Community hub

Recent from talks

Contribute something

Nothing was collected or created yet.

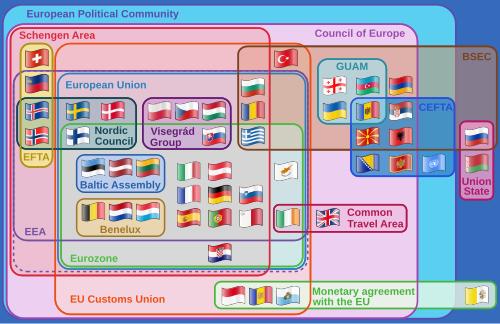

Eurozone

View on Wikipedia

| Policy of | European Union |

|---|---|

| Type | Monetary union |

| Currency | Euro |

| Established | 1 January 1999 |

| Member states | |

| Governance | |

| Monetary authority | Eurosystem |

| Political oversight | Eurogroup |

| Statistics | |

| Area | 2,801,552 km2 (1,081,685 sq mi)[1] |

| Population | 351,379,988 (1 January 2025)[2] |

| Density | 125/km2 (323.7/sq mi) |

| GDP (nominal) | €14.372 trillion €40,990 (per capita) (2023)[3] |

| Interest rate | 2.5%[4] |

| Inflation | 2.4% (February 2025)[5] |

| Unemployment | 6.2% (January 2025)[6] |

| Trade balance | €310 billion trade surplus[7] |

The euro area,[8] commonly called the eurozone (EZ), is a currency union of 20 member states of the European Union (EU) that have adopted the euro (€) as their primary currency and sole legal tender, and have thus fully implemented Economic and Monetary Union policies.

The 20 eurozone members are: Austria, Belgium, Croatia, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia, and Spain.

The largest economies in the eurozone are France and Germany, whose combined economic output accounts for almost half of the zone’s total.[9] A number of non-EU member states, namely Andorra, Monaco, San Marino, and Vatican City have formal agreements with the EU to use the euro as their official currency and issue their own coins.[10][11][12] In addition, Kosovo and Montenegro have adopted the euro unilaterally, relying on euros already in circulation rather than minting currencies of their own.[13] These six countries, however, have no representation in any eurozone institution.[14]

The Eurosystem is the monetary authority of the eurozone, the Eurogroup is an informal body of finance ministers that makes fiscal policy for the currency union, and the European System of Central Banks is responsible for fiscal and monetary cooperation between eurozone and non-eurozone EU members. The European Central Bank (ECB) makes monetary policy for the eurozone, sets its base interest rate, and issues euro banknotes and coins. Since the 2008 financial crisis, the eurozone has established and used provisions for granting emergency loans to member states in return for enacting economic reforms.[15] The eurozone has also enacted some limited fiscal integration; for example, in peer review of each other's national budgets. The issue is political and in a state of flux in terms of what further provisions will be agreed for eurozone change.

The eurozone comprises about half the countries in geographical Europe.[16] Within the European Union (EU), seven member states have not yet adopted the euro and continue to use their own national currencies: Bulgaria, the Czech Republic, Denmark, Hungary, Poland, Romania, and Sweden. Of these, all except Denmark are legally committed to adopting the euro once they meet the required convergence criteria.[17] Bulgaria has been approved to become the 21st eurozone member effective 1 January 2026.[18] To date, no country has left the eurozone, and there are no formal provisions for either voluntary withdrawal or expulsion.[19]

Territory

[edit]Eurozone

[edit]

In 1998, eleven member states of the European Union had met the euro convergence criteria, and the eurozone came into existence with the official launch of the euro (alongside national currencies) on 1 January 1999 in those countries: Austria, Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal, and Spain. Greece qualified in 2000 and was admitted on 1 January 2001.[citation needed]

These twelve founding members introduced physical euro banknotes and euro coins on 1 January 2002. After a short transition period, they took out of circulation and rendered invalid their pre-euro national coins and notes.[citation needed]

