Community hub

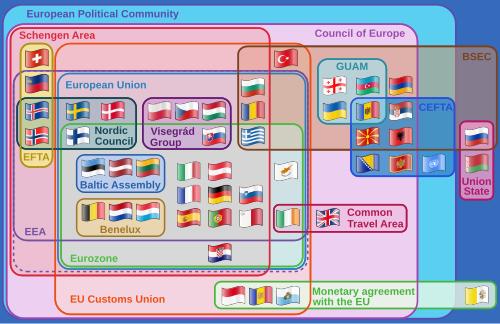

European Union Customs Union

View on Wikipedia

Key Information

The European Union Customs Union (EUCU), formally known as the Community Customs Union, is a customs union which consists of all the member states of the European Union (EU), Monaco, and the British Overseas Territory of Akrotiri and Dhekelia. Some detached territories of EU states do not participate in the customs union, usually as a result of their geographic separation.[a] In addition to the EUCU, the EU is in customs unions with Andorra, San Marino and Turkey (with the exceptions of certain goods),[b] through separate bilateral agreements.[2]

There are no tariffs or non-tariff barriers to trade between the members of the customs union and—unlike a free trade area—members of the customs union impose a common external tariff on all goods entering the union.[3]

The European Commission negotiates for and on behalf of the Union as a whole in international trade deals, rather than each member state negotiating individually. It also represents the Union in the World Trade Organization and any trade disputes mediated through it.

Common external tariffs

[edit]The EU Customs Union sets the tariff rates for imports to the EU from other countries. These rates are detailed and depend on the specific type of product imported, and can also vary by the time of year.[4] The full WTO Most Favoured Nation tariff rates apply only to those countries that do not have a Free Trade Agreement with the EU, or are not on a WTO recognised exemption scheme such as Everything but Arms (an EU support arrangement for Least Developed Countries).

Union and common transit

[edit]Union transit, formerly called "Community transit", is a system generally applicable to the movement of non-Union goods for which customs duties and other charges due on import have not been paid, and of Union goods, which, between their point of departure and point of destination in the EU, have to pass through the territory of a third country.[5]

The 'common' transit procedure is used for the movement of goods between the EU Member States, the EFTA countries (Iceland, Norway, Liechtenstein and Switzerland), Turkey (since 1 December 2012), North Macedonia (since 1 July 2015) and Serbia (since 1 February 2016). The operation of the common transit procedure with the UK is ensured as the UK has deposited its instrument of accession on 30 January 2019 with the Secretariat of the Council of the EU.[5] The procedure is based on the Convention of 20 May 1987 on a common transit procedure. The rules are effectively identical to those of the Union transit.[5]

Edward Kellett-Bowman MEP, as rapporteur for a European Parliament Committee of Inquiry, presented a report to the Parliament in February 1997 [6] which identified the removal of border controls and a lack of co-operation by member states as being responsible for a rise in organised crime and smuggling.[7] Kellett-Bowman's report led to the European Union setting up a customs investigation body and computerising transit-monitoring systems.[8]

Modernised Customs Code

[edit]The Modernised Customs Code (MCC) was adopted under Regulation (EC) No 450/2008 of the European Parliament and of the Council of 23 April 2008 laying down the Community Customs Code (Modernised Customs Code).[9] The MCC was primarily adopted to enable IT customs and trade solutions to be adopted.[10]

Union Customs Code

[edit]The Union Customs Code (UCC), intended to further modernise customs procedures, entered into force on 1 May 2016. This superseded the MCC.[10] The European Commission has stated that the aims of the UCC are simplicity, service and speed.[11] Implementation took place over a period of time and most aspects of implementation were complete by 31 December 2020, although some formalities managed by electronic systems may not be fully implemented until 31 December 2025.[12]

One major goal of the UCC is to progress towards the complete use of electronic systems for interactions between businesses and customs authorities, and between customs authorities, bringing all paper-based customs processes to an end.[13]

Non-EU participants

[edit]Monaco and the British Overseas Territory of Akrotiri and Dhekelia are integral parts of the EU's customs territory.[2][14]

| State / territory | Agreement | Entry into force |

|---|---|---|

| Franco-Monegasque Customs Convention[15][16][17] | 1968 | |

| Treaty of Accession 2003[18] Brexit withdrawal agreement[14] |

1 May 2004 |

EU territories with opt-outs

[edit]

While all EU member states are part of the customs union, not all of their respective territories participate. Territories of member states which have remained outside of the EU (overseas territories of the European Union) generally do not participate in the customs union.[19]

However, some territories within the EU do not participate in the customs union for tax and/or geographical reasons:

- Büsingen am Hochrhein (German exclave within Switzerland, part of the Swiss Customs Area)[20][21]

- Heligoland (small German archipelago in the North Sea with VAT free status)[20][19]

- Livigno (remote Alpine town in Italy with VAT free status)[20][21]

- Ceuta and Melilla (Spanish territories in Africa with VAT free status).[20][21]

Historical opt outs

[edit]The following territories were excluded until the end of 2019:

- Campione d'Italia (an exclave of Italy surrounded by Swiss territory)

- the Italian waters of Lake Lugano

Bilateral customs unions

[edit]Andorra, San Marino and Turkey are each in a customs union with the EU.[2]

| State | Agreement | Entry into force | Notes |

|---|---|---|---|

| Agreement in the form of an Exchange of Letters between the European Economic Community and the Principality of Andorra – Joint Declarations[22] | 1 January 1991 | Excludes agricultural produce | |

| Agreement on Cooperation and Customs Union between the European Economic Community and the Republic of San Marino[23] | 1 April 2002 | ||

| Decision No 1/95 of the EC-Turkey Association Council of 22 December 1995 on implementing the final phase of the Customs Union[24] | 31 December 1995 | Excludes agricultural produce |

Special arrangements concerning territories of the United Kingdom

[edit]The United Kingdom of Great Britain and Northern Ireland left the European Union on 31 January 2020 and transition arrangements ended on 31 December 2020. Special arrangements have been made for those parts of the United Kingdom and its territories that share a land border with an EU member state.

