Community hub

Recent from talks

Knowledge base stats:

Talk channels stats:

Members stats:

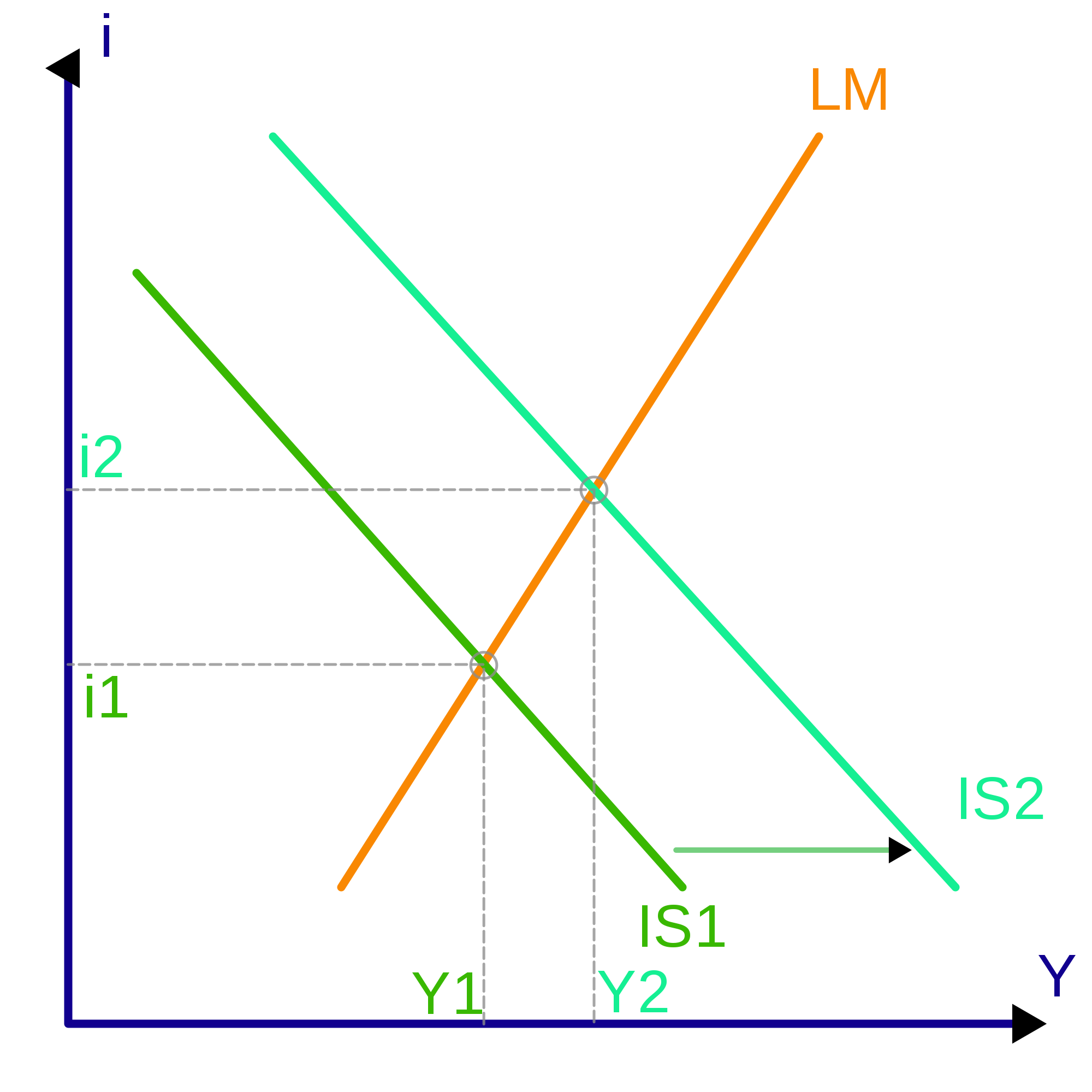

IS–LM model

The IS–LM model, or Hicks–Hansen model, is a two-dimensional macroeconomic model which is used as a pedagogical tool in macroeconomic teaching. The IS–LM model shows the relationship between interest rates and output in the short run. The intersection of the "investment–saving" (IS) and "liquidity preference–money supply" (LM) curves illustrates a "general equilibrium" where supposed simultaneous equilibria occur in both the goods and the money markets. The IS–LM model shows the importance of various demand shocks (including the effects of monetary policy and fiscal policy) on output and consequently offers an explanation of changes in national income in the short run when prices are fixed or sticky. Hence, the model can be used as a tool to suggest potential levels for appropriate stabilisation policies. It is also used as a building block for the demand side of the economy in more comprehensive models like the AD–AS model.

