Community hub

Recent from talks

Contribute something

Nothing was collected or created yet.

Audit

View on Wikipedia| Part of a series on |

| Accounting |

|---|

|

An audit is an "independent examination of financial information of any entity, whether profit oriented or not, irrespective of its size or legal form when such an examination is conducted with a view to express an opinion thereon."[1] Auditing also attempts to ensure that the books of accounts are properly maintained by such entities as required by law. Auditors consider the propositions before them, obtain evidence, roll forward prior year working papers, and evaluate the propositions in their auditing report.[2]

Audits provide third-party assurance to various stakeholders that the subject matter is free from material misstatement.[3] The term is most frequently applied to audits of the financial information relating to a legal person. Other commonly audited areas include: secretarial and compliance, internal controls, quality management, project management, water management, and energy conservation. As a result of an audit, stakeholders may evaluate and improve the effectiveness of risk management, control, and governance over the subject matter.

In recent years auditing has expanded to encompass many areas of public and corporate life. Professor Michael Power refers to this extension of auditing practices as the "Audit Society".[4]

Etymology

[edit]The word "audit" derives from the Latin word audire which means "to hear".[5]

History

[edit]Auditing has been a safeguard measure since ancient times.[6] During medieval times, when manual bookkeeping was prevalent, auditors in Britain used to hear the accounts read out for them and checked that the organization's personnel were not negligent or fraudulent.[7] In 1951, Moyer identified that the most important duty of the auditor was to detect fraud.[8] Chatfield documented that early United States auditing was viewed mainly as verification of bookkeeping detail.[9]

The Central Auditing Commission of the Communist Party of the Soviet Union (Russian: Центральная ревизионная комиссия КПСС) operated from 1921 to 1990.

Information technology audit

[edit]An information technology audit, or information systems audit, is an examination of the management controls within an Information technology (IT) infrastructure. The evaluation of obtained evidence determines if the information systems are safeguarding assets, maintaining data integrity, and operating effectively to achieve the organization's goals or objectives. These reviews may be performed in conjunction with a financial statement audit, internal audit, or other form of attestation engagement.

Accounting

[edit]Due to strong incentives (including taxation, misselling and other forms of fraud) to misstate financial information, auditing has become a legal requirement for many entities who have the power to exploit financial information for personal gain. Traditionally, audits were mainly associated with gaining information about financial systems and the financial records of a company or a business. Financial audits also assess whether a business or corporation adheres to legal duties as well as other applicable statutory customs and regulations.[10][11]

Financial audits are performed to ascertain the validity and reliability of information, as well as to provide an assessment of a system's internal control. The third party auditor will express an opinion of the person, organization, or system in question. The opinion given on financial statements will depend on the audit evidence obtained.

A statutory audit is a legally required review of the accuracy of a company's or government's financial statements and records. The purpose of a statutory audit is to determine whether an organization provides a fair and accurate representation of its financial position by examining information such as bank balances, bookkeeping records, and financial transactions.

Due to constraints, an audit seeks to provide only reasonable assurance that the statements are free from material error. Hence, statistical sampling is often adopted in audits. In the case of financial audits, a set of financial statements are said to be true and fair when they are free of material misstatements – a concept influenced by both quantitative (numerical) and qualitative factors. Recently, the argument that auditing should go beyond just true and fair is gaining momentum,[12] and the US Public Company Accounting Oversight Board has come out with a concept release on the same.[13]

Cost accounting is a process for verifying the cost of manufacturing or producing of any article, on the basis of accounts measuring the use of material, labor or other items of cost. The term "cost audit" refers to a systematic and accurate verification of the cost accounts and records, and checking for adherence to the cost accounting objectives. According to the Institute of Cost and Management Accountants, a cost audit is "an examination of cost accounting records and verification of facts to ascertain that the cost of the product has been arrived at, in accordance with principles of cost accounting."[citation needed]

In most nations, an audit must adhere to generally accepted standards established by governing bodies. These standards assure third parties or external users that they can rely upon the auditor's opinion on the fairness of financial statements or other subjects on which the auditor expresses an opinion. The audit must therefore be precise and accurate, containing no additional misstatements or errors.[citation needed]

Integrated audits

[edit]In the US, audits of publicly traded companies are governed by rules laid down by the Public Company Accounting Oversight Board (PCAOB), which was established by Section 404 of the Sarbanes–Oxley Act of 2002. Such an audit is called an integrated audit, where auditors, in addition to an opinion on the financial statements, must also express an opinion on the effectiveness of a company's internal control over financial reporting, in accordance with PCAOB Auditing Standard No. 5.[14]

There are also new types of integrated auditing becoming available that use unified compliance material (see the unified compliance section in Regulatory compliance). Due to the increasing number of regulations and need for operational transparency, organizations are adopting risk-based audits that can cover multiple regulations and standards from a single audit event.[citation needed] This is a very new but necessary approach in some sectors to ensure that all the necessary governance requirements can be met without duplicating effort from both audit and audit hosting resources.[citation needed]

Assessments

[edit]The purpose of an assessment is to measure something or calculate a value for it. An auditor's objective is to determine whether financial statements are presented fairly, in all material respects, and are free of material misstatement. Although the process of producing an assessment may involve an audit by an independent professional, its purpose is to provide a measurement rather than to express an opinion about the fairness of statements or quality of performance.[15]

Auditors

[edit]Auditors of financial statements & non-financial information (including compliances audit) can be classified into various categories:

- An external auditor or statutory auditor is an independent firm engaged by the client subject to the audit to express an opinion on whether the company's financial statements are free of material misstatements, whether due to fraud or error. For publicly traded companies, external auditors may also be required to express an opinion on the effectiveness of internal controls over financial reporting. External auditors may also be engaged to perform other agreed-upon procedures, related or unrelated to financial statements. Most importantly, external auditors, though engaged and paid by the company being audited, should be regarded as independent and have the status of a third party.[citation needed]

- A cost auditor or statutory cost auditor is an independent firm engaged by the client subject to the cost audit to express an opinion on whether the company's cost statements and cost sheet are free of material misstatements, whether due to fraud or error. For publicly traded companies, external auditors may also be required to express an opinion on the effectiveness of internal controls over cost reporting. These specialized auditors are called Cost Accountants in India, and globally either Cost and Management Accountants or Certified Management Accountants.

- Government auditors review the finances and practices of government bodies. In the United States, these auditors report their finds to Congress, which uses them to create and manage policies and budgets. Government auditors work for the U.S. Government Accountability Office, and most state governments have similar departments to audit state and municipal agencies.

- A secretarial auditor or statutory secretarial auditor is an independent firm engaged by a client subject to an audit of its compliance to secretarial and other applicable laws to express an opinion on whether the company's secretarial records and compliance of applicable laws are free of material misstatements, whether due to fraud or error, as these invite heavy fines or penalties. For bigger public companies, external secretarial auditors may also be required to express an opinion on the effectiveness of internal controls over the client's compliance system management. In India, these auditors are called company secretaries, and are members of the Institute of Company Secretaries of India, holding a Certificate of Practice. (http://www.icsi.edu/)

- Internal auditors are employed by the organizations they audit. They work for government agencies (federal, state and local); for publicly traded companies; and for non-profit companies across all industries. The internationally recognized standard setting body for the profession is the Institute of Internal Auditors, or IIA (www.theiia.org). The IIA has defined internal auditing as follows: "Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization's operations. It helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes".[16] Thus professional internal auditors provide independent and objective audit and consulting services focused on evaluating whether the board of directors, shareholders, stakeholders, and corporate executives have reasonable assurance that the organization's governance, risk management, and control processes are designed adequately and function effectively. Internal audit professionals (Certified Internal Auditors - CIAs) are governed by the international professional standards and code of conduct of the Institute of Internal Auditors.[17] While internal auditors are not independent of the companies that employ them, independence and objectivity are a cornerstone of the IIA professional standards, and are discussed at length in the standards and the supporting practice guides and practice advisories. Professional internal auditors are mandated by IIA standards to be independent of the business activities they audit. This independence and objectivity are achieved through the organizational placement and reporting lines of the internal audit department. Internal auditors of publicly traded companies in the United States are required to report functionally to the board of directors directly, or a sub-committee of the board of directors (typically the audit committee), and not to management except for administrative purposes. They follow standards described in the professional literature for the practice of internal auditing (such as Internal Auditor, the journal of the IIA),[18] or other similar and generally recognized frameworks for management control when evaluating an entity's governance and control practices; and apply COSO's "Enterprise Risk Management-Integrated Framework" or other similar and generally recognized frameworks for entity-wide risk management when evaluating an organization's entity-wide risk management practices. Professional internal auditors also use control self-assessment (CSA) as an effective process for performing their work.

