Community hub

Recent from talks

Contribute something

Nothing was collected or created yet.

Currency union

View on Wikipedia| Part of a series on |

| World trade |

|---|

|

A currency union (also known as monetary union) is an intergovernmental agreement that involves two or more states sharing the same currency. These states may not necessarily have any further integration (such as an economic and monetary union, which would have, in addition, a customs union and a single market).

There are three types of currency unions:

- Informal – unilateral adoption of a foreign currency.[1]

- Formal – adoption of foreign currency by virtue of bilateral or multilateral agreement with the monetary authority, sometimes supplemented by issue of local currency in currency peg regime.

- Formal with common policy – establishment by multiple countries of a common monetary policy and monetary authority for their common currency.

The theory of the optimal currency area addresses the question of how to determine what geographical regions should share a currency in order to maximize economic efficiency.[2]

Advantages and disadvantages

[edit]This section needs additional citations for verification. (August 2019) |

Implementing a new currency in a country is always a controversial topic because it has both many advantages and disadvantages. New currency has different impacts on businesses and individuals, which creates more points of view on the usefulness of currency unions. As a consequence, governmental institutions often struggle when they try to implement a new currency, for example by entering a currency union.

Advantages

[edit]- A currency union helps its members strengthen their competitiveness on a global scale and eliminate the exchange rate risk.

- Transactions among member states can be processed faster and their costs decrease since fees to banks are lower.[3]

- Prices are more transparent and so are easier to compare, which enables fair competition.

- The probability of a monetary crisis is lower. The more countries there are in the currency union, the more they are resistant to crisis.

Disadvantages

[edit]- The member states lose their sovereignty in monetary policy decisions. There is usually an institution (such as a central bank) that takes care of the monetary policymaking in the whole currency union.

- The risk of asymmetric "shocks" may occur. The criteria set by the currency union are never perfect, so a group of countries might be substantially worse off while the others are booming.

- Implementing a new currency causes high financial costs. Businesses and also single persons have to adapt to the new currency in their country, which includes costs for the businesses to prepare their management, employees, and they also need to inform their clients and process plenty of new data.

- Unlimited capital movement may cause moving most resources to the more productive regions at the expense of the less productive regions. The more productive regions tend to attract more capital in goods and services, which might avoid the less productive regions.[4][5]

Convergence and divergence

[edit]Convergence in terms of macroeconomics means that countries have a similar economic behaviour (similar inflation rates and economic growth). It is easier to form a currency union for countries with more convergence as these countries have the same or at least very similar goals. The European Monetary Union (EMU) is a contemporary model for forming currency unions. Membership in the EMU requires that countries follow a strictly defined set of criteria (the member states are required to have a specific rate of inflation, government deficit, government debt, long-term interest rates and exchange rate). Many other unions have adopted the view that convergence is necessary, so they now follow similar rules to aim the same direction.

Divergence is the exact opposite of convergence. Countries with different goals are very difficult to integrate in a single currency union. Their economic behaviour is completely different, which may lead to disagreements. Divergence is therefore not optimal for forming a currency union.[6]

History

[edit]The first currency unions were established in the 19th century. The German Zollverein came into existence in 1834, and by 1866, it included most of the German states. The fragmented states of the German Confederation agreed on common policies to increase trade and political unity.

The Latin Monetary Union, comprising France, Belgium, Italy, Switzerland, and Greece, existed between 1865 and 1927, with coinage made of gold and silver. Coins of each country were legal tender and freely interchangeable across the area. The union's success made other states join informally.

The Scandinavian Monetary Union, comprising Sweden, Denmark, and Norway, existed between 1873 and 1905 and used a currency based on gold. The system was dissolved by Sweden in 1924.[7]

A currency union among the British colonies and protectorates in Southeast Asia, namely the Federation of Malaya, North Borneo, Sarawak, Singapore and Brunei was established in 1952. The Malaya and British Borneo dollar, the common currency for circulation was issued by the Board of Commissioners of Currency, Malaya and British Borneo from 1953 until 1967. Following the cessation of the common currency arrangement, Malaysia (the combination of Federation of Malaya, North Borneo, Sarawak), Singapore and Brunei began issuing their own currencies. Contemporarily, a currency reunion of these countries might still be feasible based on the findings of economic convergence.[8][9]

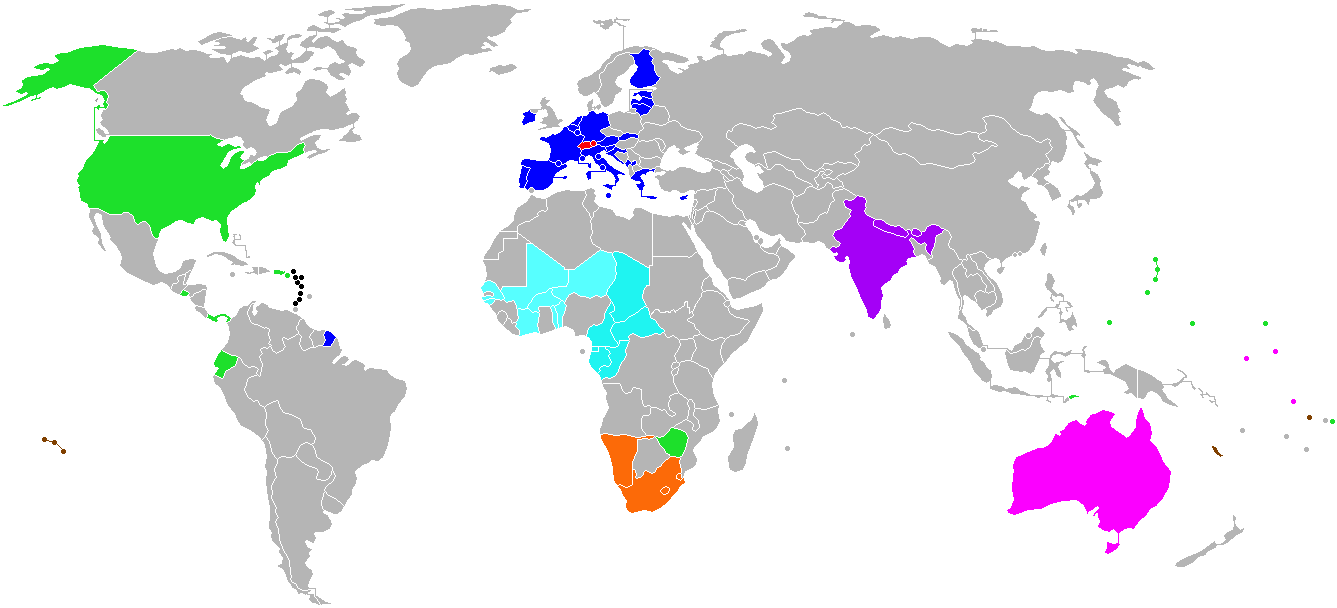

List of currency unions

[edit]Existing

[edit]Note: Every customs and monetary union and economic and monetary union also has a currency union.

![]() Zimbabwe is theoretically in a currency union with four blocs as the South African rand, Botswana pula, British pound and US dollar freely circulate. The US Dollar was, until 2016, official tender.[17]

Zimbabwe is theoretically in a currency union with four blocs as the South African rand, Botswana pula, British pound and US dollar freely circulate. The US Dollar was, until 2016, official tender.[17]

Additionally, the autonomous and dependent territories, such as some of the EU member state special territories, are sometimes treated as separate customs territory from their mainland state or have varying arrangements of formal or de facto customs union, common market and currency union (or combinations thereof) with the mainland and in regards to third countries through the trade pacts signed by the mainland state.[18]

Currency union in Europe

[edit]The European currency union is a part of the Economic and Monetary Union of the European Union (EMU). EMU was formed during the second half of the 20th century after historic agreements, such as Treaty of Paris (1951), Maastricht Treaty (1992). In 2002, the euro, a single European currency, was adopted by 12 member states. Currently, the Eurozone has 20 member states. The other members of the European Union are required to adopt the euro as their currency (except for Denmark, which has been given the right to opt out), but there has not been a specific date set. The main independent institution responsible for stability of the euro is the European Central Bank (ECB). The Eurosystem groups together the ECB and the national central banks (NCBs) of the Member States whose currency is the euro. The European System of Central Banks (ESCB) is made up of the ECB and the national central banks of all Member States of the European Union (EU), regardless of whether or not they have adopted the euro. The Governing Board consists of the Executive Committee of the ECB and the governors of individual national banks, and determines the monetary policy, as well as short-term monetary objectives, key interest rates and the extent of monetary reserves.[19]

