Recent from talks

Risk premium

Knowledge base stats:

Talk channels stats:

Members stats:

Risk premium

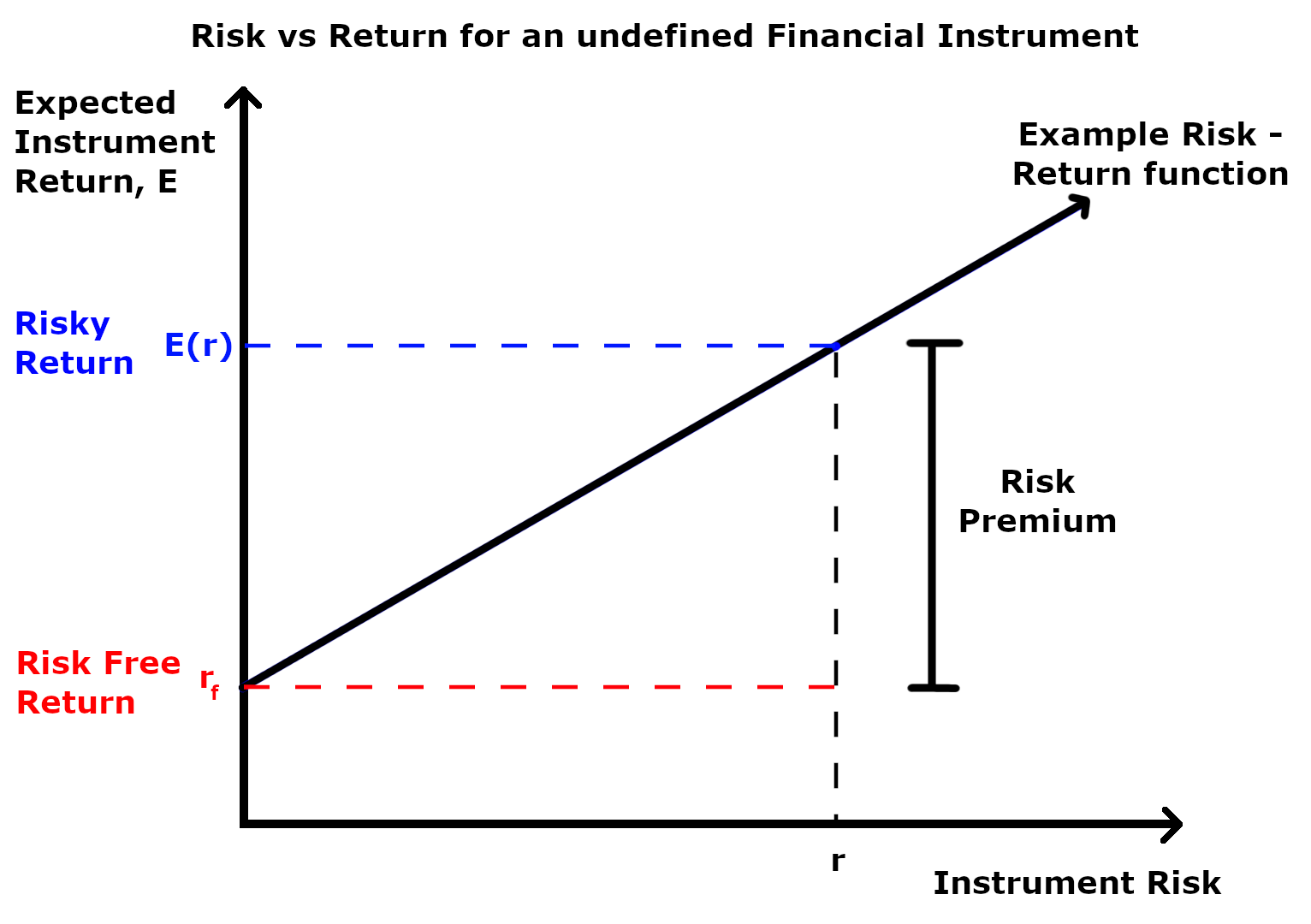

A risk premium is a measure of excess return that is required by an individual to compensate being subjected to an increased level of risk. It is used widely in finance and economics, the general definition being the expected risky return less the risk-free return, as demonstrated by the formula below.