The model was developed by John Hicks in 1937 and was later extended by Alvin Hansen as a mathematical representation of Keynesian macroeconomic theory. Between the 1940s and mid-1970s, it was the leading framework of macroeconomic analysis. Today, it is generally accepted as being imperfect and is largely absent from teaching at advanced economic levels and from macroeconomic research, but it is still an important pedagogical introductory tool in most undergraduate macroeconomics textbooks.

As monetary policy since the 1980s and 1990s generally does not try to target money supply as assumed in the original IS–LM model, but instead targets interest rate levels directly, some modern versions of the model have changed the interpretation (and in some cases even the name) of the LM curve, presenting it instead simply as a horizontal line showing the central bank's choice of interest rate. This allows for a simpler dynamic adjustment and supposedly reflects the behaviour of actual contemporary central banks more closely.

The IS–LM model was introduced at a conference of the Econometric Society held in Oxford during September 1936. Roy Harrod, John R. Hicks, and James Meade all presented papers describing mathematical models attempting to summarize John Maynard Keynes' General Theory of Employment, Interest, and Money. Hicks, who had seen a draft of Harrod's paper, invented the IS–LM model (originally using the abbreviation "LL", not "LM"). He later presented it in "Mr. Keynes and the Classics: A Suggested Interpretation". Hicks and Alvin Hansen developed the model further in the 1930s and early 1940s, Hansen extending the earlier contribution. The model became a central tool of macroeconomic teaching for many decades. Between the 1940s and mid-1970s, it was the leading framework of macroeconomic analysis. It was particularly suited to illustrate the debate of the 1960s and 1970s between Keynesians and monetarists as to whether fiscal or monetary policy was most effective to stabilize the economy. Later, this issue faded from focus and came to play only a modest role in discussions of short-run fluctuations.

The IS-LM model assumes a fixed price level and consequently cannot in itself be used to analyze inflation. This was of little importance in the 1950s and early 1960s when inflation was not an important issue, but became problematic with the rising inflation levels in the late 1960s and 1970s, which led to extensions of the model to also incorporate aggregate supply in some form, e.g. in the form of the AD–AS model, which can be regarded as an IS-LM model with an added supply side explaining rises in the price level.

One of the basic assumptions of the IS-LM model is that the central bank targets the money supply. However, a fundamental rethinking in central bank policy took place from the early 1990s when central banks generally changed strategies towards targeting inflation rather than money growth and using an interest rate rule to achieve their goal. As central banks started paying little attention to the money supply when deciding on their policy, this model feature became increasingly unrealistic and sometimes confusing to students. David Romer in 2000 suggested replacing the traditional IS-LM framework with an IS-MP model, replacing the positively sloped LM curve with a horizontal MP curve (where MP stands for "monetary policy"). He advocated that it had several advantages compared to the traditional IS-LM model. John B. Taylor independently made a similar recommendation in the same year. After 2000, this has led to various modifications to the model in many textbooks, replacing the traditional LM curve and story of the central bank influencing the interest rate level indirectly via controlling the supply of money in the money market to a more realistic one of the central bank determining the policy interest rate as an exogenous variable directly.

Today, the IS-LM model is largely absent from macroeconomic research, but it is still a backbone conceptual introductory tool in many macroeconomics textbooks.

The point where the IS and LM schedules intersect represents a short-run equilibrium in the real and monetary sectors (though not necessarily in other sectors, such as labor markets): both the product market and the money market are in equilibrium. This equilibrium yields a unique combination of the interest rate and real GDP.