Planned

[edit]| Community | Currency | Region | Target date | Notes |

|---|---|---|---|---|

| East African shilling | Africa | 2012 (not met), 2015 (not met), 2024 (not met),[20] 2031[21] | ||

| West African Monetary Zone | Eco | Africa | 2027 | Inside Economic Community of West African States, planned to eventually merge with West African franc |

| ASEAN+3 | Asian Monetary Unit [citation needed] | Asia | ? | a free trade agreements matrix partially established |

| Khaleeji | Arabian Peninsula | ? | Oman and the United Arab Emirates do not intend to adopt the currency at first but will do at a later date. | |

| Afro or Afriq | Africa | 2028[22] | Planned for 2028 or later | |

| Brazil, Argentina and possibly other countries | Sur | Latin America | ? | As Financial Times reports, Brazil and Argentina will announce in January 2023 that they are starting preparatory work on a common currency "Sur" (South). The initiative would later be extended to invite other Latin American nations.[23] |

Disbanded

[edit]- between

Bahrain and

Bahrain and  Abu Dhabi using the Bahraini dinar

Abu Dhabi using the Bahraini dinar - between

Bahrain,

Bahrain,  Kuwait,

Kuwait,  Oman,

Oman,  Qatar and the

Qatar and the  Trucial States, using the Gulf rupee from 1959 until 1966

Trucial States, using the Gulf rupee from 1959 until 1966 - between

Aden,

Aden,  South Arabia, Bahrain,

South Arabia, Bahrain,  Kenya, Kuwait, Oman, Qatar,

Kenya, Kuwait, Oman, Qatar,  British Somaliland, the Trucial States,

British Somaliland, the Trucial States,  Uganda,

Uganda,  Zanzibar and

Zanzibar and  British India (later independent

British India (later independent  India) using the Indian rupee until 1974

India) using the Indian rupee until 1974 - between

Belgium and the

Belgium and the  Grand-Duchy of Luxemburg (Belgium-Luxembourg Economic Union) using the Belgian/Luxembourgish franc from 1921 to the Euro

Grand-Duchy of Luxemburg (Belgium-Luxembourg Economic Union) using the Belgian/Luxembourgish franc from 1921 to the Euro - between British India and the

Straits Settlements (1837–1867) using the Indian rupee

Straits Settlements (1837–1867) using the Indian rupee - between

Czech Republic and

Czech Republic and  Slovakia (briefly from January 1, 1993 to February 8, 1993) using the Czechoslovak koruna

Slovakia (briefly from January 1, 1993 to February 8, 1993) using the Czechoslovak koruna - between

Ethiopia and

Ethiopia and  Eritrea using the Ethiopian birr

Eritrea using the Ethiopian birr - between

France,

France,  Monaco, and

Monaco, and  Andorra using the French franc

Andorra using the French franc - between

Austria-Hungary and

Austria-Hungary and  Liechtenstein using the Austro-Hungarian krone

Liechtenstein using the Austro-Hungarian krone - between the Eastern Caribbean,

Jamaica,

Jamaica,  Barbados,

Barbados,  Trinidad and Tobago and

Trinidad and Tobago and  British Guiana using the British West Indies dollar

British Guiana using the British West Indies dollar - between the Eastern Caribbean, Barbados, Trinidad and Tobago and British Guiana using the Eastern Caribbean dollar

- between

Italy,

Italy,  Vatican City, and

Vatican City, and  San Marino using the Italian lira

San Marino using the Italian lira - between

Jamaica and the

Jamaica and the  Cayman Islands using the Jamaican pound and later Jamaican dollar

Cayman Islands using the Jamaican pound and later Jamaican dollar - between Kenya, Uganda, and Zanzibar using the East African rupee

- between Kenya, Uganda, and Zanzibar (and later

Tanganyika) using the East African florin

Tanganyika) using the East African florin - between

Kenya, Tanganyika and

Kenya, Tanganyika and  Zanzibar (later merged as

Zanzibar (later merged as  Tanzania),

Tanzania),  Uganda, South Arabia, British Somaliland and

Uganda, South Arabia, British Somaliland and  Italian Somaliland using the East African shilling

Italian Somaliland using the East African shilling - Latin Monetary Union (1865–1927), initially between

France, Belgium,

France, Belgium,  Italy and

Italy and  Switzerland, and later involving

Switzerland, and later involving  Greece,[24]

Greece,[24]  Romania,

Romania,  Spain and other countries.

Spain and other countries. - between

Liberia and the

Liberia and the  United States using the United States dollar

United States using the United States dollar - between

Mauritius and

Mauritius and  Seychelles using the Mauritian rupee

Seychelles using the Mauritian rupee - between

Nigeria,

Nigeria,  the Gambia,

the Gambia,  Sierra Leone,

Sierra Leone,  the Gold Coast and Liberia using the British West African pound

the Gold Coast and Liberia using the British West African pound - between

Prussia and the North German states (1838–1857) using the North German thaler

Prussia and the North German states (1838–1857) using the North German thaler - between

Russia and the

Russia and the  former Soviet republics (1991–1993) using the Soviet ruble

former Soviet republics (1991–1993) using the Soviet ruble - between

Armenia and

Armenia and  Artsakh using the Armenian dram

Artsakh using the Armenian dram - between

Qatar and all the emirates of the

Qatar and all the emirates of the  United Arab Emirates, except Abu Dhabi using the Qatari and Dubai riyal

United Arab Emirates, except Abu Dhabi using the Qatari and Dubai riyal - between

Saudi Arabia and Qatar using the Saudi riyal

Saudi Arabia and Qatar using the Saudi riyal - between

Western Samoa and

Western Samoa and  New Zealand using the New Zealand pound

New Zealand using the New Zealand pound - Scandinavian Monetary Union (1870s until 1924), between

Denmark,

Denmark,  Norway and

Norway and  Sweden[24]

Sweden[24] - between the

Solomon Islands,

Solomon Islands,  Papua New Guinea and

Papua New Guinea and  Australia using the Australian dollar

Australia using the Australian dollar - between Australia, Papua,

New Guinea,

New Guinea,  Nauru,

Nauru,  the Solomon Islands, and

the Solomon Islands, and  the Gilbert and Ellice Islands using the Australian pound

the Gilbert and Ellice Islands using the Australian pound - between

Bavaria,

Bavaria,  Baden,

Baden,  Württemberg,

Württemberg,  Frankfurt, and

Frankfurt, and  Hohenzollern using the South German guilder

Hohenzollern using the South German guilder - between

Spain and Andorra using the Spanish peseta

Spain and Andorra using the Spanish peseta - between

Trinidad and Tobago and

Trinidad and Tobago and  Grenada using the Trinidad and Tobago dollar

Grenada using the Trinidad and Tobago dollar - between

Brunei,

Brunei,  Malaysia, and

Malaysia, and  Singapore (1953–1967) using the Malaya and British Borneo dollar

Singapore (1953–1967) using the Malaya and British Borneo dollar - between

Cambodia,

Cambodia,  Laos, Guangzhouwan,

Laos, Guangzhouwan,  Annam,

Annam,  Tonkin, and

Tonkin, and  Cochinchina (later

Cochinchina (later  Vietnam) between 1885 and 1952 using the French Indochinese piastre

Vietnam) between 1885 and 1952 using the French Indochinese piastre - between

South Africa, South West Africa, and

South Africa, South West Africa, and  Bechuanaland (later independent

Bechuanaland (later independent  Botswana) using the South African rand

Botswana) using the South African rand - between

Egypt,

Egypt,  Anglo-Egyptian Sudan, and

Anglo-Egyptian Sudan, and  Mandatory Palestine (until 1926) using the Egyptian pound

Mandatory Palestine (until 1926) using the Egyptian pound - between

West Germany and

West Germany and  East Germany between 1 July 1990 and 3 October 1990, as part of a temporary, so-called "Monetary, Economic and Social Union" prior to German reunification.

East Germany between 1 July 1990 and 3 October 1990, as part of a temporary, so-called "Monetary, Economic and Social Union" prior to German reunification. - between what ultimately became the

Republic of Ireland and the United Kingdom, between 1928 and 1979. The Irish Pound was held at exactly the same value as Sterling for this period, although it was not accepted for payments in the UK.

Republic of Ireland and the United Kingdom, between 1928 and 1979. The Irish Pound was held at exactly the same value as Sterling for this period, although it was not accepted for payments in the UK. - Yen Bloc (between 1905 and 1945), between the

Empire of Japan, the

Empire of Japan, the  Korean Empire,

Korean Empire,  Manchukuo,

Manchukuo,  Mengjiang, the

Mengjiang, the  Wang Jingwei regime, and Japanese-occupied Southeast Asia prior to and during World War II.