- Consultant auditors are external personnel contracted by a client to perform an audit following the client's auditing standards. This differs from the external auditor, who follows their own auditing standards. The level of independence is therefore somewhere between the internal auditor and the external auditor. The consultant auditor may work independently, or as part of an audit team that includes internal auditors. Consultant auditors are used when the firm lacks sufficient expertise to audit certain areas, or simply for staff augmentation when staff are not available.

The most commonly used external audit standards are the US GAAS of the American Institute of Certified Public Accountants and the International Standards on Auditing (ISA) developed by the International Auditing and Assurance Standard.

Technological developments

[edit]Recent advances in artificial intelligence and automation are reshaping audit practice. Audit firms now apply data analytics and machine-learning techniques to analyze entire datasets instead of statistical samples, improving anomaly detection and efficiency. However, these technologies also introduce challenges related to data quality, algorithmic bias, and the need for professional judgment.[19][20]

Performance audits

[edit]A performance audit is an independent examination of a program, function, operation or the management systems and procedures of a governmental or non-profit entity to assess whether the entity is achieving economy, efficiency and effectiveness in the employment of available resources. Safety, security, information systems performance, and environmental concerns are increasingly the subject of audits.[21] There are now audit professionals who specialize in security audits and information systems audits. With nonprofit organizations and government agencies, there has been an increasing need for performance audits, examining their success in satisfying mission objectives.[citation needed]

Quality audits

[edit]Quality audits are performed to verify conformance to standards through reviewing objective evidence. A system of quality audits may verify the effectiveness of a quality management system. This is part of certifications such as ISO 9001. Quality audits are essential to verify the existence of objective evidence showing conformance to required processes, to assess how successfully processes have been implemented, and to judge the effectiveness of achieving any defined target levels. Quality audits are also necessary to provide evidence concerning reduction and elimination of problem areas, and they are a hands-on management tool for achieving continual improvement in an organization.

To benefit the organization, quality auditing should not only report non-conformance and corrective actions but also highlight areas of good practice and provide evidence of conformance. In this way, other departments may share information and amend their working practices as a result, also enhancing continual improvement.

Project audit

[edit]A project audit provides an opportunity to uncover issues, concerns and challenges encountered during the project lifecycle.[22] Conducted midway through the project, a project audit provides the project manager, project sponsor and project team an interim view of what has gone well, as well as what needs to be improved to successfully complete the project. If done at the close of a project, the audit can be used to develop success criteria for future projects by providing a forensic review. This review identifies which elements of the project were successfully managed and which ones presented challenges. As a result, the review will help the organization identify what it needs to do to avoid repeating the same mistakes on future projects.

Projects can undergo two types of project audits:[21]

- Regular Health Check Audits: The aim of a regular health check audit is to understand the current state of a project in order to increase project success.

- Regulatory Audits: The aim of a regulatory audit is to verify that a project is compliant with regulations and standards. The best practices of NEMEA Compliance Centre state that the regulatory audit must be accurate, objective, and independent while providing oversight and assurance to the organization.

Other forms of project audits:

Formal: Applies when the project is in trouble, and the sponsor agrees that the audit is needed, sensitivities are high, and conclusions must be proved via sustainable evidence.

Informal: Applies when a new project manager is provided, there is no indication the project is in trouble and there is a need to report whether the project is proceeding as planned. Informal audits can apply the same criteria as formal audits, but it is not necessary for the report to be so formal or in-depth.[23]

Energy audits

[edit]An energy audit is an inspection, survey and analysis of energy flows for energy conservation in a building, process or system to reduce the amount of energy input into the system without negatively affecting the output.

Operations audit

[edit]An operations audit is an examination of the operations of the client's business. In this audit, the auditor thoroughly examines the efficiency, effectiveness and economy of the operations with which the management of the client is achieving its objectives. The operational audit goes beyond internal controls issues since management does not achieve its objectives merely by compliance to a satisfactory system of internal controls. Operational audits cover any matters which may be commercially unsound. The objective of operational audit is to examine three E's, namely:[citation needed] Effectiveness – doing the right things with the least wastage of resources, Efficiency – performing work in the least possible time, and Economy – balance between benefits and costs to run the operation.[citation needed]

A control self-assessment is a commonly used tool for completing an operations audit.[24]

Forensic audits

[edit]Also referred to as forensic accountancy, forensic accountant or forensic accounting, a forensic audit is an investigative audit in which accountants specialized in both accounting and investigation seek to uncover frauds, missing money and negligence.[citation needed]

See also

[edit]- Academic audit

- Accounting

- Audit plan

- Big Four accounting firms

- Clinical audit

- Comptroller, Comptroller General, and Comptroller General of the United States

- Continuous auditing

- Cost auditing

- COSO framework, Risk management

- EarthCheck

- Financial audit, External auditor, Certified Public Accountant (CPA), and Audit risk

- Information technology audit, History of information technology auditing, and Information security audit

- Internal audit

- International Organization of Supreme Audit Institutions (INTOSAI)

- Lead auditor, under the chief audit executive or Director of audit

- Mainframe audit

- Management auditing

- Operational auditing

- Peer review

- Quality audit

- Risk-based internal audit

- Supreme audit institution

- SOFT audit

- Technical audit

References

[edit]- ^ Gupta, Kamal (November 2004). Contemporary Auditing. McGraw Hill. p. 1095. ISBN 0070585849.

- ^ "Audit assurance". Archived from the original on 2020-07-01. Retrieved 2013-05-17.

- ^ PricewaterhouseCoopers. "What is an audit?". PwC. Retrieved 2022-03-03.

- ^ Power, Michael (1999), The Audit Society: Rituals of Verification. Oxford: Oxford University Press.

- ^ Assurance, Auditing and. "Chapter 1". ICAI - The Institute of Chartered Accountants of India. Vol. 1. Institute of Chartered Accountants of India. p. 1. Archived from the original on 2020-07-01. Retrieved 2013-05-17.

- ^ Loeb, Stephen E.; Shamoo, Adil E. (1989-09-01). "Data audit: Its place in auditing". Accountability in Research. 1 (1): 23–32. doi:10.1080/08989628908573771. ISSN 0898-9621. PMID 26859053.

- ^ Derek Matthews, History of Auditing (2006-09-27). The changing audit process from the 19th century till date. Routledge-Taylor & Francis Group. p. 6. ISBN 9781134177912.

- ^ C. A., Moyer (January 1951). "Early Developments in American Auditing". Accounting Review. 26 (1): 3–8. JSTOR 239850.

