Community hub

Recent from talks

Contribute something

Nothing was collected or created yet.

Proprietary software

View on Wikipedia

Proprietary software is software that grants its creator, publisher, or other rightsholder or rightsholder partner a legal monopoly by modern copyright and intellectual property law to exclude the recipient from freely sharing the software or modifying it, and—in some cases, as is the case with some patent-encumbered and EULA-bound software—from making use of the software on their own, thereby restricting their freedoms.[1]

Proprietary software is a subset of non-free software, a term defined in contrast to free and open-source software; non-commercial licenses such as CC BY-NC are not deemed proprietary, but are non-free. Proprietary software may either be closed-source software or source-available software.[1][2]

Origin

[edit]Until the late 1960s, computers—especially large and expensive mainframe computers, machines in specially air-conditioned computer rooms—were usually leased to customers rather than sold.[3][4] Service and all software available were usually supplied by manufacturers without separate charge until 1969. Computer vendors usually provided the source code for installed software to customers.[citation needed] Customers who developed software often made it available to the public without charge.[5] Closed source means computer programs whose source code is not published except to licensees. It is available to be modified only by the organization that developed it and those licensed to use the software.

In 1969, IBM, which had antitrust lawsuits pending against it, led an industry change by starting to charge separately for mainframe software[6][7] and services, by unbundling hardware and software.[8]

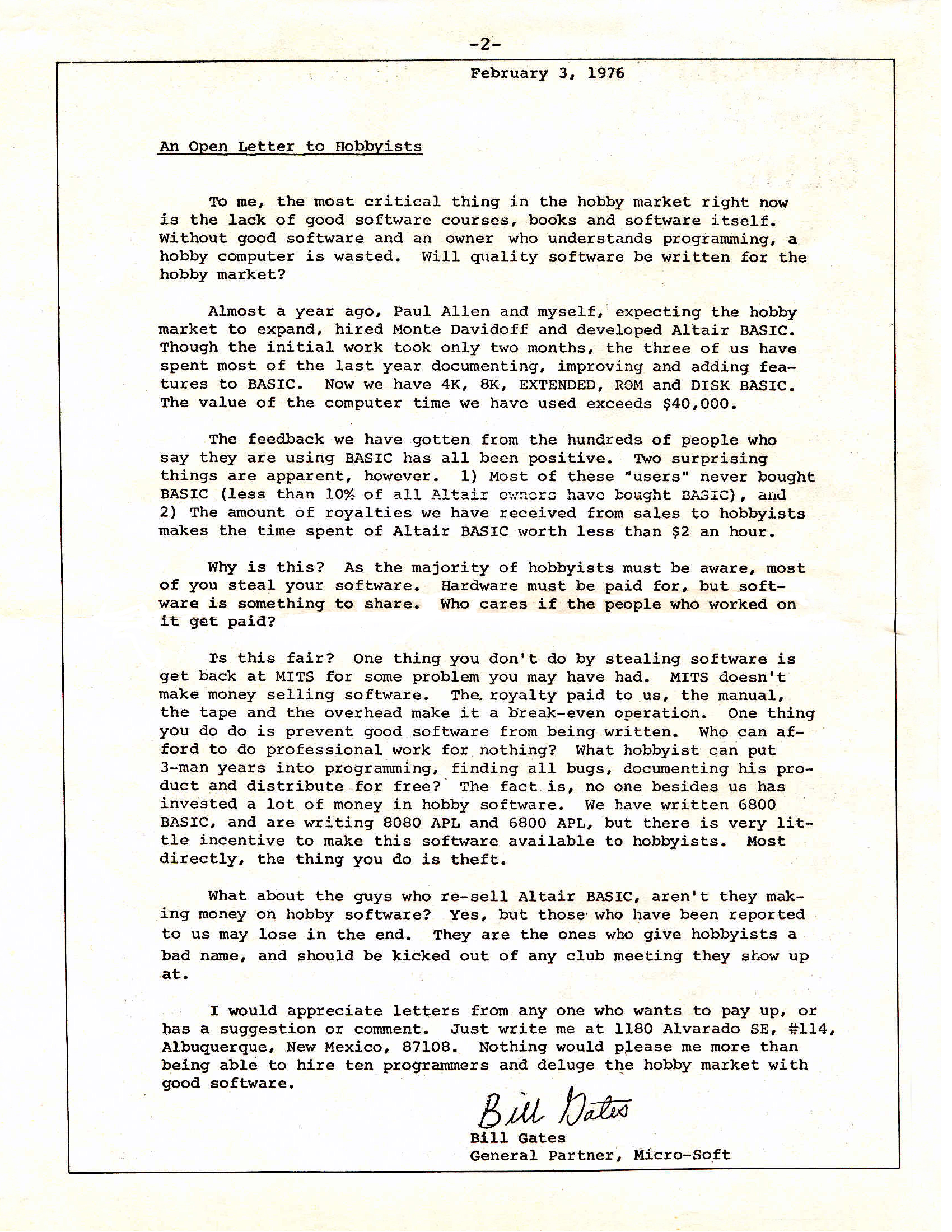

Bill Gates' "Open Letter to Hobbyists" in 1976 decried computer hobbyists' rampant copyright infringement of software, particularly Microsoft's Altair BASIC interpreter, and asserted that their unauthorized use hindered his ability to produce quality software. But the legal status of software copyright, especially for object code, was not clear until the 1983 appeals court ruling in Apple Computer, Inc. v. Franklin Computer Corp.[9][10][11]

According to Brewster Kahle the legal characteristic of software changed also due to the U.S. Copyright Act of 1976.[12] The Commission on New Technological Uses of Copyrighted Works concluded in 1978 with the recommendations that became the Computer Software Copyright Act of 1980.[13]

Starting in February 1983 IBM adopted an "object-code-only" model for a growing list of their software and stopped shipping much of the source code,[14][15] even to licensees.

In 1983, binary software became copyrightable in the United States as well by the Apple vs. Franklin law decision,[16] before which only source code was copyrightable.[17] Additionally, the growing availability of millions of computers based on the same microprocessor architecture created for the first time an unfragmented and big enough market for binary distributed software.[17]

Examples of proprietary operating system include Microsoft Windows, Classic Mac OS, macOS, iOS and iPadOS.[18]

Types

[edit]| Free/Open Licenses | Non-free Licenses | |||||

|---|---|---|---|---|---|---|

| Public domain & equivalents | Permissive license | Copyleft (protective license) | Noncommercial license | Proprietary license | Trade secret | |

| Software | PD, CC0 | BSD, MIT, Apache | GPL, AGPL | JRL, AFPL | proprietary software, no public license | private, internal software |

| Other creative works | PD, CC0 | CC BY | CC BY-SA | CC BY-NC | Copyright, no public license | unpublished |

Licenses

[edit].jpg)

The tendency to license proprietary software, rather than sell it, dates from the time period before the existence, then the scope of software copyright protection was clear. These licenses have continued in use after software copyright was recognized in the courts, and are considered to grant the company extra protection compared to copyright law.[19] According to United States federal law, a company can restrict the parties to which it sells but it cannot prevent a buyer from reselling the product. Software licensing agreements usually prohibit resale, enabling the company to maximize revenue.[20]

Traditionally, software was distributed in the form of binary object code that could not be understood or modified by the user,[21] but could be downloaded and run. The user bought a perpetual license to use a particular version of the software.[22] Software as service (SaaS) vendors—who have the majority market share in application software as of 2023[update][23]—rarely offer perpetual licenses.[24] SaaS licenses are usually temporary and charged on a pay-per-usage or subscription basis,[25] although other revenue models such as freemium are also used.[26] For customers, the advantages of temporary licenses include reduced upfront cost, increased flexibility, and lower overall cost compared to a perpetual license.[22] In some cases, the steep one-time cost demanded by sellers of traditional software were out of the reach of smaller businesses, but pay-per-use SaaS models makes the software affordable.[27]Mixed-source software