Wang Jingwei regime, and Japanese-occupied Southeast Asia prior to and during World War II.

Never materialized

[edit]- proposed Pan-American monetary union – abandoned in the form proposed by Argentina

- proposed monetary union between the United Kingdom and Norway using the pound sterling during the late 1940s and early 1950s

- proposed gold-backed, pan-African monetary union put forward by Muammar Gaddafi prior to his death

See also

[edit]References

[edit]- ^ "World Bank" (PDF). WorldBank.org. Retrieved 30 April 2019.

- ^ Hafner, Kurt A.; Jager, Jennifer. "The Optimum Currency Area Theory and the EMU". Intereconomics. Retrieved 1 April 2021.

- ^ Global Economy, The. "Currency unions, Monetary unions". The Global Economy. Naven Valev. Retrieved 1 April 2021.

- ^ "Study". Study.com. Retrieved 30 April 2019.

- ^ "Global Financial Integrity". gfintegrity.org. 20 June 2011. Retrieved 30 April 2019.

- ^ Enoch, Charles; Krueger, Russell. "Currency unions: key variables, definitions, measurement, and statistical improvement" (PDF). Bank for International Settlements. Retrieved 30 April 2019.

- ^ Bolton, Sally (10 December 2001). "History of currency unions". The Guardian. Retrieved 30 April 2019.

- ^ "History of Money in Malaysia: Colonial Notes & Coins". Bank Negara Malaysia. 2010. Archived from the original on 22 July 2011. Retrieved 5 July 2021.

- ^ Quah, C. H.; Ho, Y. J. (2020). "Economic Feasibility of Malaysia and Singapore-Brunei Monetary Reunion: A Scrutiny during Major Financial Crises". Applied Economics Journal. 27 (1): 23–51.

- ^ Anguilla and Montserrat are members of OECS currency union, but not of the CSME.

- ^ To all intents and purposes a monetary union. They are the last two nations whose dollars have remained at par and mutually interchangeable since the days when the Spanish Dollar was the united currency of large areas of the New World and Southeast Asia.

- ^ alongside the ngultrum

- ^ Not official, but freely used as a tender in Nepal, due to primarily the economic flux with India and also the instability caused by that country's civil war.

- ^ Zacharia, Janine (2010-05-31). "Palestinian officials think about replacing Israeli shekel with Palestine pound". The Washington Post and Times-Herald. ISSN 0190-8286. Retrieved 2018-08-22.

- ^ Cobham, David (2004-09-15). "Alternative currency arrangements for a new Palestinian state" (PDF). In David Cobham (ed.). The Economics of Palestine: Economic Policy and Institutional Reform for a Viable Palestine State. London: Routledge. ISBN 9780415327619. Retrieved 2018-08-22.

- ^ "Compact- Title 02 Article 05". www.fsmlaw.org.

- ^ "Zimbabwe abandons its currency". 2009-01-29. Retrieved 2019-10-15.

- ^ EU Overseas countries and some other territories participate partially in the EU single market per part four of the Treaty Establishing the European Community Archived 2013-11-16 at the Wayback Machine; Some EU Outermost regions and other territories use the Euro of the currency union, others are part of the customs union; some participate in both unions and some in neither.

Territories of the United States, Australian External Territories and Realm of New Zealand territories share the currency and mostly also the market of their respective mainland state, but are generally not part of its customs territory. - ^ "European Union". Europa.eu. Retrieved 30 April 2019.

- ^ Asongu, Simplice; Nwachukwu, Jacinta; Tchamyou, Vanessa (2016-08-01). "A Literature Survey on Proposed African Monetary Unions" (PDF). Journal of Economic Surveys. 31 (3): 878–902. doi:10.1111/joes.12174. ISSN 1467-6419. S2CID 38454408.

- ^ "Public Notice: Information About East Africa Currency Should Be Disregarded" (PDF) (Press release). Bank of Tanzania. 2024-03-04.

- ^ "A common currency at a later stage of Africa's economic integration". 30 November 2001.

- ^ "Brazil and Argentina to begin preparations for common currency, Financial Times reports". Reuters. 2023-01-22. Retrieved 2023-01-22.

- ^ a b Bolton, Sally (10 December 2001). "A history of currency unions". guardian.co.uk. Retrieved 26 February 2012.

France persuaded Belgium, Italy, Switzerland and Greece

- ^ Not currently on any political agenda, based mostly off conspiracy theories.

Further reading

[edit]- Acocella, N. and Di Bartolomeo, G. and Tirelli, P. [2007], ‘Monetary conservatism and fiscal coordination in a monetary union’, in: ‘Economics Letters’, 94(1): 56–63.

- Bergin, Paul (2008). "Monetary Union". In David R. Henderson (ed.). Concise Encyclopedia of Economics (2nd ed.). Indianapolis: Library of Economics and Liberty. ISBN 978-0865976658. OCLC 237794267.

External links

[edit]- West Africa opts for currency union

- Economist- Antipodean currencies (Australia and New Zealand)

- Reasons for the collapse of the Rouble Zone

- OECD Development Centre – the Rand Zone

| International | |

|---|---|

| National | |

| Other | |

Currency union

View on GrokipediaA currency union is an arrangement among two or more sovereign states to share a single currency and, typically, a common monetary policy managed by a supranational authority, thereby forgoing independent control over money supply and exchange rates to promote economic integration.[1] The concept draws from optimal currency area theory, pioneered by economist Robert Mundell, which argues that such unions succeed when members exhibit high labor mobility, substantial trade linkages, fiscal coordination, and symmetric economic shocks to minimize adjustment costs from asymmetric disturbances.[2] Prominent examples include the Eurozone, where 20 European Union countries adopted the euro as of 2023, facilitating seamless trade but exposing vulnerabilities during crises like the 2010s sovereign debt episode due to divergent national fiscal policies and limited risk-sharing mechanisms.[3] Other unions encompass the West African Economic and Monetary Union (UEMOA) and Central African Economic and Monetary Community (CEMAC), both utilizing the CFA franc tied to the euro, and the Eastern Caribbean Currency Union employing the East Caribbean dollar, which have sustained stability through pegs to major currencies despite varying growth trajectories among members.[4] Benefits such as eliminated exchange rate risks and lowered transaction costs empirically boost intra-union trade and investment, yet challenges persist from relinquished monetary sovereignty, amplifying the need for robust fiscal discipline and convergence criteria to avert imbalances, as observed in persistent divergences within these arrangements.[5][6]

Definition and Fundamentals

Core Definition and Requirements

A currency union is an arrangement in which two or more sovereign states or economies agree to share a single currency for domestic and international transactions, thereby eliminating exchange rate fluctuations among participants.[4][7] This shared currency replaces individual national currencies, requiring participants to relinquish control over their money supply and often their independent monetary policies.[8] Unlike fixed exchange rate pegs, which maintain separate currencies tied to a reference, a true currency union involves full adoption of the common medium of exchange, as seen in formal agreements like the Eurozone's use of the euro since January 1, 1999.[4] Core requirements for establishing and sustaining a currency union include the irrevocable adoption of the common currency by all members, typically facilitated through legal tender laws that mandate its exclusive use for settling debts and transactions within the union.[7] A supranational monetary authority, such as a shared central bank, is generally necessary to manage issuance, maintain stability, and conduct unified monetary policy, including setting interest rates and controlling inflation targets across the area.[8][3] Participants must also harmonize certain foreign exchange operations, pooling reserves or aligning interventions to defend the currency's external value.[7] However, fiscal policies often remain national, creating potential tensions without deeper integration, as evidenced by the European Central Bank's exclusive mandate for euro-area monetary policy since its inception in 1998, while national governments retain budget sovereignty under constraints like the Stability and Growth Pact's 3% GDP deficit limit introduced in 1997. In cases of unilateral currency adoption, such as Ecuador's dollarization on January 9, 2000, or Panama's longstanding use of the U.S. dollar since 1904, the union lacks a shared policy mechanism, with the issuing country (e.g., the U.S. Federal Reserve) unilaterally controlling the money supply, which can lead to adjustment challenges for adopters without representation in decision-making.[4][8] Empirical studies indicate that successful unions require sufficient economic symmetry to mitigate risks from asymmetric shocks, though formal criteria like convergence in inflation rates (e.g., within 1.5 percentage points as per the Maastricht Treaty's 1992 convergence criteria for euro entry) are often imposed ex ante but do not guarantee long-term viability.[9] Source credibility in academic literature on unions, such as works from the IMF, emphasizes data-driven assessments over ideological preferences, contrasting with some policy advocacy that overlooks fiscal divergences.[7]Distinctions from Related Concepts