Between 2007 and 2023, eight new states have acceded: Croatia, Cyprus, Estonia, Latvia, Lithuania, Malta, Slovakia, and Slovenia. Bulgaria has been approved to accede effective 1 January 2026.

| State | ISO code | Adopted on 1 Jan of |

Population in 2024[20] |

Nominal GNI in 2023 | Pre-euro currency |

Conversion rate of euro to pre-euro currency[21] |

Pre-euro currency was also used in |

Territories where euro is not used | ||

|---|---|---|---|---|---|---|---|---|---|---|

| (USD millions)[22] | As fraction of eurozone total |

Per capita in 2023 in USD | ||||||||

| AT | 1999[23] | 9,158,750 | 502,500 | 3.24% | 55,030 | schilling | 13.7603 | |||

| BE | 1999[23] | 11,832,049 | 643,394 | 4.15% | 54,580 | franc | 40.3399 | Luxembourg | ||

| HR | 2023[24] | 3,861,967 | 79,478 | 0.51% | 20,590 | kuna | 7.53450 | |||

| CY | 2008[25] | 933,505 | 30,557 | 0.20% | 32,960 | pound | 0.585274 | Northern Cyprus[a] | ||

| EE | 2011[26] | 1,374,687 | 37,843 | 0.24% | 27,620 | kroon | 15.6466 | |||

| FI | 1999[23] | 5,603,851 | 297,225 | 1.92% | 53,230 | markka | 5.94573 | |||

| FR | 1999[23] | 68,401,997 | 3,085,396 | 19.92% | 45,180 | franc | 6.55957 | Andorra Monaco |

New Caledonia[b] French Polynesia[b] Wallis and Futuna[b] | |

| DE | 1999[23] | 83,445,000 | 4,563,533 | 29.46% | 54,800 | Mark | 1.95583 | Kosovo Montenegro |

||

| GR[c] | 2001[27] | 10,397,193 | 235,041 | 1.52% | 22,590 | drachma | 340.750 | |||

| IE | 1999[23] | 5,343,805 | 419,126 | 2.71% | 78,970 | pound | 0.787564 | |||

| IT | 1999[23] | 58,989,749 | 2,237,146 | 14.44% | 37,920 | lira | 1936.27 | San Marino Vatican City |

||

| LV | 2014[28] | 1,871,882 | 42,484 | 0.27% | 22,630 | lats | 0.702804 | |||

| LT | 2015[29] | 2,885,891 | 72,021 | 0.46% | 25,080 | litas | 3.45280 | |||

| LU | 1999[23] | 672,050 | 55,965 | 0.36% | 83,980 | franc | 40.3399 | Belgium | ||

| MT | 2008[30] | 563,443 | 19,208 | 0.12% | 34,750 | lira | 0.429300 | |||

| NL | 1999[23] | 17,942,942 | 1,118,008 | 7.22% | 62,540 | guilder | 2.20371 | Aruba[d] Curaçao[e] Sint Maarten[e] Caribbean Netherlands[f] | ||

| PT | 1999[23] | 10,639,726 | 276,643 | 1.79% | 26,150 | escudo | 200.482 | |||

| SK | 2009[31] | 5,459,781 | 123,670 | 0.80% | 22,790 | koruna | 30.1260 | |||

| SI | 2007[32] | 2,123,949 | 65,430 | 0.42% | 30,860 | tolar | 239.640 | |||

| ES | 1999[23] | 48,610,458 | 1,587,224 | 10.25% | 32,830 | peseta | 166.386 | Andorra | ||

| Eurozone total | EZ[g] | — | 350,077,581 | 15,491,903 | 100.00% | 44,304 | — | — | — | See above |

Dependent territories of EU member states not part of the EU

[edit]Three French dependent territories that are not part of the EU have adopted the euro, with France ensuring eurozone laws are implemented:

- Territorial collectivity of Saint Barthélemy

- Overseas Collectivity of Saint-Pierre and Miquelon

- French Southern and Antarctic Lands

Non-member usage

[edit]