- ^ Johnson, H. Thomas (1975). "Reviewed work: A History of Accounting Thought, Michael Chatfield". The Business History Review. 49 (2): 256–257. doi:10.2307/3113713. JSTOR 3113713. S2CID 154953655.

- ^ Mishra, Birendra K.; Paul Newman, D.; Stinson, Christopher H. (1997). "Environmental regulations and incentives for compliance audits". Journal of Accounting and Public Policy. 16 (2): 187–214. doi:10.1016/S0278-4254(97)00003-3. Retrieved 1 April 2023.

- ^ Thottoli, Mohammed Muneerali (2021). "The relevance of compliance audit on companies' compliance with disclosure guidelines of financial statements". Journal of Investment Compliance. 22 (2). Emerald Insight: 137–150. doi:10.1108/JOIC-12-2020-0047. S2CID 236598426. Retrieved 1 April 2023.

- ^ McKenna, Francine. "Auditors and Audit Reports: Is The Firm's "John Hancock" Enough?". Forbes. Retrieved 22 July 2011.

- ^ "CONCEPT RELEASE ON POSSIBLE REVISIONS TO PCAOB STANDARDS RELATED TO REPORTS ON AUDITED FINANCIAL STATEMENTS" (PDF). Retrieved 22 July 2011.

- ^ "Auditing Standard No. 5". pcaobus.org. Retrieved 2016-06-28.

- ^ Ladda, R.L. Basic Concepts Of Accounting. Solapur: Laxmi Book Publication. p. 58. ISBN 978-1-312-16130-6.

- ^ "Pages - Definition of Internal Auditing". Na.theiia.org. 2000-01-01. Retrieved 2013-09-02.

- ^ "Pages - International Professional Practices Framework (IPPF)". Na.theiia.org. 2000-01-01. Retrieved 2013-09-02.

- ^ "Professional internal auditors, in carrying out their responsibilities, apply COSO's Integrated Framework-Internal Control". Theiia.org.

- ^ Appelbaum, Deniz A.; Kogan, Alexander; Vasarhelyi, Miklos A. (2017). "Big Data and Analytics in the Modern Audit Engagement: Research Needs". Auditing: A Journal of Practice & Theory. 36 (4): 1–27. doi:10.2308/ajpt-51684.

- ^ "Digital Transformation & Innovation in Auditing: Insights from a Review of Academic Research". IFAC Knowledge Gateway. International Federation of Accountants. 24 August 2022. Retrieved 20 October 2025.

- ^ a b Different Types of Audits (June 2013) Auditronix Guidance Note Archived July 18, 2013, at the Wayback Machine

- ^ Stanleigh, Micheal (2009). "UNDERTAKING A SUCCESSFUL PROJECT AUDIT" (PDF). PROJECT SMART. Retrieved 18 May 2016.

{{cite web}}: CS1 maint: url-status (link) - ^ Clarke, Kevin; Walsh, Kathleen; Flanagan, Jack (21 December 2020). "How prevalent are post-completion audits in Australia". Accounting, Accountability & Performance. 18 (2): 51–78.

- ^ Gilbert W. Joseph and Terry J. Engle (December 2005). "The Use of Control Self-Assessment by Independent Auditors". The CPA Journal. Retrieved 10 March 2012.

Further reading

[edit]- Amat, O. (2008). "Earnings management and audit adjustments: An empirical study of IBEX 35 constituents". SSRN 1374232.

Audit

View on GrokipediaEtymology and Fundamentals

Etymology

The term audit derives from the Latin verb audīre, meaning "to hear," with the noun form stemming from audītus, the past participle denoting "a hearing" or "a listening."[10] [11] This origin reflects the auditory character of early financial oversight, where auditors—often royal or ecclesiastical officials—listened to verbal recitations of accounts by stewards or taxpayers, rather than reviewing written records, a practice prevalent in ancient Mesopotamia, medieval Europe, and feudal systems.[12] [13] The word entered Middle English around the early 15th century, initially as a noun for the "official examination of accounts" conducted through such oral hearings, before expanding to encompass written scrutiny and broader verification processes by the 16th century.[10] [11] In contexts like auditing a university course without credit, the term retains this "hearing" connotation, implying passive attendance and listening akin to an observer's role in early audits.[10] Over time, semantic shifts aligned audit with evidentiary inspection, but its etymological core persists in professional terminology, distinguishing it from purely visual or documentary terms like "inspection" or "review."[14]Definition and Core Principles

An audit is an independent, objective examination of an entity's financial statements, records, and related operations to verify their accuracy, completeness, and compliance with applicable financial reporting frameworks, such as Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS).[15] The primary objective is to enable the auditor to express an opinion on whether the financial statements present fairly, in all material respects, the financial position, performance, and cash flows of the entity for the period under review.[16] This process provides reasonable assurance—defined as a high but not absolute level of confidence—that the statements are free from material misstatement due to error or fraud, distinguishing audits from absolute guarantees or mere compilations.[17] External audits, typically required for public companies or under regulatory mandates, differ from internal audits by emphasizing third-party verification for stakeholders like investors and regulators.[18] Core principles guiding audits derive from international and national standards, including those from the International Auditing and Assurance Standards Board (IAASB) and the Public Company Accounting Oversight Board (PCAOB). Independence is foundational, mandating that auditors avoid any financial, familial, or business ties that could compromise impartiality, with safeguards like rotation of audit firms for public entities to mitigate familiarity threats.[19] Professional skepticism requires auditors to maintain a questioning mindset, challenging assumptions and seeking contradictory evidence rather than accepting management representations at face value, particularly in high-risk areas like revenue recognition or related-party transactions.[3] These principles ensure audits prioritize causal factors in misstatements, such as internal control weaknesses or intentional manipulation, over superficial compliance. Audits also adhere to ethical fundamentals outlined in the International Ethics Standards Board for Accountants (IESBA) Code: integrity (honesty in all professional acts), objectivity (unbiased judgment free from conflicts), professional competence and due care (applying knowledge, skill, and thoroughness updated with current standards), confidentiality (protecting information obtained unless legally required to disclose), and professional behavior (complying with laws and avoiding actions discrediting the profession).[20] Operationally, materiality focuses efforts on matters that could reasonably influence economic decisions of users, while sufficient appropriate audit evidence—gathered through inspection, observation, inquiries, and confirmations—must be relevant, reliable, and voluminous enough to support conclusions, often via substantive testing and analytical procedures.[21] A risk-based approach tailors procedures to assessed risks of material misstatement, emphasizing internal controls' design and effectiveness, as weak controls heighten reliance on detailed transaction testing.[22] Violations of these principles, such as auditor collusion in scandals like Enron (2001), have historically prompted reforms like the Sarbanes-Oxley Act of 2002, reinforcing their empirical role in maintaining market trust.[23]Historical Evolution