A currency union involves sovereign states permanently adopting a single shared currency, typically managed by a supranational monetary authority, which eliminates national currencies and exchange rate adjustments between members. This contrasts with fixed exchange rate regimes, where countries retain their own currencies pegged to a reference currency or basket, preserving options for devaluation, revaluation, or abandonment of the peg under domestic control, albeit with credibility challenges and potential reserve losses.[10] In currency unions, seigniorage revenue from money creation is pooled or shared via the common central bank, whereas fixed pegs allow national authorities to retain such benefits, though they must maintain full convertibility backed by reserves.[11] Currency unions differ from unilateral currency substitution, such as dollarization, in their symmetry and institutional structure. Dollarization occurs when a country adopts a foreign currency like the U.S. dollar without the issuing country's consent or shared policy input, forfeiting seigniorage entirely and lacking representation in the foreign central bank, as seen in Ecuador's 2000 adoption of the dollar.[12][13] In contrast, formal currency unions like the Eurozone involve negotiated agreements among equals, with members holding stakes in a joint monetary authority such as the European Central Bank, enabling coordinated policy but requiring fiscal discipline to mitigate asymmetric shocks.[5] Currency boards, a harder unilateral peg variant, maintain a domestic currency fully backed by foreign reserves at a fixed rate but do not dissolve national monetary sovereignty to the same irrevocable degree.[14] Currency unions must be distinguished from customs unions, which focus on trade integration through elimination of internal tariffs and adoption of a common external tariff, without mandating monetary convergence or shared currencies.[15] For instance, the Southern Common Market (Mercosur) operates as a customs union among Brazil, Argentina, and others since 1991, yet members retain independent currencies and exchange rate policies, exposing them to competitive devaluations absent in currency unions.[16] Broader economic unions extend beyond currency sharing to include fiscal policy coordination, such as harmonized taxes or budgets, whereas currency unions prioritize monetary unification without necessarily imposing such fiscal transfers, as evidenced by the Eurozone's initial lack of a full fiscal union until post-2010 mechanisms like the European Stability Mechanism.[17][18] The term "monetary union" is often synonymous with currency union in emphasizing a single policy and currency area, though some contexts reserve it for arrangements with perfect currency substitutability via fixed but non-irrevocable rates.[1][7]Theoretical Foundations

Optimal Currency Area Theory

The Optimal Currency Area (OCA) theory posits that a group of economies forms an optimal currency area if the benefits of sharing a single currency outweigh the costs, particularly in terms of adjusting to economic shocks without the flexibility of independent exchange rates.[19] The theory emerged in the context of debates over fixed versus flexible exchange rates, emphasizing that currency domains should align with regions where internal adjustment mechanisms can effectively substitute for monetary policy autonomy.[20] Robert Mundell introduced the framework in his 1961 paper, arguing that balance-of-payments crises under fixed rates could be mitigated if areas sharing a currency possess sufficient factor mobility to reallocate resources across borders.[19] Mundell's primary criterion focuses on labor mobility: in an OCA, workers can relocate freely from regions facing unemployment due to asymmetric shocks—such as localized demand declines—to areas with labor shortages, thereby restoring equilibrium without nominal exchange rate adjustments.[21] [22] This assumes that barriers to migration, like cultural or linguistic differences, are minimal, allowing real wage flexibility and output stabilization. Subsequent contributions refined the model; Ronald McKinnon in 1963 highlighted openness to trade as a key factor, noting that smaller, highly integrated economies benefit from currency union to insulate against terms-of-trade volatility from independent monetary policies.[23] [24] Peter Kenen in 1969 added production diversification, positing that economies with similar output structures experience more symmetric shocks, reducing the need for exchange rate buffers and enhancing union stability.[24] [22] Additional criteria include fiscal integration for shock absorption via transfers and nominal rigidities that hinder price or wage adjustments.[25] Empirical assessments, such as those examining U.S. regions, find support for OCA conditions like interstate labor mobility and fiscal federalism, which have sustained the dollar union despite regional disparities.[26] However, applications to proposed unions like the Eurozone reveal challenges; pre-1999 analyses indicated insufficient symmetry in business cycles and limited labor mobility across member states, contributing to divergent responses during the 2008-2012 sovereign debt crisis where peripheral economies suffered prolonged adjustments without devaluation options.[27] [23] Critics argue the theory is static and overlooks endogeneity—integration may deepen post-union, fulfilling criteria retrospectively—and underemphasizes benefits like reduced transaction costs or financial market deepening.[28] [29] It also assumes shock symmetry can be reliably measured, yet evidence from global pegged regimes shows persistent vulnerabilities in diverse areas lacking robust institutions.[27] Overall, while OCA provides a benchmark for evaluating currency unions, its predictive power depends on verifiable fulfillment of criteria, as incomplete adherence has empirically amplified adjustment costs in real-world implementations.[30]Monetary and Fiscal Policy Dynamics

In currency unions, monetary policy is centralized under a supranational authority, such as a common central bank, which sets a uniform nominal interest rate and conducts operations to target union-wide price stability, forgoing national tailoring to idiosyncratic shocks.[31][32] This setup assumes symmetric business cycles or sufficient labor and goods market flexibility for adjustment, but deviations can amplify output volatility when fiscal responses lag.[33] Fiscal policy remains decentralized at the national level, allowing member states to set spending, taxation, and borrowing independently, yet without access to seigniorage or currency devaluation to finance deficits.[34] This creates incentives for fiscal restraint, as unsustainable national debts risk higher sovereign spreads and potential spillover to union-wide monetary credibility via fears of implicit bailouts or monetization.[35] Empirical evidence from the Eurozone post-2008 shows that decentralized fiscal decisions exacerbated sovereign debt pressures, with Greece's debt-to-GDP ratio exceeding 180% by 2011, prompting market-driven discipline absent automatic transfers.[33][34] The interaction generates moral hazard risks, where weaker fiscal performers may overborrow expecting solidarity from stronger members or central bank intervention, undermining the no-bailout clauses common in such arrangements.[35] To counter this, unions often impose rules like the EU's Stability and Growth Pact, capping structural deficits at 3% of GDP and debt at 60%, though enforcement has varied, with violations in seven Eurozone countries averaging 4.5% deficits during 2003–2007.[33] Without fiscal coordination or transfers—estimated at 10–30% of GDP shocks in full fiscal unions like the U.S.—asymmetric shocks propagate via trade and financial channels, heightening recession risks in divergent economies.[36] Optimal policy models suggest coupling conservative monetary stances with countercyclical national fiscal buffers, yet political fragmentation often delays implementation, as seen in delayed Eurozone fiscal compact ratification in 2012.[37][32]Economic Advantages

Trade and Efficiency Gains

Currency unions enhance trade volumes primarily by mitigating exchange rate volatility and associated risks, which otherwise deter cross-border transactions. Without the need for currency hedging or conversion, firms face lower uncertainty in pricing and profitability forecasts, fostering deeper economic integration. This mechanism aligns with first-principles expectations: stable nominal exchange rates reduce the effective cost of international trade, enabling smaller and more frequent shipments as well as simplified invoicing in a common unit. Empirical analyses substantiate these effects, with bilateral trade between union members typically increasing by 20-200% relative to pairs with independent currencies, depending on the estimation methodology and sample.[38][39][40] Transaction cost reductions provide a direct efficiency gain, as the elimination of foreign exchange fees—often 1-2% per transaction—compounds across supply chains and consumer markets. In the Eurozone, adoption of the euro in 1999 correlated with intra-union trade rising by approximately 5-15%, after controlling for prior European integration trends like the single market. This boost manifested in expanded export varieties and intensified competition, as evidenced by gravity model regressions on firm-level data from France and other members. Broader openness to global trade also improves, with currency union members exhibiting 10-30% higher overall trade-to-GDP ratios than comparable non-union economies.[41][42][43] Price transparency further amplifies these benefits, allowing consumers and producers to compare goods across borders without conversion distortions, which promotes arbitrage and curbs inflationary divergences. Studies on historical unions, such as the Latin Monetary Union in the 19th century, similarly document heightened commerce due to standardized pricing, though modern cases like the East Caribbean Currency Union show more modest gains in smaller economies owing to limited diversification. Heterogeneity persists: gains accrue disproportionately to differentiated goods sectors, while commodity exporters may see attenuated effects if global prices dominate. Overall, these dynamics yield microeconomic efficiencies, including streamlined payments systems and reduced inventory holdings for just-in-time trade.[44][45][46]Price Stability and Investment Effects

