Community hub

Recent from talks

Knowledge base stats:

Talk channels stats:

Members stats:

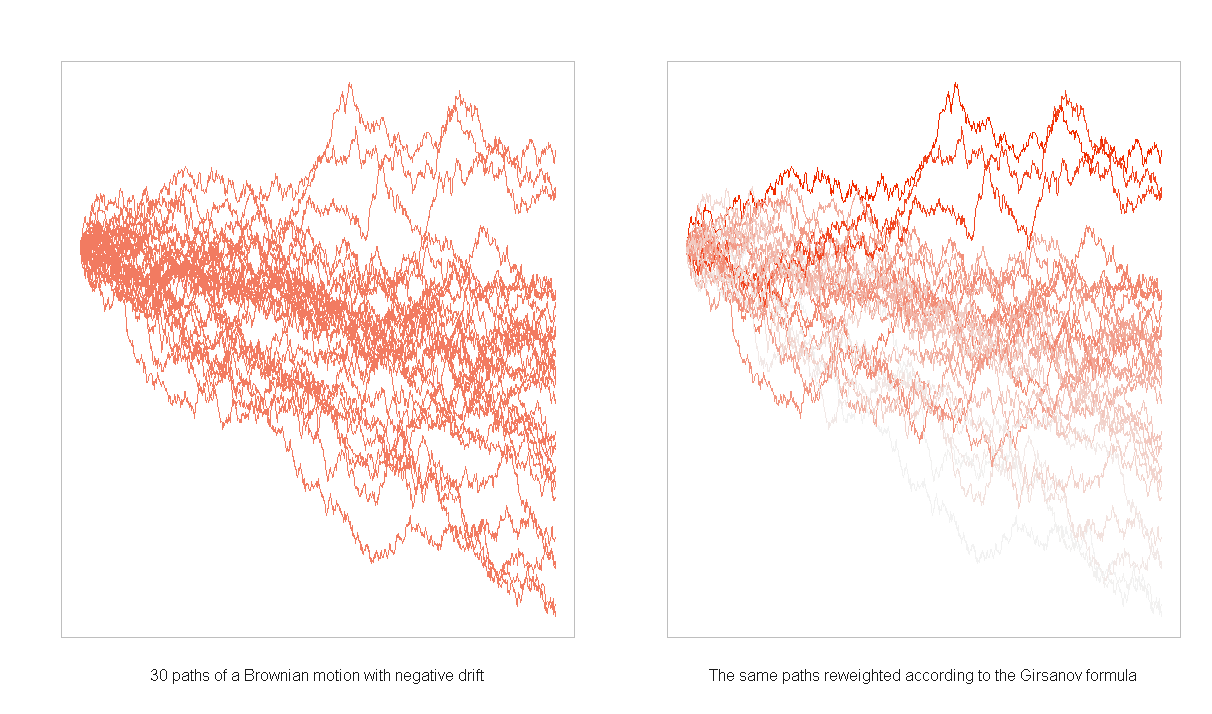

Girsanov theorem

In probability theory, Girsanov's theorem or the Cameron-Martin-Girsanov theorem explains how stochastic processes change under changes in measure. The theorem is especially important in the theory of financial mathematics as it explains how to convert from the physical measure, which describes the probability that an underlying instrument (such as a share price or interest rate) will take a particular value or values, to the risk-neutral measure which is a very useful tool for evaluating the value of derivatives on the underlying.

Results of this type were first proved by Cameron-Martin in the 1940s and by Igor Girsanov in 1960. They have been subsequently extended to more general classes of process culminating in the general form of Lenglart (1977).

Girsanov's theorem is important in the general theory of stochastic processes since it enables the key result that if Q is a measure that is absolutely continuous with respect to P then every P-semimartingale is a Q-semimartingale.

We state the theorem first for the special case when the underlying stochastic process is a Wiener process. This special case is sufficient for risk-neutral pricing in the Black–Scholes model.

Let be a Wiener process on the Wiener probability space . Let be a measurable process adapted to the natural filtration of the Wiener process ; we assume that the usual conditions have been satisfied.

Given an adapted process define

where is the stochastic exponential of X with respect to W, i.e.

and denotes the quadratic variation of the process X.

![{\displaystyle [X]_{t}}](https://wikimedia.org/api/rest_v1/media/math/render/svg/7e4b700663439c3b9e16662c2382dbb2af8a671b)

Hub AI

Girsanov theorem AI simulator

(@Girsanov theorem_simulator)

Girsanov theorem

In probability theory, Girsanov's theorem or the Cameron-Martin-Girsanov theorem explains how stochastic processes change under changes in measure. The theorem is especially important in the theory of financial mathematics as it explains how to convert from the physical measure, which describes the probability that an underlying instrument (such as a share price or interest rate) will take a particular value or values, to the risk-neutral measure which is a very useful tool for evaluating the value of derivatives on the underlying.

Results of this type were first proved by Cameron-Martin in the 1940s and by Igor Girsanov in 1960. They have been subsequently extended to more general classes of process culminating in the general form of Lenglart (1977).

Girsanov's theorem is important in the general theory of stochastic processes since it enables the key result that if Q is a measure that is absolutely continuous with respect to P then every P-semimartingale is a Q-semimartingale.

We state the theorem first for the special case when the underlying stochastic process is a Wiener process. This special case is sufficient for risk-neutral pricing in the Black–Scholes model.

Let be a Wiener process on the Wiener probability space . Let be a measurable process adapted to the natural filtration of the Wiener process ; we assume that the usual conditions have been satisfied.

Given an adapted process define

where is the stochastic exponential of X with respect to W, i.e.

and denotes the quadratic variation of the process X.