[edit]Software distributions considered as proprietary may in fact incorporate a "mixed source" model including both free and non-free software in the same distribution.[28] Most if not all so-called proprietary UNIX distributions are mixed source software, bundling open-source components like BIND, Sendmail, X Window System, DHCP, and others along with a purely proprietary kernel and system utilities.[29][30]

Multi-licensing

[edit]Some free software packages are also simultaneously available under proprietary terms. Examples include MySQL, Sendmail and ssh. The original copyright holders for a work of free software, even copyleft free software, can use dual-licensing to allow themselves or others to redistribute proprietary versions. Non-copyleft free software (i.e. software distributed under a permissive free software license or released to the public domain) allows anyone to make proprietary redistributions.[31][32] Free software that depends on proprietary software is considered "trapped" by the Free Software Foundation. This includes software written only for Microsoft Windows,[33] or software that could only run on Java, before it became free software.[34]

Legal basis

[edit]Most of the software is covered by copyright which, along with contract law, patents, and trade secrets, provides legal basis for its owner to establish exclusive rights.[35]

A software vendor delineates the specific terms of use in an end-user license agreement (EULA). The user may agree to this contract in writing, interactively on screen (clickwrap), or by opening the box containing the software (shrink wrap licensing). License agreements are usually not negotiable.[36] Software patents grant exclusive rights to algorithms, software features, or other patentable subject matter, with coverage varying by jurisdiction. Vendors sometimes grant patent rights to the user in the license agreement.[37] The source code for a piece of proprietary software is routinely handled as a trade secret.[38] Software can be made available with fewer restrictions on licensing or source-code access; software that satisfies certain conditions of freedom and openness is known as "free" or "open-source."[39]

Limitations

[edit]Since license agreements do not override applicable copyright law or contract law, provisions in conflict with applicable law are not enforceable.[40] Some software is specifically licensed and not sold, in order to avoid limitations of copyright such as the first-sale doctrine.[41]

Exclusive rights

[edit]The owner of proprietary software exercises certain exclusive rights over the software. The owner can restrict the use, inspection of source code, modification of source code, and redistribution.

Use of the software

[edit]Vendors typically limit the number of computers on which software can be used, and prohibit the user from installing the software on extra computers.[citation needed] Restricted use is sometimes enforced through a technical measure, such as product activation, a product key or serial number, a hardware key, or copy protection.

Vendors may also distribute versions that remove particular features, or versions which allow only certain fields of endeavor, such as non-commercial, educational, or non-profit use.

Use restrictions vary by license:

- Windows Vista Starter is restricted to running a maximum of three concurrent applications.

- The retail edition of Microsoft Office Home and Student 2007 is limited to non-commercial use on up to three devices in one household.

- Windows XP can be installed on one computer, and limits the number of network file sharing connections to 10.[42] The Home Edition disables features present in Windows XP Professional.

- Traditionally, Adobe licenses are limited to one user, but allow the user to install a second copy on a home computer or laptop.[43] This is no longer true with the switching to Creative Cloud.

- iWork '09, Apple's productivity suite, is available in a five-user family pack, for use on up to five computers in a household.[44]

Inspection and modification of source code

[edit]Vendors typically distribute proprietary software in compiled form, usually the machine language understood by the computer's central processing unit. They typically retain the source code, or human-readable version of the software, often written in a higher level programming language.[45] This scheme is often referred to as closed source.[46]

While most proprietary software is distributed without the source code, some vendors distribute the source code or otherwise make it available to customers. For example, users who have purchased a license for the Internet forum software vBulletin can modify the source for their own site but cannot redistribute it. This is true for many web applications, which must be in source code form when being run by a web server. The source code is covered by a non-disclosure agreement or a license that allows, for example, study and modification, but not redistribution.[47] The text-based email client Pine and certain implementations of Secure Shell are distributed with proprietary licenses that make the source code available.[citation needed]Some licenses for proprietary software allow distributing changes to the source code, but only to others licensed for the product, and some[48] of those modifications are eventually picked up by the vendor.

Some governments fear that proprietary software may include defects or malicious features which would compromise sensitive information. In 2003 Microsoft established a Government Security Program (GSP) to allow governments to view source code and Microsoft security documentation, of which the Chinese government was an early participant.[49][50] The program is part of Microsoft's broader Shared Source Initiative which provides source code access for some products. The Reference Source License (Ms-RSL) and Limited Public License (Ms-LPL) are proprietary software licenses where the source code is made available.

Governments have also been accused of adding such malware to software themselves. According to documents released by Edward Snowden, the NSA has used covert partnerships with software companies to make commercial encryption software exploitable to eavesdropping, or to insert backdoors.[51][52]

Software vendors sometimes use obfuscated code to impede users who would reverse engineer the software.[53] This is particularly common with certain programming languages.[citation needed] For example, the bytecode for programs written in Java can be easily decompiled to somewhat usable code,[citation needed] and the source code for programs written in scripting languages such as PHP or JavaScript is available at run time.[54]

Redistribution

[edit]Proprietary software vendors can prohibit the users from sharing the software with others. Another unique license is required for another party to use the software.

In the case of proprietary software with source code available, the vendor may also prohibit customers from distributing their modifications to the source code.

Shareware is closed-source software whose owner encourages redistribution at no cost, but which the user sometimes must pay to use after a trial period. The fee usually allows use by a single user or computer. In some cases, software features are restricted during or after the trial period, a practice sometimes called crippleware.

Interoperability with software and hardware

[edit]Proprietary file formats and protocols

[edit]Proprietary software often[citation needed] stores some of its data in file formats that are incompatible with other software, and may also communicate using protocols which are incompatible. Such formats and protocols may be restricted as trade secrets or subject to patents.[citation needed]

Proprietary APIs

[edit]A proprietary application programming interface (API) is a software library interface "specific to one device or, more likely to a number of devices within a particular manufacturer's product range."[55] The motivation for using a proprietary API can be vendor lock-in or because standard APIs do not support the device's functionality.[55]

The European Commission, in its March 24, 2004, decision on Microsoft's business practices,[56] quotes, in paragraph 463, Microsoft general manager for C++ development Aaron Contorer as stating in a February 21, 1997, internal Microsoft memo drafted for Bill Gates:

- The Windows API is so broad, so deep, and so functional that most ISVs would be crazy not to use it. And it is so deeply embedded in the source code of many Windows apps that there is a huge switching cost to using a different operating system instead.

Early versions of the iPhone SDK were covered by a non-disclosure agreement. The agreement forbade independent developers from discussing the content of the interfaces. Apple discontinued the NDA in October 2008.[57]

Vendor lock-in

[edit]Any dependency on the future versions and upgrades for a proprietary software package can create vendor lock-in, entrenching a monopoly position.[58]

Software limited to certain hardware configurations

[edit]Proprietary software may also have licensing terms that limit the usage of that software to a specific set of hardware. Apple has such a licensing model for macOS, an operating system which is limited to Apple hardware, both by licensing and various design decisions. This licensing model has been affirmed by the United States Court of Appeals for the Ninth Circuit.[59]

Abandonment by proprietors

[edit]Proprietary software which is no longer marketed, supported or sold by its owner is called abandonware, the digital form of orphaned works. If the proprietor of a software package should cease to exist, or decide to cease or limit production or support for a proprietary software package, recipients and users of the package may have no recourse if problems are found with the software. Proprietors can fail to improve and support software because of business problems.[60] Support for older or existing versions of a software package may be ended to force users to upgrade and pay for newer versions[61](planned obsolescence). Sometimes another vendor or a software's community themselves can provide support for the software, or the users can migrate to either competing systems with longer support life cycles or to FOSS-based systems.[62]

Some proprietary software is released by their owner at end-of-life as open-source or source available software, often to prevent the software from becoming unsupported and unavailable abandonware.[63][64][65] 3D Realms and id Software are famous for the practice of releasing closed source software into the open source.[further explanation needed] Some of those kinds are free-of-charge downloads (freeware), some are still commercially sold (e.g. Arx Fatalis).[further explanation needed] More examples of formerly closed-source software in the List of commercial software with available source code and List of commercial video games with available source code.