Hub AI

IS–LM model AI simulator

(@IS–LM model_simulator)

IS–LM model

The IS–LM model, or Hicks–Hansen model, is a two-dimensional macroeconomic model which is used as a pedagogical tool in macroeconomic teaching. The IS–LM model shows the relationship between interest rates and output in the short run. The intersection of the "investment–saving" (IS) and "liquidity preference–money supply" (LM) curves illustrates a "general equilibrium" where supposed simultaneous equilibria occur in both the goods and the money markets. The IS–LM model shows the importance of various demand shocks (including the effects of monetary policy and fiscal policy) on output and consequently offers an explanation of changes in national income in the short run when prices are fixed or sticky. Hence, the model can be used as a tool to suggest potential levels for appropriate stabilisation policies. It is also used as a building block for the demand side of the economy in more comprehensive models like the AD–AS model.

The model was developed by John Hicks in 1937 and was later extended by Alvin Hansen as a mathematical representation of Keynesian macroeconomic theory. Between the 1940s and mid-1970s, it was the leading framework of macroeconomic analysis. Today, it is generally accepted as being imperfect and is largely absent from teaching at advanced economic levels and from macroeconomic research, but it is still an important pedagogical introductory tool in most undergraduate macroeconomics textbooks.

As monetary policy since the 1980s and 1990s generally does not try to target money supply as assumed in the original IS–LM model, but instead targets interest rate levels directly, some modern versions of the model have changed the interpretation (and in some cases even the name) of the LM curve, presenting it instead simply as a horizontal line showing the central bank's choice of interest rate. This allows for a simpler dynamic adjustment and supposedly reflects the behaviour of actual contemporary central banks more closely.

The IS–LM model was introduced at a conference of the Econometric Society held in Oxford during September 1936. Roy Harrod, John R. Hicks, and James Meade all presented papers describing mathematical models attempting to summarize John Maynard Keynes' General Theory of Employment, Interest, and Money. Hicks, who had seen a draft of Harrod's paper, invented the IS–LM model (originally using the abbreviation "LL", not "LM"). He later presented it in "Mr. Keynes and the Classics: A Suggested Interpretation". Hicks and Alvin Hansen developed the model further in the 1930s and early 1940s, Hansen extending the earlier contribution. The model became a central tool of macroeconomic teaching for many decades. Between the 1940s and mid-1970s, it was the leading framework of macroeconomic analysis. It was particularly suited to illustrate the debate of the 1960s and 1970s between Keynesians and monetarists as to whether fiscal or monetary policy was most effective to stabilize the economy. Later, this issue faded from focus and came to play only a modest role in discussions of short-run fluctuations.

The IS-LM model assumes a fixed price level and consequently cannot in itself be used to analyze inflation. This was of little importance in the 1950s and early 1960s when inflation was not an important issue, but became problematic with the rising inflation levels in the late 1960s and 1970s, which led to extensions of the model to also incorporate aggregate supply in some form, e.g. in the form of the AD–AS model, which can be regarded as an IS-LM model with an added supply side explaining rises in the price level.

One of the basic assumptions of the IS-LM model is that the central bank targets the money supply. However, a fundamental rethinking in central bank policy took place from the early 1990s when central banks generally changed strategies towards targeting inflation rather than money growth and using an interest rate rule to achieve their goal. As central banks started paying little attention to the money supply when deciding on their policy, this model feature became increasingly unrealistic and sometimes confusing to students. David Romer in 2000 suggested replacing the traditional IS-LM framework with an IS-MP model, replacing the positively sloped LM curve with a horizontal MP curve (where MP stands for "monetary policy"). He advocated that it had several advantages compared to the traditional IS-LM model. John B. Taylor independently made a similar recommendation in the same year. After 2000, this has led to various modifications to the model in many textbooks, replacing the traditional LM curve and story of the central bank influencing the interest rate level indirectly via controlling the supply of money in the money market to a more realistic one of the central bank determining the policy interest rate as an exogenous variable directly.

Today, the IS-LM model is largely absent from macroeconomic research, but it is still a backbone conceptual introductory tool in many macroeconomics textbooks.

The point where the IS and LM schedules intersect represents a short-run equilibrium in the real and monetary sectors (though not necessarily in other sectors, such as labor markets): both the product market and the money market are in equilibrium. This equilibrium yields a unique combination of the interest rate and real GDP.