Currency unions typically achieve price stability through a centralized monetary authority that implements a uniform policy targeting low inflation across member states, often resulting in reduced volatility compared to independent national policies. In the Eurozone, the European Central Bank (ECB) has maintained an inflation target of 2% since refining its strategy in 2021, with harmonized index of consumer prices (HICP) averaging close to this level from the euro's introduction in 1999 through recent years, despite temporary surges. Empirical analyses indicate that monetary unions enhance stabilization by anchoring expectations and limiting high-inflation episodes more effectively than unilateral inflation-targeting regimes. For instance, studies of various unions show that shared currencies correlate with lower long-term inflation dispersion when fiscal discipline is enforced, though outcomes depend on institutional safeguards against fiscal dominance.[47][48][49] Persistent challenges arise from economic heterogeneity, where divergent productivity growth or demand pressures generate inflation differentials that a one-size-fits-all policy cannot fully address, potentially eroding real competitiveness in lagging members. In the Eurozone, unit labor cost divergences since 1999 have fueled such imbalances, with southern economies experiencing higher inflation relative to the core, complicating adjustment without exchange rate flexibility. These effects underscore that while unions promote average stability, they amplify risks from asymmetric shocks absent labor mobility or fiscal transfers, as evidenced by post-2008 divergences exceeding pre-union levels in some cases.[50][51] Regarding investment, the elimination of intra-union exchange rate risk and transaction costs in currency unions facilitates capital mobility, encouraging both foreign direct investment (FDI) and portfolio flows by lowering barriers to cross-border allocation. Empirical gravity models estimate that the euro increased inward FDI within the Eurozone by approximately 16%, with stronger effects for flows from non-members to adopters, driven by reduced hedging needs and enhanced market integration. Studies of the European Monetary Union (EMU) confirm positive impacts on U.S. FDI into euro-adopting countries, with inflows rising significantly post-1999, though benefits vary by recipient-country fundamentals like institutions and growth prospects. In broader samples, including developing unions like ECOWAS proposals, currency adoption correlates with higher FDI inflows, equivalent to 10-20% boosts in some regressions, contingent on credible policy frameworks. However, unions may deter investment in high-debt members during crises if perceived default risks rise without national monetary buffers, as seen in peripheral Eurozone economies during the sovereign debt episode.[52][53][54][55]Economic Disadvantages and Risks

Loss of Exchange Rate Flexibility

In a currency union, member states surrender independent control over their nominal exchange rates, eliminating a primary tool for addressing external imbalances and asymmetric economic shocks. This forfeiture means that countries cannot depreciate their currency to enhance export competitiveness or cushion against demand contractions, forcing reliance on internal adjustments such as wage reductions or fiscal austerity.[19] According to Robert Mundell's optimal currency area theory, flexible exchange rates enable depreciation to substitute for unemployment during localized downturns, particularly when labor mobility is low; in their absence, unions demand high economic integration to mitigate adjustment costs.[19][56] The rigidity amplifies vulnerabilities to divergent inflation rates, leading to persistent real exchange rate misalignments that erode competitiveness without nominal corrections. For instance, pre-crisis eurozone peripherals like Greece experienced cumulative inflation exceeding core members by over 30 percentage points from 2000 to 2009, fostering unit labor cost divergences of up to 30% relative to Germany and resulting in unsustainable current account deficits peaking at 15% of GDP in Greece by 2008.[57][58] Unable to devalue, affected economies resort to "internal devaluation," compressing domestic prices and wages, but nominal rigidities—such as downward wage stickiness—prolong recessions and elevate unemployment, as evidenced by Greece's GDP contraction of 25% from 2008 to 2013 alongside internal devaluation efforts yielding only partial realignment.[59][60] Empirical analyses of currency unions, including the euro, indicate that this constraint heightens crisis propagation risks, with output losses from shocks averaging 1-2% higher in inflexible regimes compared to flexible ones, absent fiscal transfers or integrated markets.[46] Critics argue that while unions promote nominal stability, the absence of exchange rate buffers undermines resilience in heterogeneous economies, as seen in the eurozone's 2010-2012 sovereign debt turmoil where peripherals' inability to adjust exchange rates intensified contagion and required external bailouts totaling over €240 billion for Greece alone by 2018.[59][60] Proponents of flexibility counter that it allows rapid rebalancing, though unions may compensate via deeper integration, a precondition often unmet in practice.[19]Asymmetric Shocks and Adjustment Costs

Asymmetric shocks, defined as economic disturbances with heterogeneous impacts across currency union members—such as idiosyncratic supply disruptions or demand shifts—undermine the efficacy of a uniform monetary policy, as the latter cannot optimally address divergent needs.[61] In optimal currency area frameworks, the degree of shock symmetry influences union viability; persistent asymmetries elevate adjustment burdens, particularly where pre-union exchange rate flexibility previously mitigated imbalances.[23] Empirical analyses of the Eurozone reveal that while business cycle correlations increased modestly prior to 1999, crisis-era shocks exposed underlying divergences, with peripheral economies suffering disproportionate hits from real estate collapses and credit contractions.[62] Without nominal exchange rate adjustments, equilibrium restoration relies on internal mechanisms: relative wage and price flexibility for competitiveness gains, labor mobility to reallocate resources, capital inflows for financing gaps, and fiscal transfers where available. However, these channels often entail high short-term costs due to nominal rigidities and institutional constraints; wage stickiness, for example, delays internal devaluation, prolonging output gaps.[63] In the Eurozone, labor mobility remains subdued—annual net migration rates between core and periphery averaged below 0.5% of population during 2000–2015—limiting automatic stabilization and amplifying regional unemployment persistence.[64] Internal devaluation, the primary competitiveness tool in such unions, involves aggressive wage and unit labor cost reductions but triggers demand contraction via debt-deflation dynamics and multiplier effects, yielding deeper recessions than external devaluation alternatives.[65] [66] During the 2009–2012 Eurozone crisis, Greece's response to asymmetric fiscal and competitiveness shocks included a 20–25% unit labor cost drop by 2015, yet this correlated with amplified GDP losses and unemployment surges exceeding 25%, as fiscal austerity compounded the adjustment.[67] [68] Risk-sharing via private capital flows proved volatile and procyclical, eroding during downturns, while the absence of a full fiscal union restricted automatic stabilizers to national levels, averaging under 30% of GDP shock absorption.[69] Quantified estimates underscore these costs: dynamic stochastic general equilibrium models indicate that asymmetric demand shocks in currency unions without fiscal coordination can double output volatility relative to flexible exchange regimes, with welfare losses from 1–3% of steady-state consumption depending on flexibility parameters.[70] In West African monetary unions, analogous supply asymmetries have similarly yielded adjustment lags, with output deviations persisting 2–3 years longer than in non-union peers.[71] Absent reforms enhancing labor markets or fiscal integration, such shocks foster divergence, as evidenced by persistent current account imbalances in the Eurozone post-2010.[72]Political and Institutional Dimensions

Sovereignty Trade-offs

In currency unions, member states forfeit national monetary sovereignty by delegating control over money supply, interest rates, and exchange rate policy to a supranational central bank, such as the European Central Bank (ECB) in the Eurozone, which prioritizes union-wide objectives like price stability over individual national needs.[73] This delegation eliminates the option for unilateral currency devaluation, a tool historically used to restore competitiveness during economic downturns or balance-of-payments crises, forcing reliance instead on internal adjustments like wage reductions and fiscal austerity, which can prolong recessions in divergent economies.[74] Empirical analyses indicate that while this setup fosters trade integration—evidenced by a 13-20% increase in bilateral trade volumes among union members—the loss of policy autonomy heightens vulnerability to asymmetric shocks, where region-specific disturbances cannot be addressed independently.[75] The Eurozone's sovereign debt crisis from 2009 to 2015 exemplifies these trade-offs, particularly in Greece, where adherence to the euro precluded devaluation despite a current account deficit exceeding 15% of GDP in 2008 and public debt surpassing 127% of GDP by 2009.[76] Unable to print money or adjust exchange rates, Greece endured enforced austerity under ECB and troika (ECB, IMF, European Commission) oversight, resulting in a 25% GDP contraction between 2008 and 2013 and unemployment peaking at 27.5% in 2013, as internal devaluation proved slower and more socially disruptive than external alternatives.[77] Political sovereignty was further eroded through bailout conditions that imposed supranational fiscal monitoring, including in 2015 when German Chancellor Angela Merkel conditioned aid on Greece surrendering budgetary autonomy to EU institutions, highlighting how larger members can impose preferences on smaller ones lacking veto power.[78] Critics, including post-Keynesian economists, argue this dynamic subordinates national democratic accountability to technocratic or creditor-driven decisions, amplifying risks of sovereign default without offsetting fiscal transfers.[79] Broader institutional implications include diminished capacity for tailored responses to domestic inflation differentials or capital flows; for instance, peripheral Eurozone countries experienced credit booms pre-2008 due to low ECB rates suited to core economies like Germany, exacerbating imbalances without national tools to counteract them.[80] In smaller unions like the West African Economic and Monetary Union (WAEMU), anchored to the euro via the CFA franc, members similarly cede seigniorage rights and maintain fixed pegs enforced by France until reforms in 2019-2020, trading sovereignty for stability amid volatile commodity exports but limiting countercyclical policies during shocks like the 2014-2016 oil price drop.[81] Proponents contend that pooled sovereignty enhances credibility and reduces inflationary biases inherent in national central banks, as evidenced by the ECB's average inflation rate of 1.8% from 1999-2022 versus higher volatility in pre-euro peripherals, yet this presumes symmetric interests and adequate convergence, conditions often unmet in heterogeneous unions.[74] Ultimately, these trade-offs demand robust governance to mitigate resentment, with empirical evidence suggesting unions endure longer when supplemented by fiscal unions or escape clauses, absent which sovereignty losses can fuel political backlash.[73]Governance Structures and Central Banking