Ancient and Pre-Industrial Origins

The earliest auditing practices emerged in ancient Mesopotamia around 3500 BC, where cuneiform clay tablets recorded agricultural transactions, inventories, and labor efforts, with verification processes evident to reconcile records against physical assets and prevent fraud.[24] Similar systems appeared in ancient Babylon and Egypt by the 4th century BC, involving scribes who audited granary movements through physical counts, oral examinations of overseers, and cross-checks of papyrus ledgers to ensure accurate tracking of grain, taxes, and tribute.[25] These methods prioritized detection of discrepancies in state-controlled resources, reflecting a causal need for oversight in centralized economies reliant on surplus storage.[26] In the Achaemenid Persian Empire under Darius I (r. 522–486 BC), royal inspectors functioned as auditors, traveling incognito as "the King's ears" to examine provincial financial records, tax collections, and administrative compliance, thereby enforcing accountability across vast territories.[27] In classical Greece, particularly 5th–4th century BC Athens, logistai—public accountants numbering up to 30—conducted mandatory post-term audits (euthynai) of magistrates' accounts, reviewing revenues, expenditures, and public funds to identify embezzlement or errors before the Assembly.[28] Roman quaestors, from the Republic era onward, managed the aerarium (state treasury), audited provincial governors' fiscal reports, and oversaw tax farming, with detailed codices required for Senate scrutiny to curb corruption in expanding imperial finances.[26][29] Pre-industrial auditing persisted and formalized in medieval Europe, adapting ancient principles to feudal, ecclesiastical, and royal administration. From the 12th century, England's Exchequer audited sheriffs' annual accounts via pipe rolls—parchment summaries of county revenues and debts—through adversarial hearings that verified cash inflows against expected yields from royal demesnes.[30] Late medieval innovations, circa 1250–1500, integrated auditing into state-building across northwestern Europe, with procedures like cross-referenced ledgers and independent verifiers enhancing accountability in courts, monasteries, and emerging bureaucracies, though reliant on manual reconciliation prone to human error.[31] These practices emphasized stewardship over assets, driven by the need to mitigate agency problems between rulers and agents in agrarian societies lacking modern enforcement mechanisms.[32]Industrial Era Professionalization

The Industrial Revolution, commencing around 1760 in Britain, expanded business operations through factories, railways, and joint-stock companies, creating a separation between ownership and management that heightened the need for independent financial verification to safeguard investors.[33] This era's economic growth, with joint-stock company formations surging after the repeal of the Bubble Act in 1825, exposed risks of managerial fraud and accounting errors, prompting demands for specialized auditors beyond mere bookkeepers or shareholders.[25] Early auditing focused on detailed transaction vouching and balance sheet checks, but the scale of enterprises required expertise in detecting irregularities amid rapid industrialization.[34] Legislative measures advanced professionalization; the Joint Stock Companies Act of 1844 mandated the appointment of auditors for incorporated companies and required balance sheet preparation, though initial auditors were often company members lacking independence.[35] Corporate failures, such as those in the mid-19th century, underscored the limitations of non-professional oversight, leading to calls for qualified practitioners.[36] By the 1850s, auditing techniques shifted toward systematic verification, influenced by growing capital markets where shareholder protection relied on credible attestations.[37] Professional institutes emerged to establish credentials and standards; in Scotland, the Society of Accountants in Edinburgh formed in 1854, followed by similar bodies in Glasgow, marking the first organized accountancy groups with entry via examination and experience.[38] In England, regional societies proliferated in the 1870s, culminating in the Institute of Chartered Accountants in England and Wales (ICAEW) receiving its royal charter in 1880, unifying efforts to regulate membership and promote auditing proficiency.[39] These organizations emphasized independence, ethical conduct, and technical training, professionalizing auditing as a distinct occupation responsive to industrial complexities.[40] In the United States, the trend paralleled with the American Association of Public Accountants founded in 1887, reflecting transatlantic influences from British practices.[41]20th-Century Standardization

The standardization of auditing in the 20th century was driven by major financial crises, regulatory interventions, and professional initiatives to enhance reliability and consistency in financial reporting. The 1929 stock market crash and ensuing Great Depression exposed deficiencies in auditing practices, prompting U.S. legislative reforms. The Securities Act of 1933 required audited financial statements for new securities issuances, while the Securities Exchange Act of 1934 established the Securities and Exchange Commission (SEC) and mandated annual independent audits for registered companies, emphasizing auditor independence to protect investors.[42][43] These acts shifted auditing from ad hoc verification to a formalized assurance function tied to public market integrity, increasing auditor liability and demand for uniform procedures.[5] In response to ongoing scandals, such as the 1938 McKesson & Robbins fraud involving falsified inventories, the American Institute of Certified Public Accountants (AICPA) formed the Committee on Auditing Procedure (CAP) in 1939. The CAP issued Statement on Auditing Procedure (SAP) No. 1 that year, marking the first authoritative U.S. auditing standard, which required auditors to verify management assertions against generally accepted accounting principles (GAAP) and expanded testing beyond balance sheets to income statements.[5][44] Over the next three decades, the CAP produced 54 SAPs (1939–1972), addressing topics like internal controls, sampling, and confirmation procedures, which collectively formed the foundation for Generally Accepted Auditing Standards (GAAS).[45] By 1972, the AICPA codified these into 10 GAAS, divided into general standards, standards of fieldwork (e.g., planning and evidence gathering), and reporting standards, providing a structured framework for audit execution and opinions.[46] Subsequent refinements included SAP No. 27 (1957), which discouraged lengthy "long-form" reports in favor of concise opinions, and SAS No. 2 (1974), which formalized the short-form audit report structure.[5] Internationally, standardization lagged behind U.S. developments but gained momentum post-World War II amid globalization of capital markets. Professional bodies in the UK and elsewhere adopted similar principles through bodies like the Institute of Chartered Accountants in England and Wales, influencing Commonwealth practices. The pivotal global step occurred in 1977 with the founding of the International Federation of Accountants (IFAC) by 63 accountancy organizations from 51 countries, aimed at harmonizing practices.[47] IFAC's International Auditing Practices Committee (IAPC, now IAASB) began issuing International Auditing Guidelines in the 1980s, evolving into a comprehensive set of International Standards on Auditing (ISAs) by 1994, which emphasized risk-based approaches and were designed for cross-border applicability without supplanting national rules.[48][49] These efforts addressed causal gaps in pre-war auditing, such as inconsistent verification amid multinational operations, though adoption varied due to jurisdictional sovereignty. By century's end, GAAS and nascent ISAs had professionalized auditing, reducing variability but revealing limitations later exposed in events like the 1980s savings and loan crisis.[5]Post-Enron Reforms and Modern Developments

The collapse of Enron Corporation in late 2001, amid revelations of accounting fraud involving off-balance-sheet entities and auditor complicity by Arthur Andersen, prompted swift legislative action in the United States. The Sarbanes-Oxley Act (SOX), enacted on July 30, 2002, established the Public Company Accounting Oversight Board (PCAOB) as a nonprofit corporation under SEC oversight to regulate audits of public companies, replacing self-regulation by the accounting profession.[50] SOX's Title I empowered the PCAOB to develop auditing standards, conduct inspections of registered firms, and enforce compliance, addressing conflicts of interest that enabled Enron's manipulations. Key provisions included Section 404, mandating management assessment of internal controls over financial reporting with auditor attestation, and Section 302 requiring CEO and CFO certification of financial statements' accuracy.[51] Empirical studies indicate SOX enhanced audit quality by reducing earnings management and financial restatements, though at significant cost—initial compliance expenses averaged $1.5 million to $2.3 million annually for smaller firms in the early years, with benefits accruing through improved investor confidence and fewer material weaknesses in controls.[52] Auditor independence rules prohibited non-audit services and mandated lead partner rotation every five years, curbing familiarity threats observed in Enron.[51] The PCAOB's inspections, starting in 2004, identified deficiencies in 40-50% of Big Four audits initially, driving remediation and higher standards.[53] Internationally, similar reforms emerged, such as the EU's 8th Company Law Directive in 2006, emphasizing auditor oversight, though U.S. changes set a global benchmark amid skepticism of self-policing in a profession historically reliant on reputational incentives over rigorous verification.[54] In recent years, PCAOB efforts have focused on standard modernization amid technological shifts and persistent risks like cyber threats and complex transactions. In May 2024, the PCAOB adopted QC 1000, a scalable quality control standard requiring firms to design systems addressing risks such as insufficient professional skepticism, effective for audits after December 15, 2025.[55] Amendments to AS 1105 (Audit Evidence) and AS 2310 (Confirmations), approved by the SEC in August 2024, emphasize evaluating data reliability in technology-assisted environments and third-party confirmations, responding to fraud cases involving manipulated evidence; these take effect for fiscal years ending after June 15, 2025, and December 15, 2025, respectively.[56] Auditing firms increasingly integrate AI and data analytics for continuous monitoring, reducing reliance on sampling but raising challenges in validating algorithmic outputs, as evidenced by PCAOB findings of tech-related deficiencies in 2023-2024 inspections.[57] By October 2025, PCAOB guidance clarified AS 1105 implementation with examples for digital evidence, underscoring causal links between weak controls and undetected misstatements in an era of accelerated filings.[58] These evolutions prioritize substantive verification over procedural compliance, countering critiques that early SOX burdens stifled smaller issuers without proportionally advancing causal accountability.[59]Purposes and Objectives