Pricing and economics

[edit]Proprietary software is not synonymous with commercial software,[66][67] although the two terms are sometimes used synonymously in articles about free software.[68][69] Proprietary software can be distributed at no cost or for a fee, and free software can be distributed at no cost or for a fee.[70] The difference is that whether proprietary software can be distributed, and what the fee would be, is at the proprietor's discretion. With free software, anyone who has a copy can decide whether, and how much, to charge for a copy or related services.[71]

Proprietary software that comes for no cost is called freeware.

Proponents of commercial proprietary software argue that requiring users to pay for software as a product increases funding or time available for the research and development of software. For example, Microsoft says that per-copy fees maximize the profitability of software development.[72]

Proprietary software generally creates greater commercial activity over free software, especially in regard to market revenues.[73] Proprietary software is often sold with a license that gives the end user right to use the software.

Technical support for proprietary software can often be provided only by employees of the company that created the program and such service is included with the software. However, a dedicated technical support system increases the cost of software maintenance, which has an impact on its price.[74]

See also

[edit]References

[edit]- ^ a b Saraswati Experts. "2.5.3". COMPUTER SCIENCE WITH C++. Saraswati House Pvt Ltd. p. 1.27. ISBN 978-93-5199-877-8. Retrieved 29 June 2017.

- ^ Brendan Scott (March 2003). "Why Free Software's Long Run TCO must be lower". AUUGN. 24 (1). AUUG, Inc. 1. Definitions. Retrieved 29 June 2017.

- ^

Ceruzzi, Paul E. (2003). A History of Modern Computing. Cambridge, MA: MIT Press. p. 128. ISBN 0-262-53203-4.

Although IBM agreed to sell its machines as part of a Consent Decree effective January 1956, leasing continued to be its preferred way of doing business.

- ^ "The History of Equipment Leasing", Lease Genie, archived from the original on April 11, 2008, retrieved November 12, 2010,

In the 1960s, IBM and Xerox recognized that substantial sums could be made from the financing of their equipment. The leasing of computer and office equipment that occurred then was a significant contribution to leasings [sic] growth, since many companies were exposed to equipment leasing for the first time when they leased such equipment.

- ^ "Overview of the GNU System". GNU Operating System. Free Software Foundation. 2016-06-16. Retrieved 2017-05-01.

- ^ Pugh, Emerson W. (2002). "Origins of Software Bundling". IEEE Annals of the History of Computing. 24 (1): 57–58. Bibcode:2002IAHC...24a..57P. doi:10.1109/85.988580.

- ^ Hamilton, Thomas W. (1969). IBM's Unbundling Decision: Consequences for Users and the Industry. Programming Sciences Corporation.

- ^ "Chronological History of IBM: 1960s". IBM. n.d. Archived from the original on July 3, 2016. Retrieved May 28, 2016.

Rather than offer hardware, services and software exclusively in packages, marketers 'unbundled' the components and offered them for sale individually. Unbundling gave birth to the multibillion-dollar software and services industries, of which IBM is today a world leader.

- ^ Gates, Bill (February 3, 1976). "An Open Letter to Hobbyists". Retrieved May 28, 2016.

- ^ Swann, Matthew (18 November 2004). Executable Code is Not the Proper Subject of Copyright Law (Technical report). Cal Poly State University. CPSLO-CSC-04-02.

- ^ Pamela Samuelson (Sep 1984), "CONTU Revisited: The Case against Copyright Protection for Computer Programs in Machine-Readable Form", Duke Law Journal, 1984 (4): 663–769, doi:10.2307/1372418, JSTOR 1372418, archived from the original on Aug 4, 2017

- ^ Robert X. Cringely. Cringely's interview with Brewster Kahle. YouTube. 46 minutes in. Archived from the original on 2019-01-18.

- ^ Rep. Kastenmeier, Robert W. [D-WI-2 (1980-03-26). "H.R.6934 - 96th Congress (1979-1980): Computer Software Copyright Act of 1980". www.congress.gov. Retrieved 2025-09-16.

{{cite web}}: CS1 maint: numeric names: authors list (link) - ^ Cantrill, Bryan (2014-09-17). Corporate Open Source Anti-patterns. YouTube. Event occurs at 3:15. Archived from the original on 2021-10-27. Retrieved 2015-12-26.

- ^ Gallant, John (1985-03-18). "IBM policy draws fire - Users say source code rules hamper change". Computerworld. Retrieved 2015-12-27.

While IBM's policy of withholding source code for selected software products has already marked its second anniversary, users are only now beginning to cope with the impact of that decision. But whether or not the advent of object-code-only products has affected their day-to-day DP operations, some users remain angry about IBM's decision. Announced in February 1983, IBM's object-code-only policy has been applied to a growing list of Big Blue system software products

- ^ Hassett, Rob (Dec 18, 2012). "Impact of Apple vs. Franklin Decision". InternetLegal.com. Archived from the original on Sep 8, 2023.

- ^ a b Landley, Rob (2009-05-23). "May 23, 2009". landley.net. Retrieved 2024-06-22.

So if open source used to be the norm back in the 1960's and 70's, how did this _change_? Where did proprietary software come from, and when, and how? How did Richard Stallman's little utopia at the MIT AI lab crumble and force him out into the wilderness to try to rebuild it? Two things changed in the early 80's: the exponentially growing installed base of microcomputer hardware reached critical mass around 1980, and a legal decision altered copyright law to cover binaries in 1983. Increasing volume: The microprocessor creates millions of identical computers

- ^ https://www.geeksforgeeks.org/software-engineering/difference-between-open-source-software-and-proprietary-software/

- ^ Terasaki 2013, p. 469.

- ^ Terasaki 2013, pp. 469–470.

- ^ Boyle 2003, p. 45.

- ^ a b Clohessy et al. 2020, pp. 40–41.

- ^ Watt 2023, p. 4.

- ^ Dempsey & Kelliher 2018, p. 48.

- ^ Dempsey & Kelliher 2018, pp. 48, 57.

- ^ Dempsey & Kelliher 2018, pp. 61–63.

- ^ Dempsey & Kelliher 2018, p. 2.

- ^ Engelfriet, Arnoud (August–September 2006). "The best of both worlds". Intellectual Asset Management (19). Gavin Stewart. Archived from the original on 2013-09-14. Retrieved 2008-05-19.

- ^ Loftus, Jack (2007-02-19). "Managing mixed source software stacks". LinuxWorld. Archived from the original on 2010-06-03.

- ^ Tan, Aaron (2006-12-28). "Novell: We're a 'mixed-source' company". CNET Networks, Inc.

- ^ Rosenberg, Donald (2000). Open Source: The Unauthorized White Papers. Foster City: IDG. p. 109. ISBN 0-7645-4660-0.

- ^ "Categories of Free and Non-Free Software". GNU Project.

- ^ Free Software Foundation (2009-05-05). "Frequently Asked Questions about the GNU Licenses". Retrieved 2017-05-01.

- ^ Richard Stallman (2004-04-12). "Free But Shackled - The Java Trap". Retrieved 2017-05-01.

