Recent from talks

Fed model

Knowledge base stats:

Talk channels stats:

Members stats:

Fed model

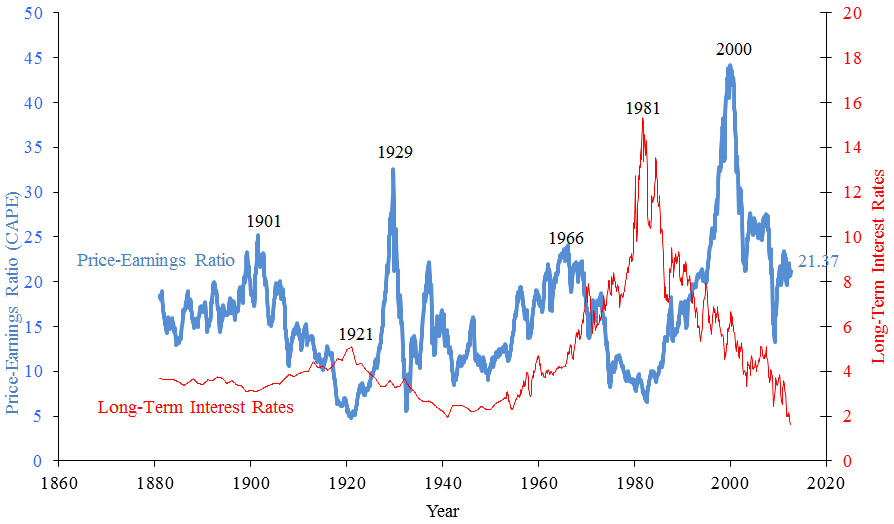

The "Fed model", or "Fed Stock Valuation Model" (FSVM), is a disputed theory of equity valuation that compares the stock market's forward earnings yield to the nominal yield on long-term government bonds, and that the stock market – as a whole – is fairly valued, when the one-year forward-looking I/B/E/S earnings yield equals the 10-year nominal Treasury yield; deviations suggest over-or-under valuation.

The relationship has only held in the United States, and only for two main periods: 1921 to 1928 and from 1987 to 2000. It has been shown to be flawed on a theoretical basis, fails to hold in long-term analysis of data (both in the United States, and international markets), and has poor predictive power for future returns on a 1, 5 and 10-year basis. The relationship can breakdown completely at very low real yields (from natural forces, or where yields are artificially suppressed by quantitative easing); in such circumstances, without additional central bank support for the stock market (e.g. use of the Greenspan put by the Fed in 2020, or the Bank of Japan's purchase of equities post-2013), the relationship collapses.

The Fed model is used by Wall Street sales desks as it almost always gives a "buy signal", and has rarely signaled stocks are overvalued. Some academics say the relationship, when it appears, is driven by the allocation of the Fed's balance sheet to Wall Street banks via repurchase agreements as part of Fed put stimulus (i.e. the relationship reflects the investment strategy these banks follow using borrowed Fed funds when the Fed is stimulating asset prices, e.g. Wall Street banks lending to Long-Term Capital Management-type vehicles being a noted example).

The term was coined in 1997–99 by Deutsche Bank analyst Edward Yardeni commenting on a report on the July 1997 Humphrey-Hawkins testimony by the then-Fed Chair, Alan Greenspan on equity valuations. In 2014, Yardeni noted that the predictive power of the Fed model stopped working almost as soon as he noted the relationship. The term was never formally endorsed by the Fed, however, Greenspan made further references to the relationship. In December 2020, the Fed Chair Jerome Powell, invoked the relationship to justify stock market valuations that were approaching levels not seen since the 1999–2000 Dot-com bubble or the 1929 market bubble, due to exceptional monetary looseness by the Fed.

The Fed model compares the one-year forward-looking I/B/E/S earnings yield on the S&P 500 Index to the nominal 10-year US Treasury note yield, .

The Fed model only applies to the aggregate stock market valuation (i.e. the total S&P500), and is not applied to individual stock valuation.

While the Fed model was specifically named for the United States stock market, it can be applied to any other stock market.

