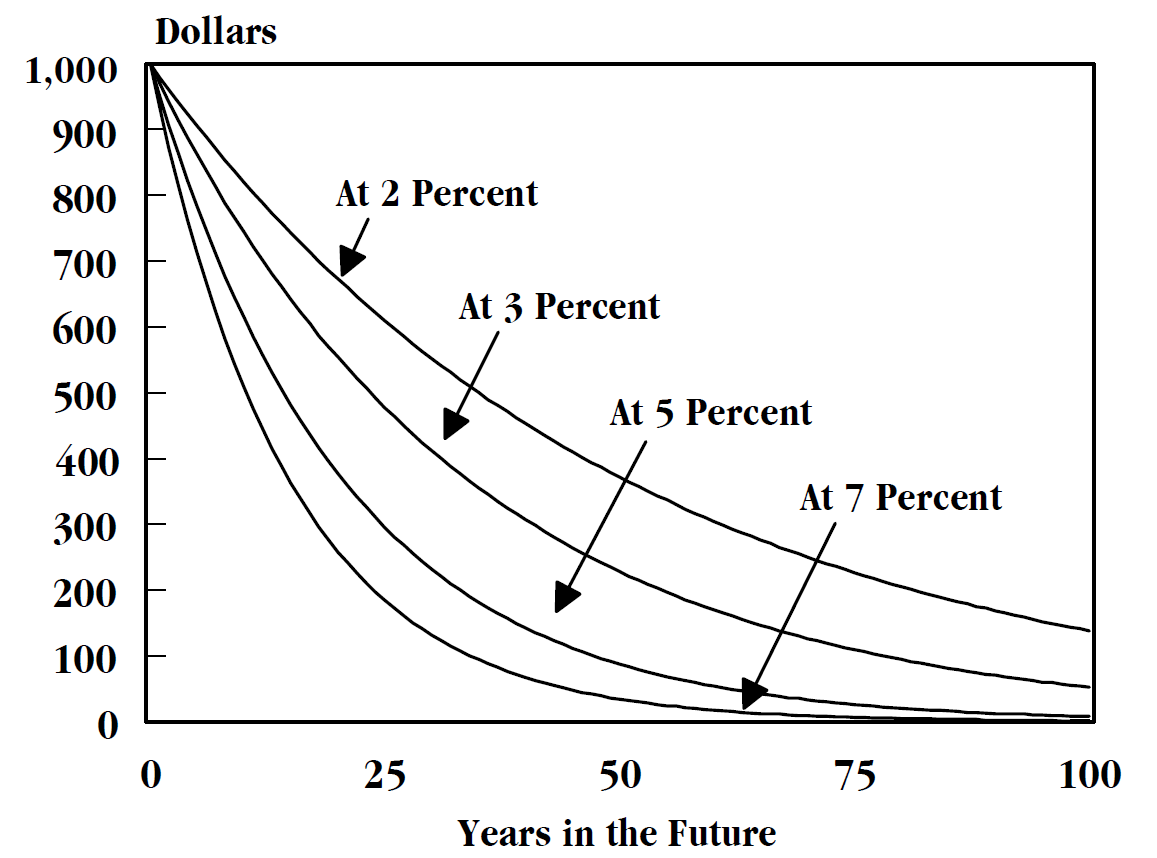

We wish to calculate the present value, also known as the "discounted value" of a payment. Note that a payment made in the future is worth less than the same payment made today which could immediately be deposited into a bank account and earn interest, or invest in other assets. Hence we must discount future payments. Consider a payment F that is to be made t years in the future, we calculate the present value as

Hub AI

Discounting AI simulator

(@Discounting_simulator)

Discounting

In finance, discounting is a mechanism in which a debtor obtains the right to delay payments to a creditor, for a defined period of time, in exchange for a charge or fee. Essentially, the party that owes money in the present purchases the right to delay the payment until some future date. This transaction is based on the fact that most people prefer current interest to delayed interest because of mortality effects, impatience effects, and salience effects. The discount, or charge, is the difference between the original amount owed in the present and the amount that has to be paid in the future to settle the debt.

The discount is usually associated with a discount rate, which is also called the discount yield. The discount yield is the proportional share of the initial amount owed (initial liability) that must be paid to delay payment for 1 year.

Since a person can earn a return on money invested over some period of time, most economic and financial models assume the discount yield is the same as the rate of return the person could receive by investing this money elsewhere (in assets of similar risk) over the given period of time covered by the delay in payment. The concept is associated with the opportunity cost of not having use of the money for the period of time covered by the delay in payment. The relationship between the discount yield and the rate of return on other financial assets is usually discussed in economic and financial theories involving the inter-relation between various market prices, and the achievement of Pareto optimality through the operations in the capitalistic price mechanism, as well as in the discussion of the efficient (financial) market hypothesis. The person delaying the payment of the current liability is essentially compensating the person to whom he/she owes money for the lost revenue that could be earned from an investment during the time period covered by the delay in payment. Accordingly, it is the relevant "discount yield" that determines the "discount", and not the other way around.

As indicated, the rate of return is usually calculated in accordance to an annual return on investment. Since an investor earns a return on the original principal amount of the investment as well as on any prior period investment income, investment earnings are "compounded" as time advances. Therefore, considering the fact that the "discount" must match the benefits obtained from a similar investment asset, the "discount yield" must be used within the same compounding mechanism to negotiate an increase in the size of the "discount" whenever the time period of the payment is delayed or extended. The "discount rate" is the rate at which the "discount" must grow as the delay in payment is extended. This fact is directly tied into the time value of money and its calculations.

The "time value of money" indicates there is a difference between the "future value" of a payment and the "present value" of the same payment. The rate of return on investment should be the dominant factor in evaluating the market's assessment of the difference between the future value and the present value of a payment; and it is the market's assessment that counts the most. Therefore, the "discount yield", which is predetermined by a related return on investment that is found in the different markets in the financial sector, is what is used within the time-value-of-money calculations to determine the "discount" required to delay payment of a financial liability for a given period of time.

If we consider the value of the original payment presently due to be P, and the debtor wants to delay the payment for t years, then a market rate of return denoted r on a similar investment asset means the future value of P is , and the discount can be calculated as

We wish to calculate the present value, also known as the "discounted value" of a payment. Note that a payment made in the future is worth less than the same payment made today which could immediately be deposited into a bank account and earn interest, or invest in other assets. Hence we must discount future payments. Consider a payment F that is to be made t years in the future, we calculate the present value as

Recent media