- ^ Liberman, Michael (1995). "Overreaching Provisions in Software License Agreements". Richmond Journal of Law and Technology. 1: 4. Retrieved November 29, 2011.

- ^ Limitations and Exceptions to Copyright and Neighbouring Rights in the Digital Environment: An International Library Perspective (2004). IFLA (2013-01-22). Retrieved on 2013-06-16.

- ^ Daniel A. Tysver (2008-11-23). "Why Protect Software Through Patents". Bitlaw. Retrieved 2009-06-03.

In connection with the software, an issued patent may prevent others from utilizing a certain algorithm (such as the GIF image compression algorithm) without permission, or may prevent others from creating software programs that perform a function in a certain way. In connection with computer software, copyright law can be used to prevent the total duplication of a software program, as well as the copying of a portion of software code.

- ^ Donovan, S. (1994). "Patent, copyright and trade secret protection for software". IEEE Potentials. 13 (3): 20. doi:10.1109/45.310923. S2CID 19873766.

Essentially there are only three ways to protect computer software under the law: patent it, register a copyright for it, or keep it as a trade secret.

- ^ Eben Moglen (2005-02-12). "Why the FSF gets copyright assignments from contributors". Retrieved 2017-05-01.

Under US copyright law, which is the law under which most free software programs have historically been first published, [...] only the copyright holder or someone having assignment of the copyright can enforce the license.

- ^ White, Aoife (2012-07-03). "Oracle Can't Stop Software License Resales, EU Court Says". Bloomberg.

- ^ Microsoft Corporation (2005-04-01). "End-User License Agreement for Microsoft Software: Microsoft Windows XP Professional Edition Service Pack 2" (PDF). Microsoft. p. Page 3. Retrieved 2009-04-29.

- ^ Microsoft Corporation (2005-04-01). "End-User License Agreement for Microsoft Software: Microsoft Windows XP Professional Edition Service Pack 2" (PDF). Microsoft. p. Page 1. Retrieved 2009-04-29.

You may install, use, access, display and run one copy of the Software on a single computer, such as a workstation, terminal or another device ("Workstation Computer"). The Software may not be used by more than two (2) processors at any one time on any single Workstation Computer. ... You may permit a maximum of ten (10) computers or other electronic devices (each a 'Device') to connect to the Workstation Computer to utilize one or more of the following services of the Software: File Services, Print Services, Internet Information Services, Internet Connection Sharing and telephony services.

- ^ Adobe Systems, Adobe Software License Agreement (PDF), retrieved 2010-06-09

- ^ Parker, Jason (January 27, 2009). "Apple iWork '09 review: Apple iWork '09". CNET. Retrieved May 2, 2022.

- ^ Heffan, Ira V. (1997). "Copyleft: Licensing Collaborative Works in the Digital Age" (PDF). Stanford Law Review. 49 (6): 1490. doi:10.2307/1229351. JSTOR 1229351. Archived from the original (PDF) on 2013-05-14. Retrieved 2009-07-27.

Under the proprietary software model, most software developers withhold their source code from users.

- ^ David A. Wheeler (2009-02-03). "Free-Libre / Open Source Software (FLOSS) is Commercial Software". Retrieved 2009-06-03.

- ^ "Distribution of IBM Licensed Programs and Licensed Program Materials and Modified Agreement for IBM Licensed Programs". Announcement Letters. IBM. February 8, 1983. 283-016.

- ^ Greg Mushial (July 20, 1983), "Module 24: SLAC Enhancements to and Beautifications of the IBM H-Level Assembler for Version 2.8", SLAC VM NOTEBOOK, Stanford Linear Accelerator Center

- ^ Shankland, Stephen (January 30, 2003). "Governments to see Windows code". CNET. Retrieved May 2, 2022.

- ^ Gao, Ken (February 28, 2003). "China to view Windows code". CNET. Retrieved May 2, 2022.

- ^ James Ball, Julian Borger and Glenn Greenwald (2013-09-06). "US and UK spy agencies defeat privacy and security on the internet". The Guardian.

- ^ Bruce Schneier (2013-09-06). "How to remain secure against NSA surveillance". The Guardian.

- ^ Jacob, Matthias; Boneh, Dan; Felten, Edward (30 October 2003). "Attacking an Obfuscated Cipher by Injecting Faults". In Feigenbaum, Joan (ed.). Digital Rights Management: ACM CCS-9 Workshop, DRM 2002, Washington, DC, USA, November 18, 2002, Revised Papers. Second International Workshop on Digital Rights Management. Lecture Notes in Computer Science. Vol. 2696. Springer Berlin Heidelberg. p. 17. ISBN 978-3-540-44993-5. Retrieved 12 January 2024 – via Internet Archive.

- ^ Tony Patton (2008-11-21). "Protect your JavaScript with obfuscation". TechRepublic. Archived from the original on March 15, 2014. Retrieved May 2, 2022.

While the Web promotes the sharing of such code, there are times when you or a client may not want to share their JavaScript code. This may be due to the sensitive nature of data within the code, proprietary calculations, or any other scenario.

- ^ a b Orenstein, David (January 10, 2000). "Application Programming Interface". Computerworld. Retrieved May 2, 2022.

- ^ "Commission Decision of 24.03.2004 relating to a proceeding under Article 82 of the EC Treaty (Case COMP/C-3/37.792 Microsoft)" (PDF). European Commission. March 24, 2004. Archived from the original (PDF) on October 28, 2008. Retrieved June 17, 2009.

- ^ Wilson, Ben (2008-10-01). "Apple Drops NDA for Released iPhone Software". CNET. Archived from the original on 2013-03-08. Retrieved 2022-05-02.

- ^ The Linux Information Project (2006-04-29). "Vendor Lock-in Definition". Retrieved 2009-06-11.

Vendor lock-in, or just lock-in, is the situation in which customers are dependent on a single manufacturer or supplier for some product [...] This dependency is typically a result of standards that are controlled by the vendor [...] It can grant the vendor some extent of monopoly power [...] The best way for an organization to avoid becoming a victim of vendor lock-in is to use products that conform to free, industry-wide standards. Free standards are those that can be used by anyone and are not controlled by a single company. In the case of computers, this can usually be accomplished by using free software rather than proprietary software (i.e., commercial software).

- ^ Don Reisinger (2011-09-29). "Apple wins key battle against Psystar over Mac clones". Retrieved 2022-05-02.

- ^ "What happens when a proprietary software company dies?". Linux. October 24, 2003. Retrieved May 2, 2022.

- ^ Livingston, Brian (December 15, 2006). "Microsoft Turns Up The Heat On Windows 2000 Users". CRN. Archived from the original on May 3, 2022. Retrieved May 2, 2022.

- ^ Cassia, Fernando (March 28, 2007). "Open Source, the only weapon against 'planned obsolescence'". The Inquirer. Archived from the original on November 22, 2012. Retrieved August 2, 2012.

- ^ Bell, John (October 1, 2009). "Opening the Source of Art". Technology Innovation Management Review. Archived from the original on March 30, 2014. Retrieved May 2, 2022.

that no further patches to the title would be forthcoming. The community was predictably upset. Instead of giving up on the game, users decided that if Activision wasn't going to fix the bugs, they would. They wanted to save the game by getting Activision to open the source so it could be kept alive beyond the point where Activision lost interest. With some help from members of the development team that were active on fan forums, they were eventually able to convince Activision to release Call to Power II's source code in October of 2003.

- ^ Wen, Howard (June 10, 2004). "Keeping the Myths Alive". Linux Dev Center. Archived from the original on April 6, 2013. Retrieved December 22, 2012.

fans of the Myth trilogy have taken this idea a step further: they have official access to the source code for the Myth games. Organized under the name MythDevelopers, this all-volunteer group of programmers, artists, and other talented people devote their time to improving and supporting further development of the Myth game series.