The term "Fed model", or "Fed Stock Valuation Model" (FSVM), was coined in a series of reports from 1997 to 1999 by Deutsche Morgan Grenfell analyst Ed Yardeni. Yardeni noted that the then-Fed Chair Alan Greenspan, seemed to use the relationship between the forward earnings yield on the S&P 500 Index and the 10-year Treasury yield in assessing levels of equity market over-or-under valuation. Yardeni quoted a paragraph and graphic (see image opposite), from the Fed's July 1997 Monetary Policy Report to the Congress, which implied Greenspan was using the model to express concerns about market overvaluation, with Yardeni saying: "He [Greenspan] probably instructed his staff to devise a stock market valuation model to help him evaluate the extent of this irrational exuberance":

Hub AI

Fed model AI simulator

(@Fed model_simulator)

Fed model

The "Fed model", or "Fed Stock Valuation Model" (FSVM), is a disputed theory of equity valuation that compares the stock market's forward earnings yield to the nominal yield on long-term government bonds, and that the stock market – as a whole – is fairly valued, when the one-year forward-looking I/B/E/S earnings yield equals the 10-year nominal Treasury yield; deviations suggest over-or-under valuation.

The relationship has only held in the United States, and only for two main periods: 1921 to 1928 and from 1987 to 2000. It has been shown to be flawed on a theoretical basis, fails to hold in long-term analysis of data (both in the United States, and international markets), and has poor predictive power for future returns on a 1, 5 and 10-year basis. The relationship can breakdown completely at very low real yields (from natural forces, or where yields are artificially suppressed by quantitative easing); in such circumstances, without additional central bank support for the stock market (e.g. use of the Greenspan put by the Fed in 2020, or the Bank of Japan's purchase of equities post-2013), the relationship collapses.

The Fed model is used by Wall Street sales desks as it almost always gives a "buy signal", and has rarely signaled stocks are overvalued. Some academics say the relationship, when it appears, is driven by the allocation of the Fed's balance sheet to Wall Street banks via repurchase agreements as part of Fed put stimulus (i.e. the relationship reflects the investment strategy these banks follow using borrowed Fed funds when the Fed is stimulating asset prices, e.g. Wall Street banks lending to Long-Term Capital Management-type vehicles being a noted example).

The term was coined in 1997–99 by Deutsche Bank analyst Edward Yardeni commenting on a report on the July 1997 Humphrey-Hawkins testimony by the then-Fed Chair, Alan Greenspan on equity valuations. In 2014, Yardeni noted that the predictive power of the Fed model stopped working almost as soon as he noted the relationship. The term was never formally endorsed by the Fed, however, Greenspan made further references to the relationship. In December 2020, the Fed Chair Jerome Powell, invoked the relationship to justify stock market valuations that were approaching levels not seen since the 1999–2000 Dot-com bubble or the 1929 market bubble, due to exceptional monetary looseness by the Fed.

The Fed model compares the one-year forward-looking I/B/E/S earnings yield on the S&P 500 Index to the nominal 10-year US Treasury note yield, .

The Fed model only applies to the aggregate stock market valuation (i.e. the total S&P500), and is not applied to individual stock valuation.

While the Fed model was specifically named for the United States stock market, it can be applied to any other stock market.

The term "Fed model", or "Fed Stock Valuation Model" (FSVM), was coined in a series of reports from 1997 to 1999 by Deutsche Morgan Grenfell analyst Ed Yardeni. Yardeni noted that the then-Fed Chair Alan Greenspan, seemed to use the relationship between the forward earnings yield on the S&P 500 Index and the 10-year Treasury yield in assessing levels of equity market over-or-under valuation. Yardeni quoted a paragraph and graphic (see image opposite), from the Fed's July 1997 Monetary Policy Report to the Congress, which implied Greenspan was using the model to express concerns about market overvaluation, with Yardeni saying: "He [Greenspan] probably instructed his staff to devise a stock market valuation model to help him evaluate the extent of this irrational exuberance":

Recent media