- European Union member states (special territories not shown)

- 20 in the eurozone1 acceding member, effective 1 January 2026 (Bulgaria)5 not in ERM II, but committed to join the eurozone on meeting the convergence criteria (Czech Republic, Hungary, Poland, Romania, and Sweden)

- Non–EU member states

With formal agreement

[edit]The euro is also used in countries outside the EU. Four states (Andorra, Monaco, San Marino, and Vatican City) have signed formal agreements with the EU to use the euro and issue their own coins.[33][34] Nevertheless, they are not considered part of the eurozone by the ECB and do not have a seat in the ECB or Euro Group.

Akrotiri and Dhekelia (located on the island of Cyprus) belong to the United Kingdom, but there are agreements between the United Kingdom and Cyprus[citation needed] and between United Kingdom and EU[citation needed] about their partial integration with Cyprus and partial adoption of Cypriot law, including the usage of euro in Akrotiri and Dhekelia.[citation needed]

Several currencies are pegged to the euro, some of them with a fluctuation band and others with an exact rate. The Bosnia and Herzegovina convertible mark was once pegged to the Deutsche mark at par, and continues to be pegged to the euro today at the Deutsche mark's old rate (1.95583 per euro). The Bulgarian lev was initially pegged to the Deutsche Mark at a rate of BGL 1000 to DEM 1 in 1997, and has been pegged at a rate of BGN 1.95583 to EUR 1 since the introduction of the euro and the redenomination of the lev in 1999. The West African and Central African CFA francs are pegged exactly at 655.957 CFA to 1 EUR. In 1998, in anticipation of Economic and Monetary Union of the European Union, the Council of the European Union addressed the monetary agreements France had with the CFA Zone and Comoros, and ruled that the ECB had no obligation towards the convertibility of the CFA and Comorian francs. The responsibility of the free convertibility remained in the French Treasury.

Without formal agreement

[edit]Kosovo and Montenegro unilaterally adopted the euro as their sole currency without an agreement and, therefore, have no issuing rights.[34] These states are not considered part of the eurozone by the ECB. However, sometimes the term eurozone is applied to all territories that have adopted the euro as their sole currency.[35][36][37] Further unilateral adoption of the euro (euroisation), by both non-euro EU and non-EU members, is opposed by the ECB and EU.[38]

Historical eurozone enlargements and exchange-rate regimes for EU members

[edit]The chart below provides a full summary of all applying exchange-rate regimes for EU members, since the birth, on 13 March 1979, of the European Monetary System with its Exchange Rate Mechanism and the related new common currency ECU. On 1 January 1999, the euro replaced the ECU 1:1 at the exchange rate markets. During 1979–1999, the Deutsche Mark functioned as a de facto anchor for the ECU, meaning there was only a minor difference between pegging a currency against the ECU and pegging it against the Deutsche Mark.

Sources: EC convergence reports 1996-2014, Italian lira, Spanish peseta, Portuguese escudo, Finnish markka, Greek drachma, Sterling

The eurozone was established with its first 11 member states on 1 January 1999. The first enlargement of the eurozone, to Greece, took place on 1 January 2001, one year before the euro physically entered into circulation. The next enlargements were to states which joined the EU in 2004, and then joined the eurozone on 1 January of the year noted: Slovenia in 2007, Cyprus in 2008, Malta in 2008, Slovakia in 2009, Estonia in 2011, Latvia in 2014, and Lithuania in 2015. Croatia, which acceded to the EU in 2013, adopted the euro in 2023.

All new EU members joining the bloc after the signing of the Maastricht Treaty in 1992 committed to adopt the euro under the terms of their accession treaties once they comply with the five economic convergence criteria. The last of these is the exchange rate stability criterion, which requires having been an ERM-member for a minimum of two years without the presence of "severe tensions" for the currency exchange rate.