- ^ Largent, Andy (October 8, 2003). "Homeworld Source Code Released". Inside Mac Games. Archived from the original on October 12, 2013. Retrieved November 24, 2012.

With the release of Homeworld 2 for the PC, Relic Entertainment has decided to give back to their impressive fan community by releasing the source code to the original Homeworld.

- ^ Rosen, Lawrence (2004). Open Source Licensing. Upper Saddle River: Prentice Hall. pp. 52, 255, 259. ISBN 978-0-13-148787-1.

- ^ Havoc Pennington (2008-03-02). "Debian Tutorial". Archived from the original on 2018-01-29. Retrieved 2009-06-04.

It is important to distinguish commercial software from proprietary software. Proprietary software is non-free software, while commercial software is software sold for money.

- ^ Russell McOrmond (2000-01-04). "What is "Commercial Software"?". Archived from the original on 2012-10-04. Retrieved 2009-05-02.

- ^ Michael K. Johnson (1996-09-01). "Licenses and Copyright". Retrieved 2009-06-16.

If you program for Linux, you do need to understand licensing, no matter if you are writing free software or commercial software.

- ^ Eric S. Raymond (2003-12-29). "Proprietary, Jargon File". Retrieved 2009-06-12.

Proprietary software should be distinguished from commercial software. It is possible for the software to be commercial [...] without being proprietary. The reverse is also possible, for example in binary-only freeware.

- ^ "Selling Free Software". GNU Project.

- ^ "The Commercial Software Model". Microsoft. May 2001. Archived from the original on 2007-03-05.

- ^ Open Source Versus Commercial Software: Why Proprietary Software is Here to Stay. Sams Publishing. October 2005. Retrieved 2022-05-02.

- ^ "Proprietary software | Definition, History, & Facts | Britannica". www.britannica.com. Retrieved 2025-04-24.

{kind=link}

External links

[edit] Media related to Proprietary software at Wikimedia Commons

Media related to Proprietary software at Wikimedia Commons

| General | |||

|---|---|---|---|

| Software packages | |||

| Community | |||

| Organisations | |||

| Licenses |

| ||

| Challenges | |||

| Related topics | |||

Proprietary software

View on GrokipediaProprietary software, also known as closed-source software, consists of programs whose source code is kept private by the copyright holder, who imposes restrictions on users' rights to inspect, modify, or redistribute it through end-user license agreements.[1][2] This model has dominated software development since the commercialization of computing in the mid-20th century, enabling creators to protect investments in research and development while monetizing via direct sales, subscriptions, or usage fees.[3] Prominent examples include Microsoft Windows, which holds a significant share of desktop operating systems, and Adobe's suite of creative tools, illustrating how proprietary licensing sustains large-scale innovation and market leadership in enterprise and consumer sectors.[2][1] Debates persist with advocates of open-source alternatives, who contend that proprietary restrictions foster dependency and stifle collaborative progress, whereas defenders highlight empirical advantages in quality control and financial incentives for proprietary maintainers, as evidenced by sustained corporate outputs absent in purely communal efforts.[4][5] Despite criticisms of potential vendor lock-in, proprietary software underpins the majority of commercial deployments, driving economic value through proprietary ecosystems that integrate hardware, services, and updates tailored to specific revenue models.[3]

Definition and Fundamentals

Core Characteristics

Proprietary software refers to computer programs owned and controlled by an individual, company, or organization that retains exclusive legal rights over its use, modification, and distribution. The defining feature is the non-disclosure of the source code, which remains confidential to protect intellectual property and competitive advantages, distinguishing it from open-source alternatives where code is publicly accessible. [2] [3] Distribution occurs primarily in compiled binary form, limiting users to executing the software as provided without insight into its underlying logic or algorithms. Licensing agreements, often termed end-user license agreements (EULAs), enforce restrictions such as bans on copying beyond authorized instances, reverse engineering, or creating derivative works, with violations potentially leading to legal action under copyright law. [3] [6] [7] Proprietary models typically involve commercial transactions, where users pay fees for access via one-time purchases, subscriptions, or per-use models, funding ongoing development and support controlled by the proprietor. This structure relies on intellectual property protections like copyrights and trade secrets to maintain monopoly-like control, though enforcement varies by jurisdiction and can face challenges from interoperability requirements or fair use doctrines. [2] [8]Distinction from Open Source and Free Software

Proprietary software restricts access to its source code, distributing only compiled binaries under end-user license agreements (EULAs) that prohibit reverse engineering, modification, or redistribution without permission, thereby maintaining the developer's exclusive control and enabling monetization through sales or subscriptions.[2] In contrast, open source software provides public access to source code under licenses approved by the Open Source Initiative (OSI), which was established in 1998 to promote collaborative development; these licenses require free redistribution, inclusion of source code, allowance for derived works, and non-discrimination against fields of endeavor, fostering community contributions and innovation without the secrecy inherent in proprietary models.[9][10] Free software, as defined by the Free Software Foundation (FSF) founded by Richard Stallman in 1985, emphasizes ethical user autonomy through four essential freedoms: the freedom to run the program for any purpose (freedom 0), to study and modify it (freedom 1), to redistribute copies (freedom 2), and to distribute modified versions (freedom 3), often enforced via copyleft licenses like the GNU General Public License (GPL) introduced in 1989.[11] While most free software qualifies as open source under OSI criteria, the reverse is not always true, as open source permits permissive licenses (e.g., MIT License) that allow incorporation into proprietary software without requiring source disclosure of derivatives, a practice the FSF critiques for potentially undermining user freedoms by enabling "semi-free" or non-free extensions.[12] Proprietary software, by withholding source code and freedoms, precludes such community-driven evolution, prioritizing developer revenue protection—evident in market dominance of products like Microsoft Windows, which held approximately 72% global desktop OS share as of 2023—over user control or collective improvement.[13] This tripartite distinction underscores causal trade-offs: proprietary models incentivize private investment in features like integrated security updates (e.g., Adobe's proprietary Flash before its 2020 end-of-life), but limit interoperability and auditing, whereas open source and free software enable transparency and adaptation at the cost of coordinated maintenance challenges, as seen in the fragmentation of Linux distributions since the kernel's 1991 release.[14] Empirical data from the OSI indicates over 1,000 approved open source licenses by 2024, reflecting broader adoption in enterprise settings for cost efficiency, yet proprietary software persists in sectors requiring vendor accountability, such as enterprise resource planning systems where support contracts exceed open alternatives in reliability guarantees.[10]Historical Evolution

Early Commercial Origins (Pre-1970s)

The development of proprietary software in its early commercial form coincided with the rise of electronic digital computers in the mid-20th century, where programs were created as confidential tools tailored to specific hardware and business needs, without public distribution of source code. Hardware manufacturers such as IBM dominated this period, providing custom or bundled programming for mainframes like the IBM 701 scientific computer released in 1953, which included proprietary utilities and assembly language tools designed exclusively for their systems to maintain competitive advantages in enterprise data processing.[15] These early efforts focused on applications for scientific calculations, inventory management, and payroll, reflecting a model where software served as an integral, non-separable component of leased hardware rather than a standalone commodity.[16] The emergence of independent software vendors in the late 1950s marked the initial shift toward commercialized proprietary packages. Applied Data Research (ADR), established in 1959, pioneered this by developing and marketing off-the-shelf utilities such as sorting and flowcharting programs for IBM mainframes, including the SORT/MERGE routine for the IBM 7090 and AUTOFLOW released in 1965, which automated program documentation.[17] ADR's approach treated software as a licensable product protected by patents—Martin Goetz of ADR secured the first U.S. software patent in 1968 for a data-sorting method—emphasizing intellectual property control to prevent reverse-engineering and ensure revenue from reusable code.[18] This contrasted with collaborative user groups like SHARE, formed by IBM customers in 1955, which exchanged limited code snippets but did not commercialize them broadly.[19] The IBM System/360 family, introduced in 1964, accelerated proprietary software complexity due to its compatibility across models, necessitating advanced operating systems like OS/360, which IBM developed internally without source disclosure to safeguard market dominance.[16] By the late 1960s, rising antitrust scrutiny from the U.S. Department of Justice prompted IBM to announce on June 23, 1969, the unbundling of software and services from hardware pricing, effective January 1, 1970, thereby formalizing software as a distinct proprietary asset that could be licensed separately and spurring third-party development.[19] This decision, influenced by legal pressures over bundling practices, underscored the proprietary nature of pre-existing software ecosystems while laying groundwork for an expanded commercial market.[20]Expansion in Personal Computing Era (1970s-1990s)