In currency unions, governance structures revolve around a supranational central bank that conducts a single monetary policy for all member states, relinquishing national control over interest rates, money supply, and exchange rate adjustments. This central authority typically features a governing body comprising representatives from member countries' national central banks (NCBs) and an executive leadership appointed at the union level, designed to promote independence from short-term political pressures while pursuing shared objectives like price stability. Decision-making often employs one-member-one-vote principles or weighted voting to accommodate varying economic sizes, though simple majorities suffice for core policy choices.[82][83] The European Central Bank (ECB), established in 1998 as the cornerstone of the Eurozone's governance, exemplifies this model. Its Governing Council, responsible for monetary policy, includes the six-member Executive Board—appointed by the European Council for non-renewable eight-year terms—and the governors of the 20 euro-area NCBs, totaling 26 voters as of 2023. The ECB's primary mandate, enshrined in the Treaty on European Union, prioritizes maintaining price stability, defined as inflation below but close to 2% over the medium term, with secondary consideration for growth and employment only after price goals are met. To address the council's expansion, a 2022 review introduced a rotation system for voting rights among NCB governors, excluding the six largest economies to ensure smaller states retain influence without paralyzing decisions. National central banks retain operational roles in implementation but must align fully with ECB directives, highlighting a hybrid structure where NCBs integrate into the Eurosystem while preserving some autonomy in non-euro functions.[82][84][85] In the CFA franc zones, two parallel central banks manage distinct sub-unions pegged to the euro at a fixed rate of 655.957 CFA francs per euro, backed historically by French treasury guarantees until partial reforms in 2019-2020 shifted toward greater autonomy. The Central Bank of West African States (BCEAO), headquartered in Dakar, Senegal, serves eight West African members of the West African Economic and Monetary Union (UEMOA); its Board of Directors includes finance ministers and central bank governors from member states, with the governor elected by the board for a six-year term. Similarly, the Bank of Central African States (BEAC) governs six Central African states in the Economic and Monetary Community of Central Africa (CEMAC), with a comparable structure emphasizing regional coordination but retaining French observer status and convertibility assurances. These arrangements prioritize external stability over flexible domestic adjustment, limiting responses to asymmetric shocks through reserve pooling and fiscal discipline rules, such as BCEAO's prohibition on direct state financing beyond specified limits.[86][87][88] The Eastern Caribbean Central Bank (ECCB), operational since 1983 for eight member states, features a Monetary Council composed of finance ministers and central bank governors, which sets policy and appoints the ECCB governor for five-year terms, overseen by a Board of Directors including national representatives. This structure enforces a currency board-like peg to the U.S. dollar at 2.70 East Caribbean dollars per dollar, with monetary base fully backed by foreign reserves, constraining expansionary policy and emphasizing financial stability amid small, open economies vulnerable to tourism shocks.[89][90] Central banking in unions faces inherent tensions from asymmetric shocks, where divergent economic conditions—such as recessions in resource-dependent members versus booms in diversified ones—impede a uniform policy's efficacy, as national exchange rate devaluations are unavailable. Empirical analyses indicate that without robust fiscal transfers or labor mobility, unions rely on wage flexibility and structural reforms for adjustment, yet evidence from the Eurozone's 2009-2012 sovereign debt crisis shows persistent divergences, with peripheral states experiencing GDP drops up to 25% while core economies grew, underscoring governance limits absent deeper integration. Proponents argue independence enhances credibility and lowers borrowing costs—Eurozone sovereign yields averaged 1-2% premia pre-crisis versus higher in non-union peers—but critics, including IMF assessments, highlight risks of moral hazard from implicit bailouts, as seen in ECB's 2012 outright monetary transactions program stabilizing markets but fueling debates over fiscal-monetary blurring.[91][92][93]Convergence and Stability Mechanisms

Economic Convergence Criteria

Economic convergence criteria establish benchmarks for countries seeking to form or join a currency union, aiming to verify sufficient economic synchronization to mitigate risks from asymmetric shocks and divergent business cycles. These criteria draw from optimal currency area (OCA) theory, which posits that unions succeed when members exhibit high labor mobility, fiscal integration for transfers, and correlated output fluctuations, thereby facilitating adjustment without independent monetary tools.[23] In practice, formal criteria often prioritize nominal indicators—such as inflation and fiscal positions—over harder-to-quantify real factors like structural similarities, reflecting a compromise between theoretical ideals and political feasibility.[94] The most codified examples appear in the European Economic and Monetary Union (EMU), where the Maastricht Treaty of 1992 outlined four nominal convergence criteria for euro adoption, assessed biennially by the European Central Bank (ECB). Price stability requires the Harmonised Index of Consumer Prices (HICP) inflation rate to remain no more than 1.5 percentage points above the average of the three best-performing EU member states over the prior year.[95] Sustainable public finances mandate a government budget deficit not exceeding 3% of GDP and public debt not surpassing 60% of GDP, or demonstrating sufficient decline toward these thresholds if exceeded.[96] Convergence of long-term interest rates stipulates that rates on benchmark ten-year bonds must lie within 2 percentage points of the average in the three lowest-inflation states.[95] Exchange rate stability demands at least two years of participation in the Exchange Rate Mechanism II (ERM II) without severe tensions or unilateral devaluations.[96] Real convergence criteria, though less formalized, emphasize structural alignment to support OCA conditions, including synchronized GDP growth cycles, integrated labor markets, and similar productivity levels across members. Empirical assessments, such as correlation coefficients of output gaps, reveal that euro area countries exhibited moderate cyclical convergence pre-1999 but faced divergences post-2008 due to uneven shock impacts, underscoring the limitations of nominal benchmarks alone.[97] For instance, southern European states like Greece met nominal criteria in 2001 through statistical adjustments later deemed unsustainable, leading to fiscal imbalances that amplified crisis vulnerabilities without adequate real integration.[98] Other currency unions apply analogous standards with varying rigor; the Economic and Monetary Community of Central Africa (CEMAC) enforces fiscal convergence via ceilings on deficits (3% of GDP) and debt (70% of GDP), alongside inflation targets below 3%, to maintain peg stability to the euro.[99] These mechanisms aim to prevent moral hazard but often prove insufficient against endogenous divergences, where union membership itself alters incentives, such as reduced exchange rate discipline fostering fiscal laxity. Critics argue nominal criteria lack strong theoretical grounding for long-term viability, as they address symptoms rather than root causes like divergent competitiveness, evidenced by persistent euro area imbalances.[94] Effective enforcement requires credible institutions, yet lapses—such as delayed sanctions under the EU's Stability and Growth Pact—highlight implementation challenges.[98]Divergence Risks and Mitigation