Northern Ireland

[edit]The UK (including Northern Ireland) is no longer a member of the European Union Customs Union. However, there are special arrangements in place for Northern Ireland: its trade with Great Britain and its trade with the European Union are each now regulated by the Brexit withdrawal agreement (specifically the Northern Ireland Protocol and the Windsor Framework), the EU–UK Trade and Cooperation Agreement, the European Union (Future Relationship) Act 2020, the United Kingdom Internal Market Act 2020. These include special provisions for trade in goods between Northern Ireland and the EU which for many purposes are similar to those that apply within the Customs Union, although Northern Ireland remains part of United Kingdom Customs territory.

Gibraltar

[edit]Gibraltar left the EU concurrently with the United Kingdom. When part of the EU, it was one of the EU territories with opt-outs and had not been part of the Customs Union. An agreement in principle has been reached between the EU, the United Kingdom, and Gibraltar to negotiate a treaty which would include provisions for trade on goods between the EU and Gibraltar.[25] These would be "substantially similar" to those within the Customs Union. As of April 2024[update], the agreement has not yet been concluded.

Akrotiri and Dhekelia

[edit]As already noted above, the British Overseas Territory of Akrotiri and Dhekelia on the island of Cyprus are integral parts of the EU's customs territory (and remained so after Brexit).

See also

[edit]- Community preference – Former principle of EU governance

- European Union value added tax – EU-wide goods and services tax policy

- European Customs Information Portal – EU Import/Export information service

- European Economic Area (EU and EFTA except Switzerland)

- European Free Trade Association (EFTA)

- European integration – Process of political, economic, social, and cultural integration of states in and around Europe

- European Single Market – Single market of the European Union and participating non-EU countries

- European Union–Turkey Customs Union – Customs union between Turkey and European Union

- Free trade agreements of the European Union – Overview of free trade agreements in the European Union

- Free trade areas in Europe – EU, EFTA, CEFTA, CISFTA, GUAM, BAFTA

- Free-trade area – Regional trade agreement

- Market access – Ability to sell goods and services across borders

- Non-tariff barriers to trade – Other types of trade barriers

- Rules of origin – Rules to attribute a country of origin to a product

- Tariff – Goods import or export tax

Explanatory footnotes

[edit]- ^ For example, Büsingen am Hochrhein, an exclave of Germany within Switzerland.

- ^ See European Union–Turkey Customs Union.

References

[edit]- ^ Dinan, Desmond (2014). Europe Recast: A History of European Union (2nd ed.). Basingstoke, New York: Palgrave Macmillan. p. 88. ISBN 978-0-333-69352-0.

- ^ a b c Customs unions, Taxation and Customs Union Archived 17 August 2016 at the Wayback Machine, European Commission. Retrieved 20 August 2016.

- ^ Erskine, Daniel H (2006). "The United States-EC Dispute Over Customs Matters: Trade Facilitation, Customs Unions, and the Meaning of WTO Obligations". Florida Journal of International Law. 18: 432–485. SSRN 987367.

- ^ Taric and Quota Data & Information Archived 24 July 2019 at the Wayback Machine – European Commission Communication and Information Resource Centre for Administrations, Businesses and Citizens.

- ^ a b c European Union, Union and Common Transit Archived 9 August 2020 at the Wayback Machine, accessed 24 December 2020

Text was copied from this source, which is available under a Creative Commons Attribution 4.0 International License Archived 16 October 2017 at the Wayback Machine.

Text was copied from this source, which is available under a Creative Commons Attribution 4.0 International License Archived 16 October 2017 at the Wayback Machine.

- ^ European Parliament, Report on the Community Transit System Archived 19 January 2022 at the Wayback Machine, 20 February 1997, accessed 31 January 2017

- ^ Neil Buckley, "Cross-border crime loses EU billions: Inquiry blames Brussels and customs for failing to clamp down on smuggling", Financial Times, 21 February 1997, p. 2.

- ^ Neil Buckley, "EU plans single body against smuggling", Financial Times, 13 March 1997, p. 2.

- ^ OJ L 145, published 4 June 2008

- ^ a b Deloitte Netherlands, "In 2016 the European Union will have a new Customs Code. But what’s new?", published 17 December 2014, accessed 11 December 2023.

- ^ "Union Customs Code". Taxation and customs union – European Commission. Archived from the original on 17 August 2016. Retrieved 25 May 2016.

- ^ European Commission, "The Union Customs Code (UCC) – Introduction". Archived 31 May 2019 at the Wayback Machine, accessed 29 March 2023.

- ^ European Commission, "Proposal for a Regulation of the European Parliament and of the Council amending Regulation (EU) No 952/2013 to prolong the transitional use of means other than the electronic data-processing techniques provided for in the Union Customs Code", COM(2018) 85 final, published 2 March 2018, accessed 29 March 2023. Archived 5 June 2023 at the Wayback Machine.

- ^ a b Protocol relating to the Sovereign Base Areas of the United Kingdom of Great Britain and Northern Ireland in Cyprus Archived 11 October 2021 at the Wayback Machine, Agreement on the withdrawal of the United Kingdom of Great Britain and Northern Ireland from the European Union and the European Atomic Energy Community, EUR-Lex, 12 November 2019.

- ^ "Taxation and Customs – FAQ". European Commission. Archived from the original on 8 June 2012. Retrieved 12 September 2012.