Assurance and Verification

Assurance in auditing entails the auditor's independent evaluation to provide a high level of confidence to users that financial statements or other subject matter are free from material misstatement. Under International Standards on Auditing (ISA) 200, the objective of an audit is to obtain reasonable assurance—defined as a high, but not absolute, level of assurance—about whether financial statements as a whole are free from such misstatements, whether caused by fraud or error.[60] This reasonable assurance is expressed through an audit opinion, which enhances user confidence in the entity's reported financial position, performance, and cash flows, distinguishing it from absolute assurance due to factors like sampling methods, inherent limitations in evidence gathering, and potential management override of controls.[61][22] Verification forms the evidentiary foundation for achieving assurance, encompassing substantive procedures to corroborate management's assertions on financial statement elements, including existence, rights and obligations, completeness, accuracy, valuation, and presentation. Auditors verify assets and liabilities through techniques such as external confirmations from third parties for receivables and payables, physical observation for inventory and fixed assets, and vouching transactions back to original documents like invoices and contracts.[62][63] These procedures, guided by standards like ISA 500 on audit evidence, aim to gather sufficient and appropriate evidence to mitigate detection risk, ensuring the audit opinion is supported by verifiable facts rather than mere representation.[64] In practice, assurance and verification intersect to address audit risk—the risk of failing to detect material misstatement—through a risk-based approach where higher-risk areas receive more rigorous verification. For instance, in financial audits under U.S. Generally Accepted Auditing Standards (GAAS), verification includes analytical procedures to identify unusual fluctuations and substantive testing scaled by assessed control effectiveness.[46] This framework, while providing reasonable assurance, acknowledges residual risks, as evidenced by historical audit failures where undetected fraud occurred despite verification efforts, underscoring the need for professional skepticism.[65]Risk Mitigation and Compliance

Audits serve to identify, assess, and mitigate organizational risks by systematically evaluating internal controls, processes, and vulnerabilities that could lead to financial losses, operational disruptions, or fraudulent activities. External and internal auditors apply risk-based approaches, prioritizing high-impact areas such as material misstatements or control weaknesses, which empirical studies indicate can reduce fraud incidence through proactive detection mechanisms like the fraud triangle analysis—involving pressure, opportunity, and rationalization factors.[66][67] For instance, internal audits contribute to enterprise-wide risk management by providing assurance on the effectiveness of risk mitigation strategies, including testing controls over financial reporting and operational integrity.[68] In compliance contexts, audits verify adherence to legal, regulatory, and internal policy requirements, thereby averting penalties, reputational damage, and litigation. Compliance audits specifically scrutinize whether operations align with standards like anti-money laundering rules or environmental regulations, identifying gaps that could expose entities to enforcement actions; for example, they mitigate risks by flagging non-compliance early, as evidenced in frameworks where audits integrate with governance to enforce accountability.[69][70] The Sarbanes-Oxley Act of 2002 (SOX) exemplifies this in the U.S., mandating public companies to establish and audit internal controls over financial reporting (Section 404), with auditors attesting to their design and operating effectiveness, which has demonstrably enhanced reporting accuracy and reduced material weaknesses reported in subsequent years.[71][72] Risk mitigation extends beyond detection to recommending remedial actions, such as strengthening segregation of duties or implementing automated monitoring tools, which studies show lower fraud risks in risk-based auditing environments.[73] Internal auditors often lead SOX compliance efforts, coordinating with management to remediate deficiencies, as a 2019 analysis found over half of companies assigning this responsibility to internal audit functions for integrated oversight. Overall, these audit functions foster a culture of accountability, with evidence from internal audit practices linking them to decreased fraud occurrences through continuous monitoring and control enhancements.[74]Value-Added Insights

Value-added insights in auditing refer to the strategic recommendations, operational enhancements, and forward-looking analyses derived from audit processes that enable organizations to improve efficiency, optimize resource allocation, and achieve long-term objectives beyond basic compliance verification. These insights arise primarily from internal audits, where professionals apply risk-based methodologies to identify inefficiencies, such as redundant processes or control gaps, leading to measurable cost reductions; for instance, a 2022 survey of internal audit functions identified independence, auditor competence, and alignment with organizational goals as key factors correlating with enhanced value delivery, including average annual savings of 5-10% in operational costs for participating firms.[75] External audits contribute more limited value-added elements, constrained by independence requirements under standards like those from the Public Company Accounting Oversight Board (PCAOB), but can highlight systemic risks in financial reporting that inform management decisions.[53] Advanced technologies amplify these insights by enabling data-driven foresight, such as continuous auditing systems that detect anomalies in real-time, reducing fraud losses by up to 50% in implemented cases according to empirical analyses of enterprise implementations.[76] Auditors leveraging whole-ledger analytics, for example, uncover patterns in transaction data that reveal supply chain vulnerabilities or pricing inefficiencies, providing clients with actionable strategies that boost profitability; a 2024 report documented instances where such techniques identified strategic opportunities yielding 15-20% improvements in working capital management. The Institute of Internal Auditors (IIA) emphasizes this role in its Global Internal Audit Standards, effective January 2025, mandating that audits demonstrate purpose through value-adding activities like advisory services on governance and risk, evaluated via key performance indicators such as recommendation adoption rates exceeding 80% in high-performing functions.[77] Empirical studies underscore the causal link between robust audit practices and tangible benefits, with internal audit effectiveness tied to factors like auditor experience and client collaboration, resulting in higher adoption of value-added services; one analysis of audit-client relationships found that committed partnerships increased provision of such services by 25-30%, enhancing overall audit survival and client retention.[78] However, realization of these insights requires overcoming barriers like management resistance or resource constraints, as evidenced by literature reviews showing that only functions with systematic programs and board support consistently deliver superior outcomes, such as improved transparency and reduced regulatory penalties.[79] In practice, value-added auditing prioritizes alignment with business strategy, using techniques like benchmarking against industry peers to recommend innovations, thereby fostering resilience against economic disruptions.[80]Standards and Regulatory Frameworks