Divergence risks in currency unions arise primarily from asymmetric economic shocks, where disturbances affect member economies unevenly, impeding adjustments that independent exchange rates would otherwise facilitate. Under optimal currency area theory, such divergences occur when business cycles are not synchronized, leading to mismatched monetary policy needs; for instance, a recession in one member may require expansionary policy, while another experiences overheating demanding tightening, resulting in suboptimal outcomes like elevated unemployment or inflationary pressures in affected regions.[23][21] These risks are exacerbated in unions lacking sufficient integration, as fixed exchange rates eliminate nominal adjustment mechanisms, forcing reliance on internal devaluation through wage and price reductions, which often prove slow and politically contentious.[100] Empirical evidence underscores these vulnerabilities, particularly in the Eurozone, where post-1999 adoption revealed widening macroeconomic divergences: GDP per capita gaps between core economies like Germany and periphery states such as Greece expanded, with the latter facing output drops exceeding 25% during the 2009-2012 sovereign debt crisis amid rigid labor markets and high public debt.[101] Inflation differentials persisted, with southern members averaging 2-3 percentage points above the Eurozone core in the mid-2000s, fueling current account imbalances that reached 15% of GDP in countries like Spain and Portugal by 2007.[102] Unit labor cost divergences further highlighted structural rigidities, as periphery competitiveness eroded without exchange rate corrections, contributing to prolonged stagnation in lagging areas.[103] Mitigation strategies emphasize building adjustment capacities absent exchange rate flexibility. Fiscal transfers, as seen in federal systems like the United States where interstate transfers absorb up to 10-30% of shocks, can redistribute resources to stabilize divergent regions, though Eurozone equivalents remain limited to ad hoc mechanisms like the European Stability Mechanism, activated post-2010 with €500 billion in lending capacity.[104] Enhancing labor mobility—evidenced by intra-Eurozone migration rates rising to 0.5% annually post-crisis—facilitates workforce reallocation, while structural reforms promoting wage flexibility and product market liberalization reduce adjustment lags, as demonstrated by Ireland's post-2008 recovery through labor market deregulation that halved unemployment from 15% to 6% by 2015.[105] Supranational fiscal rules, such as the Stability and Growth Pact's 3% deficit ceiling, aim to preempt divergences by enforcing discipline, though enforcement has been inconsistent, with violations in seven members exceeding limits in 2022.[106][107] Completing banking and capital market unions, as proposed in resilience-building analyses, would further mitigate risks by severing sovereign-bank loops and improving risk-sharing, potentially reducing output volatility by 20-30% based on simulations from integrated financial structures.[104][108]Historical Evolution

Early Historical Examples

The earliest modern currency unions emerged in 19th-century Europe amid efforts to facilitate trade and stabilize exchange rates through standardized coinage and metallic standards. These arrangements typically involved independent sovereign states adopting common monetary units and specifications without full political integration, often building on bimetallism or the gold standard.[109][110] The Latin Monetary Union (LMU), established by the Monetary Convention signed on December 23, 1865, in Paris, initially united France, Belgium, Italy, and Switzerland in a system of interchangeable silver and gold coins based on the 4.5-gram silver 5-franc piece and equivalent gold units, with a fixed bimetallic ratio of 15.5:1.[111] Greece acceded in 1867, while Spain, Romania, and others partially adopted the standards without full membership, minting coins at the union's specifications to circulate freely across borders.[112] The union aimed to counter the inefficiencies of diverse national coinages but faltered due to asymmetric silver overproduction and depreciation after 1873, prompting weaker members like Italy to mint excess silver coins—exploiting the fixed ratio under Gresham's law—resulting in net silver outflows from France and a suspension of unlimited coin acceptance by 1874.[113][114] Formal operations ceased during World War I, with the convention lapsing in 1927 after persistent deviations and national minting restrictions.[111] The Scandinavian Monetary Union (SMU), formalized by the Scandinavian Coin Convention on May 5, 1873, between Denmark and the Sweden-Norway union, with independent Norway joining in 1875, created a gold-based parity among the krone (Denmark and Norway) and krona (Sweden) at 0.403225 grams of fine gold per unit.[115] This arrangement enabled unrestricted circulation of gold coins and notes at fixed rates, supported by synchronized adherence to the gold standard, and promoted financial integration evident in reduced spreads on long-term bond yields between 1870 and 1913.[116] Unlike the LMU, the SMU endured external shocks relatively intact until World War I, when divergent suspensions of gold convertibility—Sweden maintaining it longer while Denmark and Norway devalued—eroded parity; Norway exited first in 1914, followed by de facto dissolution by 1920 amid inflation differentials exceeding 20% in some years.[117][118] Pre-19th-century precedents were rarer and less formalized, often tied to loose alliances or imperial systems rather than voluntary unions of sovereign states; for instance, Central European arrangements from the 14th to 16th centuries involved periodic alignments of silver coin standards among principalities, but lacked binding convertibility or central oversight.[119] These early experiments highlighted persistent challenges like asymmetric economic structures and external pressures, informing later unions' emphasis on convergence criteria.[120]20th and 21st Century Developments

The CFA franc zones, comprising two distinct monetary unions for former French colonies in Africa, were established on December 26, 1945, through a decree linking their currencies to the French franc at a fixed parity, originally as the Colonies Françaises d'Afrique franc to stabilize colonial economies amid postwar reconstruction.[121] The West African zone, governed by the Central Bank of West African States (BCEAO), initially included eight countries such as Senegal, Mali, and Côte d'Ivoire, while the Central African zone, under the Bank of Central African States (BEAC), covered six nations including Cameroon and Chad; both zones required members to pool 50% of foreign reserves with France until reforms in the 2010s reduced this to 20%.[122] These arrangements persisted post-independence in the 1960s, with a major devaluation of 50% against the French franc on January 12, 1994, to address chronic overvaluation and trade imbalances, though critics argue the fixed peg perpetuated dependency on French monetary policy.[123] In the Caribbean, the Eastern Caribbean Currency Union evolved from British colonial monetary boards, with the Eastern Caribbean Currency Authority formed in 1965 to issue a common currency for territories including Antigua, St. Kitts and Nevis, and Grenada, pegged to the British pound and later the U.S. dollar at 4.8:1.[124] This culminated in the establishment of the Eastern Caribbean Central Bank on October 1, 1983, serving eight member states and maintaining a currency board-like system with full foreign reserve backing for the Eastern Caribbean dollar (XCD), which has ensured low inflation averaging under 2% annually since inception but limited independent monetary responses to local shocks.[125] The European Monetary Union represented the era's most integrated currency union, advancing through the Maastricht Treaty signed on February 7, 1992, which set convergence criteria including inflation below 1.5% above the best-performing member, public debt under 60% of GDP, and fiscal deficits below 3%.[126] The euro launched as a virtual currency for electronic transactions on January 1, 1999, for 11 initial members, expanding to 12 with Greece's entry in 2001; physical notes and coins circulated from January 1, 2002, replacing national currencies and facilitating trade growth estimated at 5-15% in the union's early years.[127] Into the 21st century, the Eurozone grew to 20 members by 2023, incorporating countries like Croatia in 2023, but encountered severe tests during the 2009-2012 sovereign debt crisis, where Greece's debt-to-GDP ratio exceeded 170% by 2011, prompting bailouts totaling €289 billion from the European Stability Mechanism and IMF, conditional on austerity that deepened recessions in peripheral states.[126] Reforms included the European Central Bank's outright monetary transactions program announced in 2012, which stabilized bond yields without purchases, underscoring tensions between monetary unity and fiscal divergence absent deeper political integration.[128] Meanwhile, African unions like the CFA zones underwent partial reforms, such as the 2019 pledge to end the French reserve guarantee for West Africa, though implementation lagged, reflecting ongoing debates over sovereignty versus stability.[129]Existing Currency Unions

Eurozone

The Eurozone, formally known as the euro area, consists of European Union member states that have adopted the euro (€) as their official currency and delegated monetary policy to the European Central Bank (ECB).[130] As of October 2025, it includes 20 countries, representing approximately 350 million people and forming the second-largest economy globally by nominal GDP.[131] [132] The union's framework stems from the 1992 Maastricht Treaty, which outlined economic and monetary union (EMU) objectives, including convergence criteria on inflation, deficits, debt, and interest rates for entry.[133] The euro was launched electronically on January 1, 1999, for 11 initial members, with physical notes and coins entering circulation on January 1, 2002.[131] The ECB, established in 1998 and headquartered in Frankfurt, Germany, holds exclusive competence over monetary policy, aiming to maintain price stability with a target inflation rate below but close to 2% over the medium term. National central banks form the Eurosystem, implementing ECB decisions, while fiscal policy remains sovereign, subject to Stability and Growth Pact limits of 3% GDP deficits and 60% debt-to-GDP ratios—criteria often breached, contributing to imbalances. Membership requires EU states to join the Exchange Rate Mechanism II (ERM II) for at least two years before adoption, though enforcement has varied; Greece joined in 2001 amid later-disputed data compliance.[130]| Country | Adoption Date |