- ^ "Council Regulation (EEC) No 2913/92 of 12 October 1992 establishing the Community Customs Code". Official Journal of the European Union. 19 October 1992. Archived from the original on 29 July 2017. Retrieved 12 September 2012.

- ^ "Monaco and the European Union". Gouvernement Princier. Archived from the original on 20 January 2021. Retrieved 31 January 2021.

- ^ Protocol No. 3 on the Sovereign Base Areas of the United Kingdom of Great Britain and Northern Ireland in Cyprus Archived 13 November 2020 at the Wayback Machine, Act concerning the conditions of accession of the Czech Republic, the Republic of Estonia, the Republic of Cyprus, the Republic of Latvia, the Republic of Lithuania, the Republic of Hungary, the Republic of Malta, the Republic of Poland, the Republic of Slovenia and the Slovak Republic and the adjustments to the Treaties on which the European Union is founded, EUR-Lex, 23 September 2003.

- ^ a b Territorial status of EU countries and certain territories Archived 3 July 2021 at the Wayback Machine – European Commission, retrieved 18 December 2018

- ^ a b c d Article 6 of Council Directive 2006/112/EC Archived 29 June 2019 at the Wayback Machine, 28 November 2006

- ^ a b c "REGULATION (EU) No 952/2013 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 9 October 2013 laying down the Union Customs Code, Article 4" (PDF). EURLEX. October 2013. p. 11. Archived from the original on 14 August 2019. Retrieved 17 December 2018.

- ^ "Andorra: Customs Unions and preferential arrangements". European Commission. Archived from the original on 26 October 2012. Retrieved 12 September 2012.

- ^ "Agreement on Cooperation and Customs Union between the European Economic Community and the Republic of San Marino". Archived from the original on 7 April 2013. Retrieved 15 July 2015.

- ^ "Decision No 1/95 of the EC-Turkey Association Council of 22 December 1995 on implementing the final phase of the Customs Union" (PDF). Archived (PDF) from the original on 19 March 2013.

- ^ Martin, Maria; González, Miguel (11 January 2021). "Deal between Spain and UK plans to eliminate Gibraltar border checkpoint". El País. Madrid. Archived from the original on 25 May 2023. Retrieved 29 January 2021.

External links

[edit]- TARIC database enquiry system, gives current tariff rates applicable by exporting country and season – European Commission: Communication and Information Resource Centre for Administrations, Businesses and Citizens.

- TARIC and Quota Data & Information: user guides for the TARIC database above – European Commission: Communication and Information Resource Centre for Administrations, Businesses and Citizens.

- "Turkey border gridlock hints at pain to come for Brexit Britain". Financial Times, February 16, 2017

European Union Customs Union

View on GrokipediaHistory

Establishment in the European Economic Community

The Treaty establishing the European Economic Community (EEC), signed on 25 March 1957 in Rome by Belgium, France, the Federal Republic of Germany, Italy, Luxembourg, and the Netherlands, laid the groundwork for the EEC's customs union as a core component of its common market objectives.[9][10] The treaty entered into force on 1 January 1958, marking the formal inception of the EEC and initiating the process toward a customs union that prohibited internal customs duties and quantitative restrictions on trade while establishing a common external tariff.[11] Article 9 of the treaty explicitly defined the EEC as based on a customs union encompassing all goods trade, requiring member states to eliminate customs duties and equivalent charges between themselves and to apply a uniform customs tariff to imports from non-members.[12] This structure aimed to create a homogeneous economic area by progressively dismantling internal barriers and harmonizing external trade policy, with the common external tariff calculated as the arithmetic mean of the pre-existing national tariffs of the six members, subject to adjustments through international negotiations.[13] Implementation occurred over a transitional period originally planned to span 12 years from 1958 to 1970, but accelerated through staged reductions: the treaty mandated a 10% initial cut in internal duties effective from the entry into force, followed by nine further annual 10% reductions, alongside a relaxation of up to 20% on global import quotas.[14] By July 1968, all internal customs duties and quantitative restrictions among the six members had been fully eliminated, and the common external tariff was comprehensively applied, two years ahead of the original schedule due to political momentum and fewer disputes than anticipated in areas like agriculture.[3] This completion solidified the customs union as operational, fostering intra-EEC trade growth from approximately 30% of members' total trade in 1958 to over 50% by the early 1970s, as evidenced by subsequent economic data.[14]Expansion and Institutional Evolution

