Recent from talks

Carried interest

Knowledge base stats:

Talk channels stats:

Members stats:

Carried interest

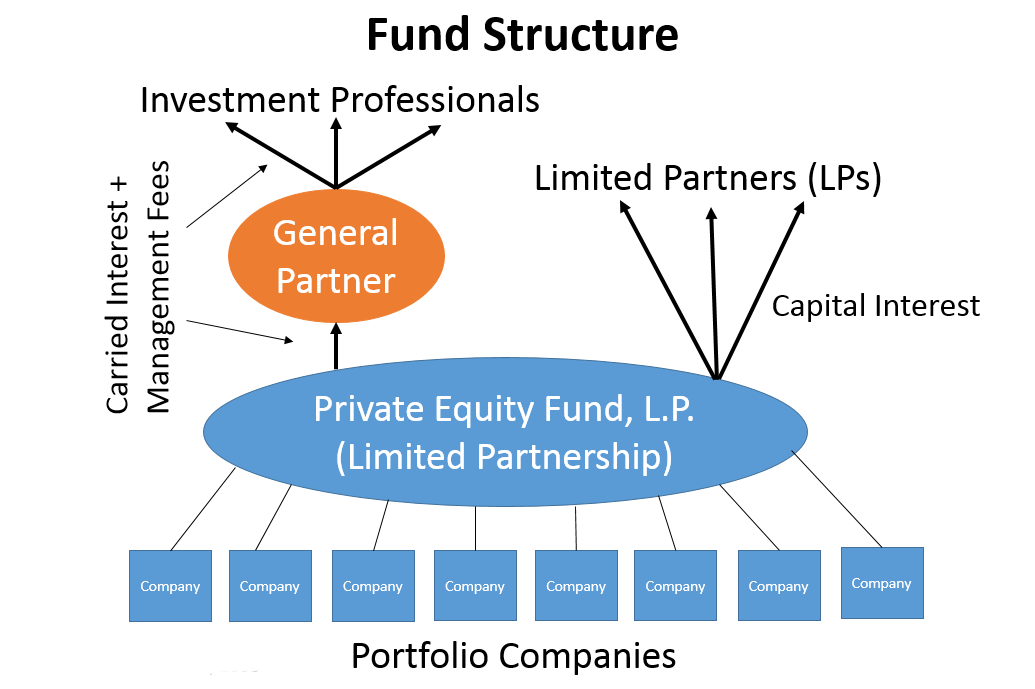

Carried interest, or carry, in finance, is a share of the profits of an investment paid to the investment manager specifically in alternative investments (private equity and hedge funds). It is a performance fee, rewarding the manager for enhancing performance. Since these fees are generally not taxed as normal income, some believe that the structure unfairly takes advantage of favorable tax treatment, e.g. in the United States. In this regard, it is often referred to as the carried interest loophole. The Hill referred to it as "Wall Street's favorite tax break."

The origin of carried interest can be traced to the 16th century when European ships were crossing to Asia and the Americas. The captain of the ship would take a 20% share of the profit from the carried goods to pay for the transport and the risk of sailing over oceans. The name is not connected with interest rates or interest payments on a loan or bank account.

Today, the term is used to name the compensation collected by investment executives in private equity funds. In the United States, carried interest is taxed at the same rate as long-term capital gains. Because this tax rate is fairly low, the policy has been criticized as a form of tax avoidance.

Carried interest is a share of the profits of an investment paid to the investment manager in excess of the amount that the manager contributes to the partnership, specifically in alternative investments, e.g., private equity and hedge funds. It is a performance fee rewarding the manager for enhancing performance.

The manager's carried interest allocation varies depending on the type of investment fund and the demand for the fund from investors. In private equity, the standard carried interest allocation historically has been 20% for funds making buyout and venture investments, but there is some variability. Notable examples of private equity firms with carried interest of more than 20% ("super carry") include Bain Capital and Providence Equity Partners. Hedge fund carry percentages have historically centered on 20% but have had greater variability than those of private equity funds. In extreme cases performance fees have reached as high as 44% of a fund's profits but is usually between 15% and 20%.

The distribution of fund returns is often directed by a distribution waterfall. Returns generated by the investment are first distributed to return each investor's initial capital contribution, including the manager. This is not "carried interest" because it is a repayment of principal. Second, returns are paid to investors other than the manager, up to a certain previously agreed rate of return (the "hurdle rate" or "preferred return"). The customary hurdle rate is 7% to 9% per annum. Third, returns are paid to the manager until it has received a rate of return equal to the hurdle rate (the "catch-up"). Not every fund provides for a hurdle and a catch-up. Often, returns during the catch-up phase are split with the manager receiving the larger (e.g. 80%) share and the investors receiving a smaller (e.g. 20%) share, until the manager's catch-up percentage has been collected. Fourth, once the manager's returns equal the investor returns, the split reverses, with the manager taking a lower (often 20%) share and the investors taking the higher (often 80%) share. All manager returns above the returns from the manager's initial contribution are "carry" or "carried interest."