International Auditing Standards

The International Standards on Auditing (ISAs) are a set of professional standards for the performance of audits of historical financial information, developed to promote consistency, quality, and transparency in auditing practices worldwide.[81] They are issued by the International Auditing and Assurance Standards Board (IAASB), an independent standard-setting body operating under the auspices of the International Federation of Accountants (IFAC).[82] The IAASB's objective is to serve the public interest by establishing high-quality auditing, assurance, and related services standards that enhance the credibility of financial reporting.[81] Established in March 1978 as the International Auditing Practices Committee (IAPC), the IAASB rebranded in 2002 and has since issued over 40 ISAs, with a major clarification and redrafting completed in 2009 to improve clarity and applicability.[82] [83] ISAs are principles-based, emphasizing professional skepticism, risk assessment, and sufficient appropriate audit evidence, and are structured into sections covering auditor responsibilities (e.g., ISA 200), planning (ISA 300), internal control (ISA 315), and fraud considerations (ISA 240).[81] They apply primarily to audits of general-purpose financial statements but have been adapted for specialized contexts, such as less complex entities via ISA for LCE issued in December 2023.[84] As of 2024, approximately 130 jurisdictions have adopted or committed to adopting ISAs, representing over 90% of IFAC member bodies, though full convergence varies due to national modifications or "carve-outs" in areas like auditor liability or specific reporting requirements.[85] [86] Empirical evidence indicates that ISA adoption correlates with improved financial reporting quality and reduced earnings management, as jurisdictions implementing ISAs exhibit lower discretionary accruals compared to non-adopters.[87] Recent developments include revisions to enhance auditor responsiveness to emerging risks. In July 2025, ISA 240 (Revised) was updated to strengthen fraud detection by mandating a "fraud lens" in risk assessments and requiring explicit documentation of fraud-related inquiries, effective for periods beginning on or after December 15, 2026.[88] Similarly, ISA 570 (Revised 2024) on going concern was revised in May 2025 to expand auditor evaluations of management's assessments amid economic uncertainties, with the same effective date.[89] The IAASB's 2025 Handbook, released in September 2025, incorporates these updates alongside guidance on technology integration, reflecting a September 2024 position paper on adapting standards to audit-assurance intersections with AI and data analytics.[90] [91] These enhancements aim to address stakeholder demands for greater transparency without compromising audit efficiency, though implementation challenges persist in jurisdictions with resource-constrained regulators.[92]National and Sector-Specific Regulations

In the United States, the Sarbanes-Oxley Act (SOX) of 2002 established the Public Company Accounting Oversight Board (PCAOB) to oversee audits of public companies, mandating registration of audit firms, inspection of audits, and enforcement of auditing standards to enhance financial reporting integrity following corporate scandals.[93] SOX Section 404 requires management and auditors to assess and report on internal controls over financial reporting, with PCAOB standards applying to audits for fiscal years beginning after December 15, 2024, including requirements for internal control audits under AS 2201.[94] The Securities and Exchange Commission (SEC) provides oversight of the PCAOB, ensuring compliance with these federal requirements for publicly traded entities.[95] In the European Union, Directive 2006/43/EC governs statutory audits of annual and consolidated accounts, requiring audits to be conducted in accordance with international standards while promoting auditor independence and transparency for public-interest entities.[96] This was amended by Directive 2014/56/EU to strengthen audit firm rotation, non-audit service restrictions, and joint audits for large entities, aiming to mitigate risks of long-term auditor-client relationships.[97] Member states transpose these into national law, with oversight by bodies ensuring cross-border audit equivalence.[98] The United Kingdom's Companies Act 2006, as amended, mandates audits for companies exceeding certain thresholds and empowers the Financial Reporting Council (FRC) to set auditing standards and supervise audit firms under Part 42.[99] The Statutory Auditors and Third Country Auditors Regulations 2016 (as updated in 2022) regulate auditor registration, inspections, and third-country equivalence, with the FRC enforcing ethical and quality standards for public interest audits.[100] Post-Brexit, these align partially with EU rules but emphasize domestic oversight to maintain audit reliability.[101] In banking, the Basel Committee on Banking Supervision's principles require internal audit functions to cover all bank activities, including outsourced ones, with direct reporting to the board or audit committee to ensure comprehensive risk assessment and control evaluation.[102] External audits must align with Basel Core Principles (revised 2024), where supervisors expect tailored procedures beyond general standards to address sector-specific risks like credit and liquidity exposures.[103] These apply globally to strengthen prudential regulation under Basel III frameworks.[104] Healthcare regulations emphasize data security audits; the U.S. HIPAA Security Rule (updated through 2024) mandates covered entities to implement audit controls for electronic protected health information, including logging access and changes to detect breaches.[105] The Office for Civil Rights conducts periodic HIPAA audits to verify compliance, focusing on risks like hacking vulnerabilities.[106] Publicly traded healthcare firms additionally face SOX internal control audits overlapping with HIPAA, requiring integrated assessments of financial and privacy safeguards.[107] In the energy sector, the U.S. Federal Energy Regulatory Commission (FERC) performs risk-based audits of regulated entities like pipelines and utilities to verify compliance with interstate commerce and reliability standards, including financial and operational reporting.[108] Environmental audits, such as those under India's Environment (Protection) Act 1986 rules (updated 2025), require accredited auditors to assess high-impact industries for pollution control and waste management, with mandatory periodic reporting to enforce sustainability compliance.[109] These sector mandates prioritize verifiable environmental and operational data over general financial audits.[110]Recent Revisions (2024-2025)

In 2024, the U.S. Government Accountability Office (GAO) issued a comprehensive revision to the Government Auditing Standards, commonly known as the Yellow Book, effective for financial audits, attestation engagements, and reviews of financial statements for periods beginning on or after December 15, 2024.[111] This update emphasizes a shift to quality management systems over traditional quality control, requiring audit organizations to design, implement, and monitor processes tailored to their size and risks, including enhanced focus on independence threats and auditor competence in areas like data analytics and fraud detection.[112] The revisions also introduce stricter peer review requirements and expanded documentation for independence impairments, aiming to address evolving governmental auditing challenges amid increasing regulatory scrutiny.[113] The Public Company Accounting Oversight Board (PCAOB) adopted AS 1000, General Responsibilities of the Auditor, on May 13, 2024, establishing foundational obligations for auditors in conducting audits of public companies, including due professional care, professional skepticism, and objectivity.[114] Approved by the SEC on August 20, 2024, this standard, along with conforming amendments to existing rules, applies to audits for fiscal years beginning on or after December 15, 2024, and seeks to clarify auditor duties in response to inspection findings on deficiencies in audit execution.[56] Additionally, PCAOB amendments to standards on Technology-Assisted Analysis (TAA), effective for fiscal years beginning on or after December 15, 2025, update AS 1105 and AS 2301 to incorporate procedures for auditing data in electronic form, reflecting the growing reliance on digital evidence and AI tools.[115] Confirmations standard amendments, effective for fiscal years ending on or after June 15, 2025, strengthen requirements for external confirmations to mitigate fraud risks in cash and receivables testing.[57] The PCAOB's Quality Control Standard (QC 1000), delayed to December 15, 2025, mandates scalable, risk-based quality management systems for firms.[57] On the international front, the International Auditing and Assurance Standards Board (IAASB) approved ISA 570 (Revised 2024), Going Concern, in December 2024, effective for audits of financial statements for periods beginning on or after December 15, 2026, with enhancements to risk assessment and disclosure requirements amid economic volatility.[116] In September 2024, the IAASB finalized ISSA 5000, the first global standard for sustainability assurance engagements, addressing non-financial reporting demands driven by ESG regulations.[117] The Institute of Internal Auditors released mandatory Global Internal Audit Standards in January 2024, restructuring guidance into core principles, implementation, and performance domains to improve internal audit effectiveness.[77] In the U.S. non-issuer space, the AICPA Auditing Standards Board advanced quality management standards in 2025, transitioning firms to risk-responsive systems effective for periods beginning on or after June 15, 2025, with proposals for a new standalone fraud standard under consideration to explicitly address fraud responsibilities beyond existing SAS requirements.[118][119] These revisions collectively respond to technological advancements, fraud prevalence, and stakeholder demands for robust assurance, though implementation challenges include resource strains on smaller firms.[120]Types of Audits