In September 2011, a diplomatic source close to the euro adoption preparation talks with the seven remaining new member states who had yet to adopt the euro at that time (Bulgaria, the Czech Republic, Hungary, Latvia, Lithuania, Poland, and Romania), claimed that the monetary union (eurozone) they had thought they were going to join upon their signing of the accession treaty may very well end up being a very different union, entailing a much closer fiscal, economic, and political convergence than originally anticipated. This changed legal status of the eurozone could potentially cause them to conclude that the conditions for their promise to join were no longer valid, which "could force them to stage new referendums" on euro adoption.[39]

Future enlargement

[edit]

Seven countries (Bulgaria, the Czech Republic, Denmark, Hungary, Poland, Romania, and Sweden) are EU members but do not use the euro. Bulgaria has been approved to adopt the single currency effective 1 January 2026.

Before joining the eurozone, a state must spend at least two years in the European Exchange Rate Mechanism (ERM II). As of January 2023, the central bank of Denmark and the Bulgarian central bank participate in ERM II.

Denmark obtained a special opt-out in the Maastricht Treaty, and thus is legally exempt from joining the eurozone unless its government decides otherwise, either by parliamentary vote or referendum. The United Kingdom likewise had an opt-out prior to withdrawing from the EU in 2020.

The remaining six countries have committed to adopt the euro in future, once they meet the convergence criteria. They should join as soon as they do so, which include being part of ERM II for two years. Sweden, which joined the EU in 1995 after the Maastricht Treaty was signed, rejected euro adoption in a 2003 referendum and since then the country has intentionally avoided fulfilling the adoption requirements by not joining ERM II, which is voluntary.[40][41] Bulgaria joined ERM II on 10 July 2020.[42]

Interest in joining the eurozone increased in Denmark, and initially in Poland, as a result of the 2008 financial crisis. In Iceland, there was an increase in interest in joining the European Union, a pre-condition for adopting the euro.[43] However, by 2010 the debt crisis in the eurozone caused interest from Poland, as well as the Czech Republic, Denmark and Sweden to cool.[44]

On 4 June 2025, the European Commission announced Bulgaria's compliance with the convergence criteria to adopt the euro on 1 January 2026.[45] In the context of Bulgaria's adoption of the euro, the Polish government under Donald Tusk has expressed a lack of economic readiness to join, whereas the newly elected Polish president Karol Nawrocki said that he is explicitly against Poland's future adoption of the euro.[46]

On 8 July 2025, the European Parliament endorsed Bulgaria's entry in the Eurozone[47] and the Council of the European Union adopted the final 3 legislative acts required for the admission.[48]

Expulsion and withdrawal

[edit]In the opinion of journalist Leigh Phillips and Locke Lord's Charles Proctor,[49][50] there is no provision in any European Union treaty for an exit from the eurozone. In fact, they argued, the Treaties make it clear that the process of monetary union was intended to be "irreversible" and "irrevocable".[50] However, in 2009, a European Central Bank legal study argued that, while voluntary withdrawal is legally not possible, expulsion remains "conceivable".[51] Although an explicit provision for an exit option does not exist, many experts and politicians in Europe have suggested an option to leave the eurozone should be included in the relevant treaties.[52]

On the issue of leaving the eurozone, the European Commission has stated that "[t]he irrevocability of membership in the euro area is an integral part of the Treaty framework and the Commission, as a guardian of the EU Treaties, intends to fully respect [that irrevocability]."[53] It added that it "does not intend to propose [any] amendment" to the relevant Treaties, the current status being "the best way going forward to increase the resilience of euro area Member States to potential economic and financial crises."[53] The European Central Bank, responding to a question by a Member of the European Parliament, has stated that an exit is not allowed under the Treaties.[54]

Likewise there is no provision for a state to be expelled from the euro.[55] Some, however, including the Dutch government, favour the creation of an expulsion provision for the case whereby a heavily indebted state in the eurozone refuses to comply with an EU economic reform policy.[56]