|---|---|

| Austria | 1999 |

| Belgium | 1999 |

| Cyprus | 2008 |

| Estonia | 2011 |

| Finland | 1999 |

| France | 1999 |

| Germany | 1999 |

| Greece | 2001 |

| Ireland | 1999 |

| Italy | 1999 |

| Latvia | 2014 |

| Lithuania | 2015 |

| Luxembourg | 1999 |

| Malta | 2008 |

| Netherlands | 1999 |

| Portugal | 1999 |

| Slovakia | 2009 |

| Slovenia | 2007 |

| Spain | 1999 |

| Croatia | 2023 |

Other Regional Unions

The West African Economic and Monetary Union (UEMOA), established in 1994, comprises eight member states—Benin, Burkina Faso, Côte d'Ivoire, Guinea-Bissau, Mali, Niger, Senegal, and Togo—that share the West African CFA franc (XOF) as their common currency.[121] The currency, issued by the Central Bank of West African States (BCEAO) headquartered in Dakar, Senegal, maintains a fixed peg to the euro at a rate of 1 euro = 655.957 XOF, backed by French treasury guarantees requiring member states to deposit 50% of foreign reserves with the French Treasury.[141] This arrangement, originating from the 1945 Bretton Woods era and reformed in 1994 to enhance regional integration, promotes monetary stability with low inflation averaging below 3% annually since inception, though critics argue the French oversight limits full sovereignty and exposes economies to external shocks without independent adjustment tools.[121] Similarly, the Economic and Monetary Community of Central Africa (CEMAC), formed in 1994 from earlier cooperation frameworks dating to 1964, includes six nations—Cameroon, Central African Republic, Chad, Republic of the Congo, Equatorial Guinea, and Gabon—using the Central African CFA franc (XAF), also pegged to the euro at the same rate and managed by the Bank of Central African States (BEAC) in Yaoundé, Cameroon.[141] Like UEMOA, it features French reserve pooling, fostering price stability with inflation under 2% in recent years, but facing challenges from oil dependency in several members, leading to fiscal divergences and occasional devaluation pressures, as seen in the 1994 CFA devaluation that halved the currency's value against the French franc to boost competitiveness. The Eastern Caribbean Currency Union (ECCU), operational since 1976 under the Eastern Caribbean Central Bank (ECCB) based in St. Kitts and Nevis, unites eight territories—Anguilla, Antigua and Barbuda, Dominica, Grenada, Montserrat, Saint Kitts and Nevis, Saint Lucia, and Saint Vincent and the Grenadines—with the East Caribbean dollar (XCD) fixed at 2.70 XCD per U.S. dollar.[124] Evolving from British colonial monetary boards established in the 1950s, the union emphasizes a currency board-like regime with full foreign reserve backing, achieving sustained low inflation around 2-3% and supporting tourism-driven growth, though vulnerability to natural disasters, such as Hurricanes Irma and Maria in 2017 which caused 5-10% GDP contractions in affected islands, highlights limited fiscal buffers without national currencies for devaluation.[142] The Common Monetary Area (CMA), formalized in 1986 succeeding the 1974 Rand Monetary Area, links South Africa with Lesotho, Namibia, and Eswatini, where the South African rand serves as legal tender or is pegged 1:1 by national currencies issued by respective central banks.[143] Governed by multilateral agreements ensuring free capital flows and rand convertibility, the arrangement has stabilized smaller economies with inflation convergence—Lesotho's averaging 5.5% from 2000-2020 aligning closer to South Africa's 5.2%—but exposes them to asymmetric shocks, such as South Africa's 2008-2009 recession transmitting contractions of up to 4% GDP to Lesotho via trade and remittances comprising 40% of its economy.[144]Former and Proposed Currency Unions

Disbanded Unions

The Latin Monetary Union, established on December 23, 1865, by France, Belgium, Italy, and Switzerland, aimed to standardize silver and gold coinage at fixed weights to promote trade across borders.[113] Greece joined in 1867, followed by Romania and others as associates, but persistent overissuance of silver coins—exceeding agreed quotas—eroded trust and triggered liquidity crises in 1873 and 1885, as weaker members like Italy and Greece minted excess currency that circulated as legal tender elsewhere.[145][146] The shift to the gold standard and divergent national policies further strained the arrangement, with France demonetizing excess silver in 1876.[147] World War I in 1914 prompted the suspension of gold convertibility across members, effectively halting operations, though the union lingered legally until Belgium's formal exit announcement in 1925 led to its dissolution on January 1, 1927.[113][147][148] The Scandinavian Monetary Union, formed between 1873 and 1875 by Denmark, Sweden, and Norway, created a common unit of account—the krone or krona—pegged to gold at 1,503 milligrams of fine gold, with mutual acceptance of national coins at par to facilitate Nordic trade.[109][149] The union endured initial shocks like the Long Depression but unraveled amid World War I, as neutral members suspended gold convertibility in 1914–1916 and adopted divergent exchange policies: Sweden prioritized gold resumption earlier, while Norway and Denmark faced inflation pressures from wartime imports.[150][118] Trade imbalances and national banknote preferences eroded par exchange by 1917, leading to de facto dissolution; formal cancellation occurred in 1924 after failed interwar revival attempts.[117][151] Other notable disbandments include the Austro-German Monetary Union of 1857, which unified Austrian and Prussian silver standards but dissolved in 1866 following Austria's defeat in the Austro-Prussian War, as political rivalry precluded sustained alignment.[110] Post-World War II cases often stemmed from decolonization or state breakups, such as the 1967 separation of Singapore from the Malaysian ringgit, where economic divergences and political tensions prompted Singapore to issue its own dollar despite initial common usage.[152] Empirical patterns across dissolutions highlight causal factors like asymmetric inflation (e.g., exceeding 10–20% differentials annually), collapsing bilateral trade volumes (often halving pre-exit), and sovereignty shifts, such as independence or war, overriding shared currency benefits.[153] These failures underscore that absent fiscal transfers or political union, monetary integration proves fragile when output shocks diverge, as seen in the classical cases where gold standard adherence amplified rather than mitigated national policy conflicts.[154]Ongoing Proposals and Challenges

The Economic Community of West African States (ECOWAS) aims to introduce the Eco as a single currency by July 2027, extending beyond the existing West African Economic and Monetary Union (WAEMU) to encompass all 15 member states and replace the CFA franc in WAEMU countries.[155] This initiative, approved by ECOWAS leaders in June 2019, seeks to foster trade integration and reduce reliance on external currencies, but it has encountered multiple postponements since the original 2000 target under the West African Monetary Zone framework.[156] As of September 2025, only four WAEMU countries met the convergence criteria for inflation and fiscal deficits in 2024, highlighting persistent divergences in economic performance.[157] Political fragmentation exacerbates these economic issues, with military coups in Mali, Burkina Faso, and Niger since 2020 prompting those nations to form the Alliance of Sahel States and threaten ECOWAS exit, which could undermine the union's viability given their combined population of over 70 million.[157] External factors, including France's historical role in anchoring the CFA franc to the euro, have fueled debates over monetary sovereignty, though WAEMU's fixed peg has provided stability amid regional volatility.[158] Empirical analyses of prior African monetary integrations, such as the rand zone's dissolution in the 1960s due to asymmetric shocks from commodity dependence, underscore risks of output divergence without robust fiscal mechanisms.[159] In the Gulf Cooperation Council (GCC), efforts toward a unified currency persist, with member states—Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates—advancing policy alignments on fiscal and monetary indicators as of March 2025.[160] Originally slated for 2010, the project stalled amid the 2008 financial crisis and divergences in oil revenue management, yet recent hydrocarbon price recoveries have renewed momentum through synchronized interest rate adjustments pegged to the U.S. dollar. Challenges include varying non-oil sector developments and fiscal vulnerabilities, as evidenced by Saudi Arabia's Vision 2030 diversification contrasting with smaller members' heavier hydrocarbon reliance, potentially amplifying asymmetric shocks absent a central fiscal authority.[161] BRICS nations (Brazil, Russia, India, China, South Africa, plus recent expandees) have discussed de-dollarization mechanisms, including a blockchain-based payment system announced in 2025, but no formal common currency proposal has progressed beyond conceptual stages.[162] Internal divergences—such as India's reluctance amid U.S. trade ties and China's yuan internationalization push—have redirected focus to bilateral local-currency settlements, which grew to 28% of intra-BRICS trade by 2024 but fall short of union-level integration.[163] Studies on prospective unions reveal that heterogeneous trade structures and policy autonomy losses, as modeled in dynamic panel analyses, often yield limited trade gains without prior business cycle synchronization, with BRICS GDP correlations averaging below 0.4 during 2010–2020.[164] Overall, proposed unions confront empirical hurdles like inadequate labor mobility and fiscal spillovers, where simulations indicate trade boosts of 10–20% but heightened recession risks in non-core members without convergence.[165]Empirical Evidence and Case Studies

Success Metrics and Failures