The personal computing era began with the introduction of microcomputers like the MITS Altair 8800 in 1975, initially featuring software shared freely among hobbyists via user groups and bulletin boards. Microsoft, co-founded by Bill Gates and Paul Allen in 1975, disrupted this culture by developing a proprietary BASIC interpreter for the Altair, licensed from a Dartmouth College version and adapted for commercial sale. Priced at $150 for cassette tape or $400 for paper tape versions, Altair BASIC required payment for full functionality, with limited demos freely distributed to encourage purchases. In a February 3, 1976, open letter published in computer magazines, Gates condemned unauthorized copying as theft, arguing that without revenue from sales, quality software development would stagnate, as hobbyist sharing undermined incentives for professional programming efforts.[21] The Apple II, launched by Apple Computer in June 1977, accelerated proprietary software's expansion through its expandable architecture and color graphics, attracting third-party developers. Apple's Integer BASIC, bundled in ROM, and subsequent Apple DOS (introduced in 1978) were copyrighted and distributed as proprietary systems, with Apple enforcing licensing for clones and peripherals. Applications like VisiCalc, the first electronic spreadsheet released in 1979 by Software Arts, epitomized commercial viability; priced at $100–$400 depending on hardware, it was protected by copyright and sold through authorized dealers, boosting Apple II sales to over 600,000 units by 1983 as users purchased machines specifically for such "killer apps." Other proprietary titles, including word processors like AppleWriter and games with copy protection schemes, dominated the ecosystem, though piracy via floppy disk duplication remained rampant, prompting early anti-copying measures like serialized disks. The IBM Personal Computer's release in August 1981 marked proprietary software's institutionalization, powered by Microsoft's MS-DOS (version 1.0 shipped in 1981), adapted from 86-DOS acquired by Microsoft in July 1981 for $75,000. IBM licensed a customized variant as PC-DOS, but Microsoft's non-exclusive deal allowed sublicensing to competitors, fostering IBM PC clones and standardizing MS-DOS across hardware by the mid-1980s, with over 10 million copies sold by 1987. This openness in hardware contrasted with closed software models, enabling proprietary applications like Lotus 1-2-3 (1983), a spreadsheet that captured 70% market share, and dBase II for databases, both reliant on DOS licensing fees and end-user agreements restricting reverse engineering. By the 1990s, Windows 3.0 (1990) built on this foundation, achieving 90% PC market penetration by 1993 through proprietary graphical interfaces layered atop MS-DOS, as revenues from software licensing—totaling billions for Microsoft—dwarfed hardware margins and entrenched intellectual property controls.[22][23]Dominance in Digital Ecosystems (2000s-Present)

In the 2000s, Microsoft Windows solidified its dominance in desktop operating systems, holding over 90% global market share by 2003, driven by the widespread adoption of Windows XP released in 2001, which powered the majority of personal computers for enterprise and consumer use.[24][25] By 2010, Windows maintained approximately 92% share amid the shift to Windows 7, reflecting proprietary software's entrenched position through compatibility with legacy applications, hardware integration, and enterprise licensing agreements that discouraged alternatives.[24] Despite antitrust scrutiny in the U.S. and Europe during the early 2000s, Microsoft's control persisted, with Windows versions like 10 (2015) and 11 (2021) sustaining around 72% share as of 2024, as open-source options like Linux captured only 4% due to limited ecosystem support.[24] The rise of mobile ecosystems further exemplified proprietary dominance, particularly Apple's iOS following the iPhone launch in 2007, which introduced a closed, proprietary platform integrating hardware, software, and the App Store in 2008, enabling strict control over app distribution and monetization.[26] iOS achieved 28% global smartphone market share by 2024, with higher penetration in premium segments, supported by proprietary features like Face ID (2017) and seamless device integration that fostered user lock-in.[27] Google's Android, open-source at its core since 2008, relied on proprietary Google Mobile Services—including the Play Store and core apps—for 72% share, where Google enforced ecosystem control via licensing, generating billions in revenue from app commissions and services.[27][28] This hybrid model underscored proprietary elements' role in scalability, as Android's fragmentation contrasted with iOS's cohesive, revenue-optimized architecture, contributing to Apple's services revenue exceeding $85 billion annually by 2023.[29] Cloud computing emerged as another proprietary stronghold, with Amazon Web Services (AWS) launching in 2006 and capturing 31-33% of the infrastructure-as-a-service market by 2024 through proprietary tools like EC2 and S3, enabling scalable, vendor-locked deployments for enterprises.[30] Microsoft Azure, building on Windows Server proprietary foundations since 2010, secured 20% share, leveraging hybrid cloud integrations with on-premises proprietary software.[30] Google Cloud Platform, at 12%, complemented Android's ecosystem with proprietary AI services like TensorFlow, collectively positioning the "Big Three" at over 60% market control and driving global cloud spending to surpass $500 billion in 2023.[31] These platforms' dominance stemmed from proprietary APIs and data analytics, which incentivized developer lock-in and R&D investment—Microsoft's cloud revenue alone reached $110 billion in fiscal 2023—outpacing open alternatives fragmented by compatibility issues.[32] Proprietary ecosystems' economic scale amplified this era's trends, with Microsoft reporting $23 billion in revenue for fiscal 2000, escalating to $211 billion by 2023, largely from Windows, Office, and Azure licensing.[33] Apple's post-iPhone pivot yielded $394 billion in 2023 revenue, 52% from hardware tied to iOS services, exemplifying how proprietary integration captured network effects in app economies.[34] Alphabet (Google) generated $283 billion in 2023, with proprietary search, ads, and cloud services reinforcing mobile dominance despite open Android licensing.[34] Regulatory challenges, including EU fines against Google for Android bundling (2018, €4.3 billion) and ongoing U.S. scrutiny of app store practices, highlighted tensions but did not erode core market positions, as proprietary models sustained innovation through recoupable investments exceeding $20 billion annually per firm.Legal and Intellectual Property Framework