The European Union Customs Union, initially comprising the six founding members of the European Economic Community—Belgium, France, Italy, Luxembourg, the Netherlands, and West Germany—fully entered into force on 1 July 1968, following phased reductions in internal tariffs and the adoption of a common external tariff as stipulated in the Treaty of Rome.[3] Expansion occurred concurrently with successive EU enlargements, as new member states automatically acceded to the Customs Union without opt-outs, extending the common external tariff and internal free movement of goods to additional territories.[15] The first enlargement took place on 1 January 1973, incorporating Denmark, Ireland, and the United Kingdom, increasing membership to nine states.[15] Greece joined on 1 January 1981, followed by Portugal and Spain on 1 January 1986, bringing the total to twelve members.[15] The 1995 accession of Austria, Finland, and Sweden on 1 January raised the number to fifteen.[15] The largest single expansion occurred on 1 May 2004 with ten Central and Eastern European states—Cyprus, Czechia, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Slovakia, and Slovenia—elevating participation to twenty-five members and significantly broadening the Union's geographic and economic scope.[3][15] Bulgaria and Romania acceded on 1 January 2007, followed by Croatia on 1 July 2013, reaching twenty-eight members until the United Kingdom's withdrawal from the EU and Customs Union on 31 January 2020, reducing the current count to twenty-seven.[15] Institutionally, the Customs Union evolved from a framework of national administrations applying harmonized rules toward greater centralization and uniformity under EU-level oversight by the European Commission, which sets the common tariff nomenclature (Combined Nomenclature) and enforces compliance.[3] The 1992 Community Customs Code standardized procedures across members, replacing disparate national codes and mandating uniform application of customs legislation by 1993 to support the single market's free movement of goods.[3] Subsequent developments emphasized risk management and digital integration: the 1987 introduction of the Single Administrative Document facilitated common transit procedures, while the 1994 launch of the TARIC (Integrated Tariff of the European Communities) database digitized tariff application.[3] By 2003, a computerized transit system (NCTS) was operational, and in 2005, the EU Customs Risk Management Framework was established to prioritize high-risk consignments over routine checks.[3] Further refinements included the 2008 Authorised Economic Operator (AEO) program, granting certified traders simplified procedures based on compliance history, and the 2011 adoption of common security risk criteria to address threats like illicit trade.[3] The 2013 Union Customs Code, effective from 1 May 2016, consolidated and modernized the 1992 code, introducing data-driven controls, binding tariff information, and enhanced cooperation among national customs authorities via EU-wide IT systems, reflecting a shift toward efficiency amid growing trade volumes post-enlargements.[3] These changes maintained the Customs Union's core principle of non-discrimination in tariff application while adapting to enforcement challenges from expanded membership and global supply chain complexities.[3]Recent Reforms and Digitalization Efforts

In May 2023, the European Commission proposed a major overhaul of the Union Customs Code (UCC), the primary legislative framework governing the EU Customs Union since 2013, to enhance digitalization, simplify procedures, and bolster enforcement amid rising e-commerce volumes and supply chain complexities. The reform package includes the creation of a centralized EU Customs Data Hub, a single-window digital platform designed to replace disparate national IT systems, enabling seamless electronic submission of customs declarations, proofs of origin, and compliance data across all Member States. This initiative targets a full transition to paperless customs by 2025, aiming to cut administrative costs for businesses by up to 20% through automated data validation and reduced manual interventions.[16][17] Central to the digitalization push is the establishment of an EU Customs Authority, tasked with managing the Data Hub's operations, standardizing risk assessment algorithms, and coordinating cross-border data sharing to combat fraud, which costs the EU an estimated €15-20 billion annually in lost revenues. The proposal mandates electronic filing for all import/export declarations, integrates artificial intelligence for real-time risk profiling, and introduces centralized clearance options for trusted traders, allowing declarations at a single EU entry point regardless of destination. These measures address longstanding fragmentation, where varying national implementations have led to inconsistencies in tariff application and valuation disputes.[18][19] Implementation milestones include the rollout of the electronic Proof of Union Status (PoUS) system from March 2024, replacing paper-based T2L(F) transit documents with digital equivalents to verify goods' free circulation status within the Union, thereby expediting internal movements and reducing border delays. By June 2025, Member States reached a common position on the revised UCC, advancing negotiations toward adoption, though concerns persist over data privacy under GDPR integration and the potential resource strain on smaller customs administrations. This aligns with the EU Customs Strategy's 17-action plan through 2025, which emphasizes interoperability with global trade systems like the World Customs Organization's standards to maintain competitiveness.[16][18] The reforms also incorporate post-Brexit adaptations, such as enhanced controls on Northern Ireland Protocol goods via the Windsor Framework, with phased digital upgrades through July 2025 to minimize disruptions. While industry stakeholders welcome the efficiency gains, critics argue the centralized model risks over-reliance on a single IT infrastructure vulnerable to cyberattacks, underscoring the need for robust contingency protocols. Overall, these efforts seek to evolve the Customs Union from a tariff-focused mechanism into a data-driven enforcement network, though full efficacy depends on uniform Member State adoption.[18]Legal and Institutional Framework

Foundational Treaties and Principles

The European Union Customs Union traces its origins to the Treaty establishing the European Economic Community (EEC Treaty), signed on 25 March 1957 in Rome by Belgium, France, Italy, Luxembourg, the Netherlands, and the Federal Republic of Germany, and entering into force on 1 January 1958. This treaty laid the groundwork for the customs union by mandating the progressive elimination of customs duties and quantitative restrictions on trade between member states, alongside the establishment of a common customs tariff toward third countries, with the goal of fostering economic interdependence and preventing future conflicts through integrated markets.[13] Article 3 of the EEC Treaty explicitly designated the customs union as a foundational element of the Community, covering all goods trade and requiring completion within a transitional period ending by 1 July 1968, when internal tariffs were fully abolished and the common external tariff was uniformly applied.[12] Core principles of the customs union, as enshrined in the EEC Treaty and later consolidated in the Treaty on the Functioning of the European Union (TFEU) following amendments via the Treaty of Maastricht (1992), Treaty of Amsterdam (1997), Treaty of Nice (2001), and Treaty of Lisbon (2007), emphasize the prohibition of customs duties on imports and exports between member states, alongside bans on charges having equivalent effect that could distort competition or impede free movement of goods.[20] Article 28(1) TFEU reaffirms that the Union comprises a customs union involving no internal duties or equivalent charges and a common customs tariff for relations with non-members, while Article 30 TFEU explicitly prohibits such internal duties, and Article 31 enables the Council to enact measures for the common tariff's administration.[21] These principles rest on causal mechanisms of tariff equalization to eliminate trade diversion risks inherent in mere free trade areas, ensuring that intra-union trade responds to comparative advantages rather than protectionist distortions, as evidenced by the treaty's requirement for a unified tariff schedule derived from averaging members' pre-existing rates (with reductions for concessions under GATT).[22] The customs union's framework also integrates a common commercial policy, originally under Articles 110-116 of the EEC Treaty and now Article 207 TFEU, granting exclusive EU competence over trade agreements affecting tariffs and export policy to maintain uniformity and prevent member states from undermining the external tariff through bilateral deals. This exclusivity stems from first-principles recognition that fragmented external policies would erode the internal union's integrity, as unilateral concessions by one member could shift trade flows and revenue losses across the bloc; empirical data from the 1960s transition shows tariff reductions averaging 20-30% on industrial goods, boosting intra-EEC trade from 30% of members' total in 1958 to over 50% by 1970 without internal barriers.[23] Subsequent treaties preserved these tenets while adapting to enlargement, with protocols ensuring acceding states align tariffs upon entry, thus extending the union's scope without altering its foundational logic.[5]Union Customs Code and Regulatory Updates