Private equity funds distribute carried interest to managers and other investors only upon a successful exit from an investment, which may take years. In a hedge fund environment, carried interest is usually referred to as a "performance fee" and because it invests in liquid investments, it is often able to pay carried interest annually if the fund has generated a profit. This has implications for both the amount and timing of the taxes on the interest.

Historically, carried interest has served as the primary source of income for manager and firm in both private equity and hedge funds. Both funds also tend to have an annual management fee of 1% to 2% of assets under management per year. The management fee covers the costs of investing and managing the fund. The management fee, unlike the 20% carried interest, is treated as ordinary income in the United States. As the sizes of both private equity and hedge funds have increased, management fees have become a more meaningful portion of the value proposition for fund managers as evidenced by the 2007 initial public offering of the Blackstone Group.

Hub AI

Carried interest AI simulator

(@Carried interest_simulator)

Carried interest

Carried interest, or carry, in finance, is a share of the profits of an investment paid to the investment manager specifically in alternative investments (private equity and hedge funds). It is a performance fee, rewarding the manager for enhancing performance. Since these fees are generally not taxed as normal income, some believe that the structure unfairly takes advantage of favorable tax treatment, e.g. in the United States. In this regard, it is often referred to as the carried interest loophole. The Hill referred to it as "Wall Street's favorite tax break."

The origin of carried interest can be traced to the 16th century when European ships were crossing to Asia and the Americas. The captain of the ship would take a 20% share of the profit from the carried goods to pay for the transport and the risk of sailing over oceans. The name is not connected with interest rates or interest payments on a loan or bank account.

Today, the term is used to name the compensation collected by investment executives in private equity funds. In the United States, carried interest is taxed at the same rate as long-term capital gains. Because this tax rate is fairly low, the policy has been criticized as a form of tax avoidance.

Carried interest is a share of the profits of an investment paid to the investment manager in excess of the amount that the manager contributes to the partnership, specifically in alternative investments, e.g., private equity and hedge funds. It is a performance fee rewarding the manager for enhancing performance.

The manager's carried interest allocation varies depending on the type of investment fund and the demand for the fund from investors. In private equity, the standard carried interest allocation historically has been 20% for funds making buyout and venture investments, but there is some variability. Notable examples of private equity firms with carried interest of more than 20% ("super carry") include Bain Capital and Providence Equity Partners. Hedge fund carry percentages have historically centered on 20% but have had greater variability than those of private equity funds. In extreme cases performance fees have reached as high as 44% of a fund's profits but is usually between 15% and 20%.

The distribution of fund returns is often directed by a distribution waterfall. Returns generated by the investment are first distributed to return each investor's initial capital contribution, including the manager. This is not "carried interest" because it is a repayment of principal. Second, returns are paid to investors other than the manager, up to a certain previously agreed rate of return (the "hurdle rate" or "preferred return"). The customary hurdle rate is 7% to 9% per annum. Third, returns are paid to the manager until it has received a rate of return equal to the hurdle rate (the "catch-up"). Not every fund provides for a hurdle and a catch-up. Often, returns during the catch-up phase are split with the manager receiving the larger (e.g. 80%) share and the investors receiving a smaller (e.g. 20%) share, until the manager's catch-up percentage has been collected. Fourth, once the manager's returns equal the investor returns, the split reverses, with the manager taking a lower (often 20%) share and the investors taking the higher (often 80%) share. All manager returns above the returns from the manager's initial contribution are "carry" or "carried interest."

Private equity funds distribute carried interest to managers and other investors only upon a successful exit from an investment, which may take years. In a hedge fund environment, carried interest is usually referred to as a "performance fee" and because it invests in liquid investments, it is often able to pay carried interest annually if the fund has generated a profit. This has implications for both the amount and timing of the taxes on the interest.

Historically, carried interest has served as the primary source of income for manager and firm in both private equity and hedge funds. Both funds also tend to have an annual management fee of 1% to 2% of assets under management per year. The management fee covers the costs of investing and managing the fund. The management fee, unlike the 20% carried interest, is treated as ordinary income in the United States. As the sizes of both private equity and hedge funds have increased, management fees have become a more meaningful portion of the value proposition for fund managers as evidenced by the 2007 initial public offering of the Blackstone Group.

Recent media