Copyright Protections and Licensing Models

Copyright protection for computer programs in the United States originated with the first registration deposit on November 30, 1961, by North American Aviation, and the Copyright Office formally began accepting software registrations on May 19, 1964.[35][36] Under the 1976 Copyright Act, effective January 1, 1978, software qualifies as a "literary work" eligible for protection, covering the specific sequence of instructions and expressions in source or object code but excluding underlying ideas, algorithms, or functional aspects.[37] This protection arises automatically upon fixation in a tangible medium, granting owners exclusive rights to reproduction, distribution, public performance, and preparation of derivative works for the author's life plus 70 years or 95–120 years for works made for hire.[38] Proprietary software developers register copyrights with the U.S. Copyright Office to enable statutory damages and attorney fees in infringement suits, deterring unauthorized copying that could undermine commercial value.[37] In proprietary contexts, copyright serves as the foundational mechanism to restrict access to source code, typically distributing only compiled binaries to prevent modification or reverse engineering.[39] This contrasts with open-source models by enforcing exclusivity, where violations trigger infringement claims under laws like the Digital Millennium Copyright Act (DMCA) of 1998, which prohibits circumvention of technological protection measures such as encryption or license keys.[37] Courts have upheld these protections, as in Apple Inc. v. Psystar Corp. (2009), where unauthorized replication of macOS on non-Apple hardware was deemed infringement, affirming that licenses can impose hardware-specific restrictions enforceable via copyright.[39] However, copyright does not safeguard against independent recreation of similar functionality, relying instead on complementary mechanisms like trade secrets for undisclosed algorithms.[40] Licensing models operationalize these protections through end-user license agreements (EULAs), contractual terms presented during installation or access that grant limited, revocable permissions for use while retaining ownership with the licensor.[41] Common provisions prohibit redistribution, decompilation, and commercial exploitation, often tying usage to specific devices or users to maximize control and revenue.[42] Perpetual licenses, prevalent in the 1990s–2000s for desktop software like Microsoft Office, allow indefinite use post one-time payment but may require separate maintenance fees for updates.[6] Subscription models, dominant since the 2010s (e.g., Adobe Creative Cloud launched in 2013), provide ongoing access via recurring fees, enabling remote enforcement and feature gating.[43] Other variants include per-user or per-device limits, as in enterprise volume licensing, and consumption-based metering for cloud services, where overages incur additional charges to align costs with actual utilization.[44] These models sustain proprietary ecosystems by coupling software with services, though enforceability varies by jurisdiction, with some courts scrutinizing "shrink-wrap" EULAs for adequate notice and assent.[41]Patents, Trade Secrets, and Enforcement

Patents grant proprietary software developers exclusive rights to inventions such as algorithms, user interfaces, and data processing methods that meet criteria of novelty, non-obviousness, and utility under laws like 35 U.S.C. § 101.[45] The first U.S. software patent was issued on April 23, 1968, covering a method for converting binary-coded decimal numerals into binary numerals.[46] Landmark Supreme Court decisions have shaped eligibility; for instance, Diamond v. Diehr (1981) upheld a patent on a rubber-curing process using a computer algorithm, affirming that software tied to a specific practical application is patentable.[47] However, Alice Corp. v. CLS Bank International (2014) invalidated patents on abstract ideas implemented via generic computers, raising the threshold for software inventions and leading to increased invalidation rates in litigation.[48] Trade secrets protect proprietary software elements like source code, internal algorithms, and development processes that derive economic value from secrecy and are subject to reasonable efforts to maintain confidentiality, as defined under the Uniform Trade Secrets Act (UTSA) adopted in 48 U.S. states.[49] Unlike patents, trade secrets require no public disclosure or registration, offering perpetual protection against misappropriation but vulnerability to independent invention or reverse engineering.[50] High-profile cases illustrate their enforcement; in Waymo LLC v. Uber Technologies, Inc. (2017), Waymo alleged Uber stole self-driving car software trade secrets from a former Google engineer, resulting in a $245 million settlement and a permanent injunction on certain technologies.[51] Enforcement of patents and trade secrets in proprietary software often involves litigation to secure injunctions, damages, or royalties, with software-related patents comprising about 30% of U.S. patent infringement cases in 2023.[52] Direct infringement occurs when a competitor copies patented code or methods, while induced infringement applies to facilitating others' use, as seen in ongoing disputes over API implementations.[53] Trade secret enforcement has surged, with a 12.4% year-over-year increase in U.S. cases reported in 2023, frequently involving departing employees or data scraping.[54] Recent verdicts, such as the $222 million award against Walmart in 2025 for misappropriating produce monitoring technology trade secrets, underscore aggressive judicial remedies including treble damages for willful violations.[55] Companies bolster enforcement through non-disclosure agreements (NDAs), employee training, and digital rights management tools to prevent unauthorized access.[56]Key Legal Precedents and Limitations

In the United States, the case of Sega Enterprises Ltd. v. Accolade, Inc. (977 F.2d 1510, 9th Cir. 1992) established that intermediate copying of proprietary software code through disassembly for the purpose of achieving interoperability constitutes fair use under copyright law, provided the final product does not substantially incorporate the original code.[57][58] The Ninth Circuit reasoned that Accolade's reverse engineering of Sega's Genesis console software was necessary to develop compatible games, outweighing potential market harm to Sega, as no direct competition in console sales occurred.[58] Conversely, MAI Systems Corp. v. Peak Computer, Inc. (991 F.2d 511, 9th Cir. 1993) ruled that loading proprietary operating system software into a computer's random access memory (RAM) during maintenance activities creates a temporary copy that infringes the copyright owner's exclusive reproduction right, even without permanent storage.[59] The court held that Peak's unauthorized booting of MAI's software on serviced computers violated the Copyright Act, as RAM loading qualifies as fixation, limiting third-party servicing unless explicitly licensed.[59] The enforceability of end-user license agreements (EULAs) restricting resale was clarified in Vernor v. Autodesk, Inc. (621 F.3d 1102, 9th Cir. 2010), where the Ninth Circuit adopted a three-factor test to distinguish licenses from sales: whether the copyright owner (1) specifies that the user is granted a license, (2) significantly restricts the user's ability to transfer the software, and (3) imposes notable use restrictions.[60] Applying this to Autodesk's AutoCAD software, the court determined transfers were licenses, not sales, thus excluding first sale doctrine protections under 17 U.S.C. § 109 and allowing Autodesk to prohibit Vernor's secondary sales.[60] Regarding application programming interfaces (APIs), Google LLC v. Oracle America, Inc. (141 S. Ct. 1183, 2021) held by the Supreme Court that Google's reimplementation of 37 Java API packages in Android constituted fair use, considering the transformative nature of the use, limited copying (11,500 lines out of 2.86 million), and negligible market harm to Oracle's licensing.[61] The 6-2 decision emphasized that declaring code serves a functional, system-organizing role, tilting fair use factors toward Google despite Oracle's proprietary claims.[61][62] The Digital Millennium Copyright Act (DMCA) of 1998 imposes significant limitations via its anti-circumvention provisions in 17 U.S.C. § 1201, prohibiting the bypassing of technological measures that control access to copyrighted works, including proprietary software protections like encryption or password systems.[63] This extends beyond traditional infringement by criminalizing tools and acts enabling circumvention, even for noninfringing purposes, though triennial exemptions by the Librarian of Congress allow limited reverse engineering for interoperability, security research, or repair in specified cases.[64][65] Critics argue these rules hinder innovation by overriding fair use doctrines, as seen in restricted device diagnostics or software modifications.[64] Internationally, the European Union's Directive 2009/24/EC on the legal protection of computer programs permits reverse engineering of proprietary software interfaces for interoperability purposes without the right holder's consent, provided it is indispensable for independent creation and does not impair error correction rights.[66] This contrasts with stricter U.S. approaches under DMCA, allowing EU users to decompile code solely to achieve compatibility, as affirmed in cases like the Court of Justice's interpretation emphasizing lawful user rights.[67] However, such exceptions exclude commercial exploitation beyond interoperability and are void if contractually prohibited, balancing proprietary control with market competition.[68]Technical Classifications and Features