The Union Customs Code (UCC), established by Regulation (EU) No 952/2013 of the European Parliament and of the Council, was adopted on 9 October 2013 and entered into force on 30 October 2013, with full applicability from 1 May 2016.[24] [25] This recast legislation replaced the prior Community Customs Code, providing a unified framework for customs procedures across the EU, including rules for declaring goods entering or leaving the customs territory, determining customs value, and applying duties and taxes. The UCC emphasizes simplification, risk management, and alignment with international standards from the World Customs Organization, while mandating electronic data interchange for declarations to enhance efficiency and security.[26] The UCC is supplemented by secondary legislation, including the Delegated Act (Regulation (EU) 2015/2446), which details provisions on guarantees and authorizations, and the Implementing Act (Regulation (EU) 2015/2447), covering operational procedures such as proofs of customs status and transit.[25] A Transitional Delegated Act (Regulation (EU) 2016/341) addressed legacy systems during the shift to full digitalization, allowing paper-based processes until systems like the Automated Export System were fully deployed.[25] These elements collectively enforce the common external tariff and eliminate internal barriers, with customs authorities empowered to conduct post-clearance audits and recover duties where declarations are inaccurate. Regulatory updates since 2016 have focused on digital transformation and adaptation to e-commerce growth. In response to increasing low-value consignments, amendments via Commission Implementing Regulation (EU) 2018/1781 introduced simplified entry procedures for express shipments under €150, reducing paperwork while maintaining revenue controls.[26] Further, the UCC-Proof of Union Status project, launched post-2016, digitized certificates to verify goods' EU origin, aiding free circulation.[27] A major reform initiative began on 17 May 2023, when the European Commission proposed revisions to the UCC to accelerate full digitalization, harmonize enforcement, and introduce an EU-wide handling fee for non-compliant declarations to deter abuse.[16] The European Parliament adopted its position in March 2024, emphasizing stronger product safety checks and data analytics for risk assessment, while the Council secured a negotiating mandate on 27 June 2025 to streamline procedures and integrate AI-driven tools for customs valuation.[28] [29] This ongoing modernization, termed the Modernised Union Customs Code (MUCC), targets completion of interconnected systems like the New Computerised Transit System (NCTS) and Customs Decision Information System by late 2025, aiming to cut administrative burdens by up to 20% through mandatory electronic submissions and centralized data hubs.[27] As of October 2025, trilogue negotiations continue, with stakeholders urging swift adoption to address fragmented national implementations that have undermined uniform application.[30]Role of EU Institutions in Enforcement

The enforcement of the European Union Customs Union relies on a shared competence between EU institutions and member states' national customs authorities, with the latter handling operational controls at borders while EU bodies ensure uniform application of rules, oversight, and supranational accountability. The Union Customs Code (Regulation (EU) No 952/2013), which entered into force on 1 May 2016, establishes the legal framework for these mechanisms, mandating risk-based controls, data harmonization, and cooperation to prevent irregularities such as undervaluation, smuggling, and non-compliance with the common external tariff. National authorities conduct the majority of customs declarations and inspections—processing over 250 million import/export declarations annually as of 2022—but must apply EU-wide standards, with the Commission providing binding guidelines and IT systems like the Customs Risk Management Framework (CRMF).[31] The European Commission, through its Directorate-General for Taxation and Customs Union (DG TAXUD), plays a central role in strategic enforcement by developing policies, negotiating international agreements, and supervising member states' implementation. DG TAXUD coordinates the EU's customs IT infrastructure, including the Import Control System 2 (ICS2) deployed progressively since 2021 for pre-arrival security data, and leads risk analysis via the Customs Risk Information System (CRIS), which flagged over 1.2 million high-risk consignments in 2023. The Commission also initiates infringement proceedings under Article 258 of the Treaty on the Functioning of the European Union (TFEU) against non-compliant states; for instance, it pursued cases against several members in 2022-2023 for inadequate controls on textile imports from China, recovering €200 million in evaded duties. Additionally, the European Anti-Fraud Office (OLAF), under Commission oversight, investigates cross-border fraud, conducting 150 customs-related probes in 2022 alone.[32][33] The Council of the European Union and the European Parliament adopt secondary legislation, such as updates to the UCC, ensuring democratic input into enforcement tools like tariff suspensions and anti-dumping measures; the Council, representing member states, holds particular sway over revenue-sensitive decisions, as customs duties contribute approximately €20 billion annually to the EU budget (around 10% of total revenue in 2023). The Court of Justice of the EU (CJEU) enforces uniformity through preliminary rulings and direct actions; in cases like Hewlett-Packard Belgium (C-65/22, 2023), it clarified valuation rules for post-import price adjustments, mandating inclusion of such elements in customs bases to prevent revenue loss, while infringement judgments have compelled states to strengthen controls, as in proceedings against Italy and Greece for systemic failures in origin verification between 2019 and 2024.[34][35] Ongoing reforms, agreed in June 2025, aim to enhance institutional enforcement by introducing an EU-wide handling fee for low-value consignments and bolstering centralized risk profiling, though operational reliance on national authorities persists to avoid supranational overreach; critics, including business groups, argue that fragmented enforcement—evident in varying detention rates across states (e.g., 5% in Germany vs. 12% in Poland in 2023 data)—undermines the union's integrity, prompting calls for a dedicated EU Customs Authority, though proposals remain in legislative limbo as of October 2025.[36][30]Core Operational Features