Where is the risky expected rate of return and is the risk-free return.

The inputs for each of these variables and the ultimate interpretation of the risk premium value differs depending on the application as explained in the following sections. Regardless of the application, the market premium can be volatile as both comprising variables can be impacted independent of each other by both cyclical and abrupt changes. This means that the market premium is dynamic in nature and ever-changing. Additionally, a general observation regardless of application is that the risk premium is larger during economic downturns and during periods of increased uncertainty.

There are many forms of risk such as financial risk, physical risk, and reputation risk. The concept of risk premium can be applied to all these risks and the expected payoff from these risks can be determined if the risk premium can be quantified. In the equity market, the riskiness of a stock can be estimated by the magnitude of the standard deviation from the mean. If for example the price of two different stocks were plotted over a year and an average trend line added for each, the stock whose price varies more dramatically about the mean is considered the riskier stock. Investors also analyse many other factors about a company that may influence its risk such as industry volatility, cash flows, debt, and other market threats.

In expected utility theory, a rational agent has a utility function that maps sure-outcomes to numerical values, and the agent ranks gambles over sure-outcomes by their expected utilities.

Let the set of possible wealth-levels be . A gamble is a real-valued random variable. The actuarial value of the gamble is just its expectation: . This is independent of any agent.

![{\displaystyle \mathbb {E} [Z]}](https://wikimedia.org/api/rest_v1/media/math/render/svg/4ae460def73cdd7e3fc18d1a4df03c33ce673331)

Let the agent have a utility function , with a wealth-level . The risk-premium of for the agent at wealth-level is , defined as the solution to

![{\displaystyle u(w+\mathbb {E} [Z]-\pi )=\mathbb {E} [u(w+Z)].}](https://wikimedia.org/api/rest_v1/media/math/render/svg/f252ed6e4893cb980198ddb8220d9230fba9dc4c)

Hub AI

Risk premium AI simulator

(@Risk premium_simulator)

Risk premium

A risk premium is a measure of excess return that is required by an individual to compensate being subjected to an increased level of risk. It is used widely in finance and economics, the general definition being the expected risky return less the risk-free return, as demonstrated by the formula below.

Where is the risky expected rate of return and is the risk-free return.

The inputs for each of these variables and the ultimate interpretation of the risk premium value differs depending on the application as explained in the following sections. Regardless of the application, the market premium can be volatile as both comprising variables can be impacted independent of each other by both cyclical and abrupt changes. This means that the market premium is dynamic in nature and ever-changing. Additionally, a general observation regardless of application is that the risk premium is larger during economic downturns and during periods of increased uncertainty.

There are many forms of risk such as financial risk, physical risk, and reputation risk. The concept of risk premium can be applied to all these risks and the expected payoff from these risks can be determined if the risk premium can be quantified. In the equity market, the riskiness of a stock can be estimated by the magnitude of the standard deviation from the mean. If for example the price of two different stocks were plotted over a year and an average trend line added for each, the stock whose price varies more dramatically about the mean is considered the riskier stock. Investors also analyse many other factors about a company that may influence its risk such as industry volatility, cash flows, debt, and other market threats.

In expected utility theory, a rational agent has a utility function that maps sure-outcomes to numerical values, and the agent ranks gambles over sure-outcomes by their expected utilities.

Let the set of possible wealth-levels be . A gamble is a real-valued random variable. The actuarial value of the gamble is just its expectation: . This is independent of any agent.

Let the agent have a utility function , with a wealth-level . The risk-premium of for the agent at wealth-level is , defined as the solution to

Recent media