Financial Audits

A financial audit constitutes an independent examination of an entity's financial statements, aimed at providing reasonable assurance that they are free from material misstatement, whether resulting from error or fraud, and are presented fairly in accordance with the applicable financial reporting framework, such as U.S. GAAP or IFRS.[121][16] This process verifies the accuracy, completeness, and compliance of reported financial position, results of operations, and cash flows, typically covering the balance sheet, income statement, statement of changes in equity, and statement of cash flows.[22] External auditors, often certified public accountants adhering to standards like those from the PCAOB for U.S. public companies or AICPA Statements on Auditing Standards for nonissuers, conduct these audits to mitigate risks of undetected errors or intentional manipulations that could mislead investors or creditors.[122][123] The primary objective distinguishes financial audits from other audit types: it focuses on historical financial data and attestation of fair presentation, rather than operational efficiency, regulatory compliance beyond financial reporting, or future-oriented performance metrics.[124] Unlike internal audits, which are conducted by organization employees to enhance internal controls and processes for management use, financial audits deliver an independent opinion for external stakeholders, such as shareholders and regulators.[125] For publicly traded companies, Section 404 of the Sarbanes-Oxley Act of 2002 mandates integration with audits of internal controls over financial reporting, ensuring reliability against material weaknesses identified in scandals like Enron, where inadequate controls led to $74 billion in shareholder losses by 2001.[126] Auditors apply a risk-based approach, assessing materiality thresholds—often set at 5% of net income or 1% of total assets—and performing substantive tests on high-risk areas like revenue recognition or inventory valuation through vouching, confirmations, and analytical procedures.[122] Sampling techniques, such as statistical or non-statistical methods, evaluate transaction populations without full verification, with error projections determining if misstatements exceed tolerable levels.[127] The culminating audit report issues one of four opinions: unmodified (clean), qualified (material issues in specific areas), adverse (pervasive misstatements), or disclaimer (insufficient evidence), influencing credit ratings and investment decisions; for instance, qualified opinions correlate with average stock price drops of 2-5% upon issuance.[22][128] International Standards on Auditing (ISAs), issued by the IAASB under IFAC, harmonize practices globally, requiring auditors to obtain sufficient appropriate audit evidence and communicate key audit matters in reports for listed entities since ISA 701's effective date of December 15, 2016. In jurisdictions like the EU, audits under the Statutory Audit Directive emphasize skepticism toward management estimates, reducing instances of over-optimistic provisioning seen in the 2008 financial crisis, where banks like Lehman Brothers reported overstated assets leading to its September 15, 2008, bankruptcy.[16] These audits enhance capital market integrity by deterring fraud, with PCAOB inspections revealing that 40% of inspected firms had deficiencies in revenue testing as of 2023 reports.[126]Compliance and Internal Audits

Compliance audits systematically assess an organization's adherence to external regulations, laws, internal policies, and industry standards to mitigate legal, financial, and reputational risks. These audits involve reviewing documentation, processes, and controls to confirm alignment with specific frameworks, such as the Sarbanes-Oxley Act (SOX) of 2002, which requires public companies to maintain effective internal controls over financial reporting and mandates Section 404 attestation by management and external auditors.[129][130] Other key examples include the Health Insurance Portability and Accountability Act (HIPAA) for protecting health information in the U.S., the General Data Protection Regulation (GDPR) for data privacy in the European Union, and the Payment Card Industry Data Security Standard (PCI-DSS) for securing cardholder data.[129][131] Non-compliance can result in penalties, as evidenced by fines exceeding $1 billion imposed under GDPR in its first few years of enforcement for violations like inadequate data processing consents.[131] Internal audits, by contrast, constitute an independent and objective assurance activity conducted within the organization to evaluate and enhance the effectiveness of risk management, control, and governance processes. According to the Institute of Internal Auditors (IIA), internal auditing adds value by providing recommendations for operational improvements, distinct from the narrower regulatory focus of pure compliance audits.[132] The IIA's Global Internal Audit Standards, effective January 2025 following revisions in 2024, emphasize principles like integrity, objectivity, and proficiency, with new requirements addressing data privacy risks and ethical information handling amid rising cyber threats.[77][133] Internal audits often encompass compliance elements—such as testing controls under frameworks like the Committee of Sponsoring Organizations (COSO)—but extend to broader operational efficiencies, with auditors sampling processes to identify inefficiencies or fraud risks before external scrutiny arises.[134] While compliance audits prioritize verifiable adherence to predefined rules, often with exhaustive sampling of transactions for high-stakes regulations like SOX, internal audits adopt a risk-based approach with potentially smaller but more analytically driven samples to inform strategic decisions.[135] This distinction arises from their scopes: compliance audits serve primarily as regulatory checkpoints, potentially triggered by government mandates or certifications, whereas internal audits function proactively to support management in preempting issues, though both rely on evidence like logs, records, and interviews.[136] Overlap occurs when internal audit teams incorporate compliance testing, as permitted under IIA guidance, enabling integrated assessments that avoid redundant efforts while ensuring holistic risk coverage.[137] In practice, organizations like financial institutions under Dodd-Frank Act oversight integrate these to balance regulatory demands with internal resilience, reducing the incidence of violations reported to bodies like the U.S. Securities and Exchange Commission.[130]Performance and Operational Audits

Performance audits involve an independent examination of a government or public sector entity's programs, functions, or operations to assess whether they achieve intended objectives through economy, efficiency, and effectiveness, often referred to as the "3Es."[138] These audits provide findings or conclusions based on sufficient, appropriate evidence evaluated against predefined criteria, such as legal requirements or best practices.[112] In the United States, performance audits are governed by the Government Accountability Office's (GAO) Generally Accepted Government Auditing Standards (GAGAS), outlined in the 2024 Yellow Book revision, which mandates compliance with general standards for independence, competence, and due care; field work standards for planning, evidence gathering, and supervision; and reporting standards for clear communication of results.[112] Operational audits, by contrast, focus on evaluating the efficiency and effectiveness of an organization's internal processes, systems, and resource utilization in the private or corporate sector, aiming to identify opportunities for cost savings and operational improvements without primary emphasis on financial statement accuracy.[139] While performance audits typically prioritize public sector value-for-money outcomes and program accountability, operational audits emphasize broader business workflow optimization, such as inventory management or supply chain processes, though the terms overlap and are sometimes used interchangeably— with "performance" more common in government contexts and "operational" in commercial ones.[140] For instance, a 2023 operational audit of CV. X, an Indonesian company, revealed inefficiencies in inventory controls leading to excess stock and tied-up capital, recommending streamlined procedures that reduced holding costs by an estimated 15-20% post-implementation.[141] Both types employ systematic methodologies, including risk-based planning to select audit scope, data analysis, interviews, and benchmarking against industry standards to test operational controls and outcomes.[142] In government settings, performance audits have driven measurable efficiencies; for example, a 2022 New Jersey state comptroller audit of public programs identified redundant contracting processes, resulting in projected annual savings of $10 million through consolidated procurement.[143] Similarly, operational audits in business contexts, such as a global bank's adoption of integrated audit software in 2023, shifted auditor focus from administrative tasks to analytical reviews, enhancing risk detection and operational throughput by 25%.[144] These audits underscore causal links between process flaws— like inadequate internal controls or misaligned incentives— and suboptimal performance, prioritizing empirical evidence over anecdotal assessments to recommend actionable reforms.[142]Specialized Audits