Common External Tariff Application

The Common External Tariff (CET) forms the core of the EU Customs Union's external trade policy, imposing uniform duties on imports from non-EU countries entering any member state's external border, thereby preventing tariff circumvention and protecting the internal market's integrity. This uniformity is mandated by the EU Treaties and operationalized through the Common Customs Tariff (CCT), which applies identically across all entry points without variation by member state. Customs duties are calculated based on the customs value of goods, typically their transaction value plus adjustments for transport and insurance, ensuring consistent revenue collection and trade deflection avoidance.[37] Application begins with the classification of imported goods using the Combined Nomenclature (CN), an EU-specific extension of the World Customs Organization's Harmonized System, featuring eight-digit codes updated annually via Council Regulation (e.g., applicable from January 1, 2025). Importers or their agents declare the CN code, country of origin, and other details via the Single Administrative Document (SAD) or electronic equivalents under the Union Customs Code (UCC), which has governed procedures since May 1, 2016. Customs authorities verify classification, often issuing binding tariff information (BTI) for certainty, with misclassification penalties enforceable under national laws aligned to EU standards.[38][6][39] Tariff rates are retrieved from the TARIC (Integrated Tariff of the European Communities) database, a daily-updated multilingual system integrating the CET's ad valorem rates—averaging around 5% for industrial goods—with supplementary measures like anti-dumping duties (e.g., up to 50% on certain steel imports from specific origins), countervailing duties, and safeguard quotas. For agricultural products, specific duties (e.g., € per kg) or compound rates may apply, alongside tariff quotas limiting duty-free or reduced-rate imports (e.g., 1.3 million tons annually for poultry under WTO agreements). Preferential rates reduce or eliminate duties for eligible third countries under free trade agreements (FTAs, covering over 70 partners as of 2024) or the Generalized Scheme of Preferences (GSP), verified via certificates of origin.[40][37] Enforcement relies on national customs administrations of the member state of import, which collect the duties, retaining 25% to cover collection costs and as an incentive for efficient enforcement, while transferring the remaining 75% to the EU budget. These administrations operate under EU oversight, with risk-based controls at borders using shared IT systems like the Customs Decision System for BTIs and the Import Control System 2 (ICS2) for pre-arrival data since 2021. Uniformity is reinforced by the UCC's requirement for equivalent treatment, Commission audits, and adjudication by the Court of Justice of the EU for disputes, preventing member states from deviating to favor domestic interests. Autonomous tariff suspensions, granted for raw materials not produced sufficiently in the EU (e.g., certain chemicals under annual Council acts), provide temporary duty relief to support manufacturing competitiveness.[41][42][39]Elimination of Internal Customs Barriers

The elimination of internal customs barriers constitutes a foundational element of the EU Customs Union, prohibiting customs duties on imports and exports between member states, as well as any charges having equivalent effect, under Articles 28–30 of the Treaty on the Functioning of the European Union (TFEU). This includes shipments and packages, for which there are no customs duties or extra fees. For example, no customs duties apply to goods shipped from Croatia to Denmark in 2025 or 2026, as both are EU member states in the customs union, allowing free movement of goods without tariffs; changes in 2026, such as the €3 duty on low-value parcels under €150, apply only to imports from outside the EU, not intra-EU trade.[43][44][45] This principle, rooted in the Treaty of Rome signed on March 25, 1957, mandated the progressive abolition of such duties and quantitative restrictions over a transitional period ending in 1968, fostering the free circulation of goods across the internal market.[3] Quantitative restrictions and measures equivalent thereto are similarly banned under TFEU Articles 34–35, ensuring no quotas or discriminatory practices impede intra-EU trade flows.[45] The process commenced with the establishment of the European Economic Community (EEC) on January 1, 1958, among the six founding members—Belgium, France, West Germany, Italy, Luxembourg, and the Netherlands—through staged tariff reductions: an initial 10% cut in 1959, followed by annual 20% decreases from 1960, culminating in the complete removal of internal duties and restrictions on July 1, 1968.[3] Concurrently, a common external tariff was applied to imports from non-members, unifying trade policy.[3] For subsequent accessions, new members integrate by immediately adopting the common tariff and eliminating internal barriers; for instance, the 2004 enlargement to ten additional states (including Cyprus, Czech Republic, Estonia, Hungary, Latvia, Lithuania, Malta, Poland, Slovakia, and Slovenia) extended the union without reimposing intra-EU duties.[3] In operational terms, goods in free circulation—those originating in the EU or cleared through external customs without unpaid duties—move without internal declarations, tariffs, or routine border checks, with controls consolidated at external frontiers to prevent fraud and protect health standards.[1] The 1993 completion of the single market further eradicated remaining formalities, such as systematic customs documentation at internal borders, enabling seamless logistics; EU customs authorities function as a unified system, sharing data via the Customs Information System to enforce compliance.[3][1] Violations, including unauthorized charges, are actionable before the Court of Justice of the EU, which has upheld the prohibition through rulings interpreting "equivalent effect" broadly to include discriminatory fiscal measures.[45] This framework has facilitated intra-EU trade volumes exceeding €3.6 trillion annually as of 2022, though non-customs barriers like divergent technical regulations persist and are addressed separately via harmonization directives.[46] The system's integrity relies on mutual trust among members, with safeguards against circumvention, such as rules of origin verification for preferential treatment claims.[1]Common Commercial Policy and Transit Procedures