Categories of Proprietary Software

Proprietary software is categorized chiefly by its licensing and distribution models, which enforce the owner's control over usage while accommodating diverse monetization strategies. These categories determine whether access is granted through upfront payments, recurring fees, or limited trials, all while withholding source code and modification rights. Unlike open-source alternatives, proprietary categories prioritize revenue protection and vendor dependency, often leading to higher development investments but restricted user freedoms.[2][3] Perpetual licenses form a core category, providing indefinite use rights after a one-time purchase, though warranties and updates typically expire without further payment. This model prevailed in the personal computing boom of the 1980s and 1990s for standalone applications, such as early Microsoft Office suites released starting in 1989.[3][69][44] Subscription-based licenses, a more recent dominant category since the early 2010s, mandate periodic payments—often monthly or annually—for ongoing access, maintenance, and feature enhancements. Adobe's transition to the Creative Cloud subscription model in 2013 illustrates this shift, bundling tools like Photoshop into a service-oriented framework that ensures continuous vendor revenue and control.[2][70][69] Volume and site licenses cater to organizational use, permitting multiple deployments across users or locations under bulk agreements that customize terms like installation limits or support levels. These are common in enterprise settings, as with Microsoft Volume Licensing programs established in the 1990s for scalable deployment in businesses.[3][44] Additional categories include shareware, where limited versions are freely distributed for trial, prompting payment for full functionality—a model popularized in the 1980s for independent developers—and freemium, offering basic free access with paid upgrades for advanced capabilities, as in many SaaS products since the 2000s. These variants expand reach while upholding proprietary restrictions on reverse engineering and redistribution.[44][70]Architectural and Distribution Models

Proprietary software is architecturally distinguished by its reliance on compiled binary executables or object code, which conceals the underlying source code from end users to safeguard intellectual property and prevent unauthorized modifications.[71] This closed-source approach typically incorporates built-in mechanisms such as code obfuscation, encryption of key components, and runtime licensing verification to deter reverse engineering and enforce usage restrictions.[72] For instance, architectures often include proprietary security models with centralized vendor-controlled updates, ensuring that patches and features are deployed only through official channels rather than community-driven contributions.[73] In terms of distribution models, proprietary software is commonly delivered as pre-compiled binaries via digital downloads, physical media like CDs or USB drives, or app store installations, accompanied by end-user license agreements (EULAs) that prohibit redistribution or decompilation.[74] Subscription-based models, such as those used by Microsoft 365 or Adobe Creative Cloud, provide ongoing access to updated binaries over the internet, tying distribution to recurring payments and remote deactivation capabilities for non-compliance.[75] [2] Software-as-a-Service (SaaS) variants shift architecture toward server-side execution, where users interact via web interfaces without receiving local binaries, as seen in platforms like Salesforce, thereby centralizing control and enabling usage metering.[76] Enterprise deployments may involve on-premise installations of binaries customized under non-disclosure agreements, while embedded proprietary firmware in hardware devices, such as routers or printers, is distributed as integrated binary images flashed during manufacturing.[1] These models facilitate revenue through per-user licensing or perpetual fees but impose architectural trade-offs, including reduced interoperability due to proprietary protocols embedded in the binaries, which can lock users into vendor ecosystems.[6] Historical shifts, such as the move from boxed retail software in the 1990s to cloud distributions post-2010, reflect adaptations to digital delivery efficiencies, with over 80% of enterprise software revenue derived from subscription or SaaS models by 2023 according to industry analyses.[76]Business and Economic Incentives

Pricing Strategies and Revenue Models

Proprietary software vendors predominantly employ perpetual licensing and subscription-based models to monetize their products, with the choice driven by the need to recover substantial upfront development costs and sustain ongoing innovation. Perpetual licenses involve a one-time upfront payment granting indefinite use rights, often supplemented by optional annual maintenance fees covering updates and support, typically priced at 15-25% of the initial license cost. Early implementations by vendors like SAP and Microsoft emphasized revenue from these one-time large software license fees, plus annual maintenance fees (typically 15-20% of license value) and implementation consulting services; on-premise deployment with high implementation costs and long cycles; sales reliant on direct teams and large contracts; resulting in strong initial cash flow but fluctuating revenue dependent on maintenance renewals.[77][78][79] This model aligns with traditional on-premises deployments, allowing customers perceived ownership while enabling vendors to generate recurring revenue through support contracts, which can exceed 20% of license fees annually for enterprise software like Oracle Database.[80] In contrast, subscription models, increasingly dominant since the 2010s, charge recurring fees—monthly or annually—for access, updates, and cloud-hosted delivery, providing vendors with predictable cash flows and reducing piracy risks via account-based authentication.[81] The shift toward subscriptions has been pronounced among major vendors, as evidenced by Adobe's 2013 transition from perpetual licenses for Creative Suite to the Creative Cloud subscription service. Initially, this caused a revenue dip of 8% in 2013 due to customer resistance and deferred recognition of multi-year commitments, but it yielded sustained growth, with total revenue rising from $4.1 billion in 2013 to $19 billion by 2023, over 90% from recurring sources.[82][83] Similarly, Microsoft has expanded Microsoft 365 subscriptions for Office productivity tools, contributing to the Productivity and Business Processes segment's $59.7 billion in fiscal 2021 revenue, while maintaining perpetual options alongside volume licensing for enterprises.[84] Oracle offers both perpetual licenses—e.g., a $1 million upfront for database software plus hardware—and subscription tiers for cloud services, with support fees on perpetual deals ensuring long-term revenue even as subscriptions gain traction for scalability.[80] These strategies reflect economic incentives to maximize lifetime customer value amid high fixed costs of proprietary development, where marginal reproduction is near-zero but initial R&D investments demand amortization over time. Subscriptions facilitate upselling through tiered plans (e.g., basic vs. premium features) and usage-based add-ons, fostering vendor lock-in via continuous updates that obsolete standalone versions.[85] Perpetual models, however, appeal to cost-sensitive buyers seeking to cap expenses, though vendors often discount them less aggressively and pair with mandatory support to maintain revenue streams, as perpetual sales alone yield lumpy income vulnerable to market cycles.[86] Hybrid approaches, such as freemium trials leading to paid tiers, further enable market penetration while converting users to revenue-generating proprietary features.[87] Overall, the preference for subscriptions has boosted vendor valuations by emphasizing annual recurring revenue metrics attractive to investors, though it exposes customers to potential fee escalations without asset ownership.[88]Investment in Research and Development

Proprietary software developers allocate significant resources to research and development (R&D) to create novel features, enhance performance, and integrate emerging technologies such as artificial intelligence and cloud computing, with expenditures often comprising 10-20% of revenues for leading firms.[89] This investment is facilitated by intellectual property protections, which enable companies to monetize innovations through licensing and sales, thereby recouping costs and incentivizing further outlays.[90] In fiscal year 2023, Microsoft reported R&D expenses of $27.195 billion, representing approximately 13% of its revenue, a figure consistent with prior years and underscoring sustained commitment to proprietary advancements in operating systems and productivity tools.[91][92] Major proprietary software entities, including those in the "Big Tech" cohort, have escalated R&D outlays amid competitive pressures and technological shifts. From 2015 to 2023, collective R&D spending by Amazon, Alphabet, Microsoft, Apple, and Meta grew at a 22% annualized rate, reaching $213.7 billion for the trailing twelve months ending in 2023, driven by investments in proprietary AI models, custom silicon, and enterprise software ecosystems.[93] Projections for 2024 indicate Apple allocating around $33 billion and Microsoft approximately $31.9 billion, reflecting priorities in areas like augmented reality platforms and AI integration within closed-source architectures.[94] In the software and services sector, R&D budgets expanded notably between 2022 and 2023, with firms pivoting toward proprietary AI capabilities to sustain market differentiation.[95]| Company | R&D Expenditure (2023, USD Billion) | Approximate % of Revenue |

|---|---|---|

| Microsoft | 27.2 | 13% |

| Apple | 29.9 (FY2023) | ~17% of gross profit |

| Alphabet | 45.4 (estimated from trends) | Varies, ~14% |