Specialized audits encompass targeted examinations designed for particular industries, risks, or objectives, distinct from routine financial or operational reviews, often requiring expertise in niche domains such as fraud detection, technology systems, or environmental impacts. These audits address specific regulatory, legal, or business needs, employing customized methodologies to evaluate compliance, efficiency, or irregularities in focused areas. For instance, they may investigate allegations of misconduct or assess adherence to sector-specific standards, providing evidence for litigation, policy adjustments, or risk mitigation.[145] Forensic audits constitute a prominent category, involving detailed scrutiny of financial records to uncover evidence of fraud, embezzlement, or irregularities suitable for legal proceedings. Conducted by accountants with investigative training, these audits go beyond standard verification by reconstructing transactions, tracing asset flows, and identifying intentional misstatements, often prompted by whistleblower reports, disputes, or regulatory inquiries. The purpose centers on producing court-admissible findings, such as quantifying losses from fraudulent activities, with techniques including data analytics, interviews, and document authentication.[146][147] Information technology (IT) audits evaluate the security, integrity, and effectiveness of an organization's information systems, encompassing hardware, software, networks, and data management practices. Key types include systems and applications audits, which test controls for vulnerabilities; compliance audits verifying alignment with frameworks like ISO/IEC 27001 for information security management or SOC 2 for service organizations; and operational IT audits assessing efficiency in areas such as data processing facilities or enterprise architecture. These audits mitigate risks like cyberattacks or data breaches, with standards emphasizing risk-based approaches and continuous monitoring.[148][149] Environmental audits systematically assess an organization's environmental performance, compliance with regulations, and management systems to identify impacts from operations, such as waste generation, emissions, or resource use. They typically involve site inspections, record reviews, and gap analyses against standards like ISO 14001, revealing non-compliance risks or opportunities for sustainability improvements. Common in industries like manufacturing or energy, these audits support regulatory filings, liability avoidance, and voluntary reporting, with findings often driving corrective actions like pollution controls.[150][151] Other specialized forms include construction audits, which review project costs, contracts, and change orders for overruns or disputes; royalty audits, verifying payments in licensing agreements for industries like media or pharmaceuticals; and tax-specific audits focusing on niche areas such as sales and use tax accuracy or transfer pricing compliance. These engagements demand interdisciplinary knowledge, often integrating legal, technical, or scientific expertise to deliver precise, actionable insights.[152][153]Audit Execution Process

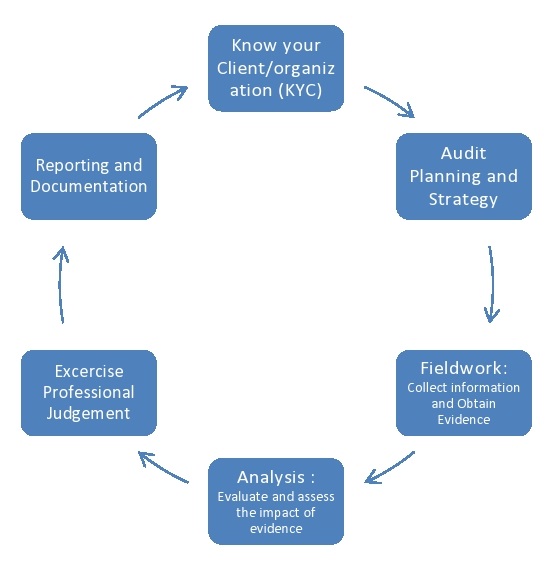

Planning and Risk Assessment

Planning an audit engagement begins with preliminary activities to evaluate the auditor's ability to accept or continue the client relationship, including assessing independence, competence, and resources required.[154] These steps ensure the audit team can perform procedures necessary to reduce audit risk to an acceptably low level, as outlined in PCAOB AS 2101, which mandates establishing an overall audit strategy encompassing the scope, timing, and direction of efforts.[154] Internationally, ISA 300 similarly requires auditors to plan the audit to perform it effectively, involving coordination among engagement team members and consideration of prior audits or related services.[155] Central to planning is obtaining an understanding of the entity and its environment, including its internal control system, to identify risks of material misstatement in the financial statements.[156] Under ISA 315 (Revised 2019), auditors must assess these risks at both the financial statement level and the assertion level for classes of transactions, account balances, and disclosures, distinguishing between those due to error and those due to fraud.[156] This process incorporates inquiries of management, analytical procedures, and observation of operations, with heightened focus on areas like revenue recognition or complex estimates where inherent risks are elevated.[157] PCAOB standards align by requiring evaluation of fraud risks and control environment effectiveness early in planning to inform the audit plan's nature, timing, and extent.[154] Materiality determination guides risk assessment thresholds, typically set as a percentage of benchmarks like net income or total assets—often 5-10% for overall materiality in practice—adjusted for qualitative factors such as regulatory scrutiny or stakeholder expectations.[158] Risk responses are then tailored: higher risks prompt more substantive testing or tests of controls, while planning also addresses staffing, technology use, and specialist involvement to address entity-specific complexities like multinational operations.[154] Documentation of the plan records these decisions, serving as a basis for supervision and review, with the process being dynamic to incorporate new information throughout the engagement.[158]Evidence Collection and Testing

Audit evidence collection and testing constitutes the core execution phase following planning and risk assessment, wherein auditors apply procedures to obtain sufficient appropriate evidence supporting their conclusions on financial statements or other audit objectives. Sufficient evidence refers to the quantity needed to reduce audit risk to an acceptably low level, while appropriate evidence encompasses relevance to the assertion under review and reliability based on source, nature, and circumstances of generation.[159] Procedures are designed responsively to assessed risks of material misstatement, prioritizing higher-risk areas, and may include both tests of controls—where reliance on internal controls is planned—and substantive procedures applied universally to detect misstatements.[159] Tests of controls assess the operating effectiveness of entity controls intended to prevent or detect material misstatements, performed only when the auditor plans to rely on those controls to modify substantive testing extent. Common methods include inquiry of personnel, observation of control activities, inspection of documents evidencing control execution, and reperformance of controls to verify independent operation. For instance, reperformance might involve the auditor independently authorizing a sample of transactions to confirm segregation of duties. If controls prove ineffective, the auditor expands substantive procedures accordingly. These tests typically employ sampling techniques, such as statistical or non-statistical methods, to infer population-wide effectiveness, with sample sizes determined by expected deviation rates and tolerable rates.[159] Substantive procedures provide direct evidence on assertions like existence, completeness, accuracy, and valuation, comprising tests of details and substantive analytical procedures. Tests of details involve vouching source documents to records (e.g., tracing invoices to ledger entries), confirming balances externally (e.g., third-party verifications of receivables), recalculating amounts, and inspecting tangible assets. Substantive analytical procedures entail evaluating financial information by studying plausible relationships, such as ratio analysis or trend comparisons, with expectations developed from prior periods, industry data, or entity budgets; significant unexpected variances prompt further investigation. These procedures often use sampling, where auditors select items based on risk, monetary value, or judgment, ensuring representation of the population.[159][160] Reliability of evidence varies by type: external confirmations from independent sources generally provide higher reliability than internal documents, while originals exceed photocopies, and auditor-generated evidence through reperformance or observation surpasses entity-provided data. Auditors consider factors like source expertise, contradictions with other evidence, and timeliness, often corroborating lower-reliability evidence with multiple sources. In performance or operational audits, evidence collection adapts to non-financial objectives, incorporating site visits, interviews, and benchmarking against standards, though financial audits emphasize quantitative verification. Documentation in working papers records procedures, evidence obtained, and conclusions, enabling review and supporting defense against challenges.[159] Emerging practices incorporate technology, such as data analytics for continuous testing and automated confirmations, enhancing efficiency but requiring validation of tool reliability. For example, auditors may use generalized audit software to analyze entire populations rather than samples, identifying anomalies via algorithms. Challenges include management override risks, addressed through unpredictable procedures, and remote evidence gathering post-2020, which demands enhanced verification protocols. Overall, the phase culminates in evaluating whether accumulated evidence supports or contradicts assertions, informing subsequent reporting.[159]Reporting, Opinions, and Follow-Up