The European Union's Common Commercial Policy (CCP) constitutes the external trade framework integral to the Customs Union, encompassing uniform measures on imports, exports, and trade relations with non-member states to prevent trade deflection and ensure consistent application across member states.[47] Enshrined in Articles 206 and 207 of the Treaty on the Functioning of the European Union (TFEU), the CCP grants the EU exclusive competence over trade in goods, while extending to services, intellectual property, and foreign direct investment aspects affecting trade, thereby centralizing negotiation authority with the European Commission on behalf of all members.[48] This policy underpins the Common External Tariff (CET), a harmonized schedule of duties applied to goods entering the EU from third countries, calculated via the Combined Nomenclature (CN) classification system based on the Harmonized System, with average applied tariffs around 5.1% for industrial goods as of 2023 data.[37] The CET, uniformly enforced at external borders, eliminates discrepancies in tariff levels that could otherwise incentivize imports through lower-duty members, a core causal mechanism for the Customs Union's integrity since its inception in 1968.[47] Beyond tariffs, the CCP incorporates non-tariff measures such as quotas, anti-dumping duties, and safeguard actions, with the Commission managing over 70 free trade agreements as of 2024, covering approximately 40% of EU imports, to strategically lower barriers while protecting domestic industries from unfair practices.[49] Empirical evidence from EU trade statistics indicates that this unified approach has diverted trade flows toward preferential partners, with intra-EU trade volumes exceeding €3.6 trillion in 2022, partly attributable to the policy's role in standardizing external barriers.[50] Complementing the CCP, transit procedures within the Customs Union facilitate the movement of goods not yet in free circulation, suspending duties, taxes, and commercial policy measures until the final destination to minimize administrative burdens and logistical costs.[51] The Union Transit Procedure, governed by the Union Customs Code (UCC) since its 2016 implementation, applies to operations between EU member states, Andorra, and San Marino, utilizing the T1 procedure for non-EU goods and T2 for certain EU goods requiring proof of status, processed electronically via the New Computerised Transit System (NCTS).[52] This system requires a transit guarantee—often a bond or authorization—to cover potential duties, with over 25 million declarations processed annually as of recent figures, enabling seamless cross-border transport without intermediate customs clearance and reducing evasion risks through real-time tracking.[53] Transit operations under the UCC stipulate strict timelines, such as completion within specified periods based on distance and transport mode, with penalties for non-compliance including guarantee calls and fines up to €10,000 per infraction in some member states.[54] The procedure's suspensive nature—holding duties in abeyance—relies on causal safeguards like sealed consignments and authorized operators, empirically demonstrated to handle high volumes efficiently, as evidenced by the EU's transit facilitation aligning with WTO Trade Facilitation Agreement standards implemented progressively since 2017.[55] Common transit extensions apply to associated states like Turkey under separate conventions, but within the core Union, these mechanisms ensure the Customs Union's operational cohesion by decoupling internal movement from external tariff enforcement.[52]Scope and Participants

Coverage of EU Member States

The European Union Customs Union encompasses the customs territories of all 27 member states, establishing a unified area where internal borders do not impose customs duties or controls on goods movement, while a common external tariff applies to imports from third countries.[2] This coverage is automatic upon EU accession, as membership requires adherence to the Union's customs provisions under the Treaty on the Functioning of the European Union (TFEU), Articles 28–32. No EU member state has opted out of the core Customs Union framework, distinguishing it from partial opt-outs in areas like the Schengen Area or the eurozone.[56] The participating member states, listed alphabetically with their EU accession dates (marking integration into the Customs Union), are:| Country | Accession Date |

|---|---|

| Austria | 1 January 1995 |

| Belgium | 1 January 1958 |

| Bulgaria | 1 January 2007 |

| Croatia | 1 July 2013 |

| Cyprus | 1 May 2004 |

| Czech Republic | 1 May 2004 |

| Denmark | 1 January 1973 |

| Estonia | 1 May 2004 |

| Finland | 1 January 1995 |

| France | 1 January 1958 |

| Germany | 1 January 1958 |

| Greece | 1 January 1981 |

| Hungary | 1 May 2004 |

| Ireland | 1 January 1973 |

| Italy | 1 January 1958 |

| Latvia | 1 May 2004 |

| Lithuania | 1 May 2004 |

| Luxembourg | 1 January 1958 |

| Malta | 1 May 2004 |

| Netherlands | 1 January 1958 |

| Poland | 1 May 2004 |

| Portugal | 1 January 1986 |

| Romania | 1 January 2007 |

| Slovakia | 1 May 2004 |

| Slovenia | 1 May 2004 |

| Spain | 1 January 1986 |

| Sweden | 1 January 1995 |

Non-EU Countries with Full or Partial Integration

The European Union Customs Union extends to several non-EU sovereign states through bilateral agreements that establish full or partial alignment with its common external tariff and internal free movement of goods, facilitating tariff-free trade while requiring adherence to EU regulatory standards for originating products. These arrangements, distinct from EU membership, allow participating countries to benefit from the Union's trade policy without participating in its decision-making processes. As of 2025, the primary non-EU participants are Turkey, Andorra, San Marino, and Monaco, each with tailored scopes that exclude certain sectors like agriculture or services.[58][59][60][61] Turkey maintains the most extensive partial integration via the EU-Turkey Customs Union, effective from 1 January 1996 following the 1963 Ankara Association Agreement and its 1970 Additional Protocol. This covers industrial goods and processed agricultural products originating in either party, subjecting imports from third countries to the EU's common external tariff, while prohibiting quantitative restrictions and ensuring free circulation of compliant goods. Exclusions include unprocessed agricultural products, coal, steel, services, intellectual property rights, public procurement, and dispute settlement mechanisms beyond WTO frameworks, leading to ongoing negotiations for modernization since 2016 to address these gaps and incorporate EU free trade agreements.[62][63][58] Andorra participates through a customs union agreement signed in 1990 and effective from 1 July 1991, limited to industrial products under Chapters 25 to 97 of the Harmonized System nomenclature. Andorra applies the EU common external tariff on third-country imports in these categories, with free movement granted to EU-originating goods upon proof of compliance with EU rules of origin; agricultural products remain outside this scope, handled via separate preferential arrangements. This setup aligns Andorra's trade policy with the EU without extending to services or capital movements.[59][64] San Marino's customs union, established by agreement in 1991 and covering all products except coal and steel, enables tariff-free circulation of goods originating from either side after verification against EU standards, with San Marino adopting the EU's common external tariff for non-EU imports. The arrangement includes provisions for joint customs controls at external borders and mutual recognition of product conformity assessments, though San Marino retains autonomy in fiscal policy and non-tariff measures outside the union's scope.[65][60] Monaco integrates into the EU Customs Union indirectly through its 1968 customs union with France, an EU member state, making it part of the EU's customs territory for goods trade. This requires Monaco to apply EU tariff schedules and rules of origin for imports from non-EU countries, with seamless movement of compliant goods to and from France and other EU states; excise duties and VAT are harmonized via French administration, though Monaco maintains independent monetary policy despite euro usage. The arrangement excludes Monaco from EU agricultural policy and fisheries.[61][66]| Country | Agreement Date | Scope | Key Exclusions |

|---|---|---|---|

| Turkey | 1 January 1996 | Industrial goods, processed agriculture | Unprocessed agriculture, services, public procurement |

| Andorra | 1 July 1991 | Industrial products (HS Chapters 25-97) | Agriculture, services |

| San Marino | 1991 | All goods except coal/steel | Fiscal policy autonomy |

| Monaco | Via France, 1968 | Goods, aligned with EU territory | Agriculture policy, fisheries |

Overseas Territories and Special Opt-Outs

The customs territory of the European Union, as defined under Article 4 of the Union Customs Code (Regulation (EU) No 952/2013), encompasses the territories of all Member States except for designated exclusions, primarily affecting certain overseas possessions and special enclaves.[25] Outermost regions (ORs)—geographically distant territories fully integrated into the EU's legal framework, including the customs union—apply the common external tariff and benefit from the elimination of internal barriers. These include France's Guadeloupe, Martinique, French Guiana, Réunion, and Mayotte (integrated as an OR since 2014); Portugal's Azores and Madeira archipelagos; and Spain's Canary Islands, which joined the customs territory in 1986 despite separate VAT arrangements.[57][67] In contrast, Overseas Countries and Territories (OCTs) associated with Denmark, France, and the Netherlands maintain autonomy in customs matters and are excluded from the EU customs territory, allowing them to set independent tariff policies while receiving preferential tariff treatment for exports to the EU under the Overseas Association Decision (Council Decision 2001/822/EC, as amended).[68][69] There are currently 13 such OCTs, including Greenland (Denmark, which opted out via a 1985 referendum, severing full EU ties while retaining fisheries access); France's New Caledonia, French Polynesia, Wallis and Futuna, Saint Pierre and Miquelon, and the French Southern and Antarctic Lands; and the Netherlands' Aruba, Curaçao, Sint Maarten, Bonaire, Sint Eustatius, and Saba.[70] These territories handle their own external trade relations, often negotiating separate agreements, which preserves local economic sovereignty but limits seamless integration with the EU's common commercial policy.[69] Special opt-outs within or adjacent to Member States' European territories further delineate the customs union's scope. Spain's autonomous cities of Ceuta and Melilla, located in North Africa, are excluded from the customs territory despite being integral parts of Spain constitutionally; they apply Spanish tariffs but operate outside the EU common external tariff, necessitating separate customs declarations for intra-EU trade.[57] Germany's Büsingen am Hochrhein enclave aligns with Swiss customs procedures under a 1965 agreement, exempting it from EU duties and VAT.[71] Italy's Livigno and the former Campione d'Italia enclave (reintegrated in 2020) enjoy fiscal exemptions for VAT and excise but remain within the customs territory for tariff purposes. The British Sovereign Base Areas of Akrotiri and Dhekelia in Cyprus, under UK sovereignty, were integrated into the EU customs territory upon Cyprus's 2004 accession and continue to apply EU rules despite the UK's 2020 withdrawal, as affirmed in the EU-UK Withdrawal Agreement.[57] These arrangements reflect historical, geographical, and political contingencies rather than uniform policy, ensuring the customs union's integrity while accommodating territorial anomalies.| Category | Examples | Customs Status | Key Features |

|---|---|---|---|

| Outermost Regions (Fully Integrated) | Guadeloupe, Martinique, French Guiana, Réunion, Mayotte (France); Azores, Madeira (Portugal); Canary Islands (Spain) | Included | Subject to common external tariff; full participation in internal free movement.[57] |

| Overseas Countries and Territories (OCTs, Excluded) | Greenland (Denmark); French Polynesia, New Caledonia (France); Aruba, Curaçao (Netherlands) | Excluded | Independent tariffs; preferential EU market access via association agreements.[68] |

| Special Opt-Out Enclaves/Territories | Ceuta, Melilla (Spain); Büsingen (Germany); Akrotiri and Dhekelia (UK bases in Cyprus) | Varied (mostly excluded or aligned externally) | Case-specific treaties; separate declarations for EU trade.[71][57] |