In a Texas law journal, University of Texas at Austin law professor Jens Dammann has argued that even now EU law contains an implicit right for member states to leave the eurozone if they no longer meet the criteria that they had to meet in order to join it.[57] Furthermore, he has suggested that, under narrow circumstances, the European Union can expel member states from the eurozone.[58]

Administration and representation

[edit]

The monetary policy of all countries in the eurozone is managed by the European Central Bank (ECB) and the Eurosystem which comprises the ECB and the central banks of the EU states who have joined the eurozone. Countries outside the eurozone are not represented in these institutions. Whereas all EU member states are part of the European System of Central Banks (ESCB), non EU member states have no say in all three institutions, even those with monetary agreements such as Monaco. The ECB is entitled to authorise the design and printing of euro banknotes and the volume of euro coins minted, and its president is currently Christine Lagarde.

The eurozone is represented politically by its finance ministers, known collectively as the Eurogroup, and is presided over by a president, currently Paschal Donohoe. The finance ministers of the EU member states that use the euro meet a day before a meeting of the Economic and Financial Affairs Council (Ecofin) of the Council of the European Union. The Group is not an official Council formation but when the full EcoFin council votes on matters only affecting the eurozone, only Euro Group members are permitted to vote on it.[59][60][61]

Since the 2008 financial crisis, the Euro Group has met irregularly not as finance ministers, but as heads of state and government (like the European Council). It is in this forum, the Euro summit, that many eurozone reforms have been decided upon. In 2011, former French President Nicolas Sarkozy pushed for these summits to become regular and twice a year in order for it to be a 'true economic government'.[62]

Reform

[edit]In April 2008 in Brussels, future European Commission President Jean-Claude Juncker suggested that the eurozone should be represented at the IMF as a bloc, rather than each member state separately: "It is absurd for those 15 countries not to agree to have a single representation at the IMF. It makes us look absolutely ridiculous. We are regarded as buffoons on the international scene".[63] In 2017 Juncker stated that he aims to have this agreed by the end of his mandate in 2019.[64] However, Finance Commissioner Joaquín Almunia stated that before there is common representation, a common political agenda should be agreed upon.[63]

Leading EU figures including the commission and national governments have proposed a variety of reforms to the eurozone's architecture; notably the creation of a Finance Minister, a larger eurozone budget, and reform of the current bailout mechanisms into either a "European Monetary Fund" or a eurozone Treasury. While many have similar themes, details vary greatly.[65][66][67][68]

Economy

[edit]

Comparison table

[edit]| Population (2023) | GDP (Local currency) (2023) | GDP (US$) (2023) | |

|---|---|---|---|

| 1410 million | CNY 126.1 trillion | US$17.7 trillion | |

| 349 million | EUR 14.4 trillion | US$15.6 trillion | |

| 335 million | USD 26.9 trillion | US$26.9 trillion |

| Economy | Nominal GDP (billions in USD) – Peak year as of 2020

| ||||||||

|---|---|---|---|---|---|---|---|---|---|

| (01) United States (Peak in 2019) | |||||||||

| (02) China (Peak in 2020) | |||||||||

| (03) |

|||||||||

| (04) Japan (Peak in 2012) | |||||||||

| (05) United Kingdom (Peak in 2007) | |||||||||

| (06) India (Peak in 2019) | |||||||||

| (07) Brazil (Peak in 2011) | |||||||||

| (08) Russia (Peak in 2013) | |||||||||

| (09) Canada (Peak in 2013) | |||||||||

| (10) Korea (Peak in 2018) | |||||||||

| (11) Australia (Peak in 2012) | |||||||||

| (12) Mexico (Peak in 2014) | |||||||||

| (13) Indonesia (Peak in 2019) | |||||||||

| (14) Turkey (Peak in 2013) | |||||||||

| (15) Saudi Arabia (Peak in 2018) | |||||||||

| (16) Switzerland (Peak in 2019) | |||||||||

| (17) Argentina (Peak in 2017) | |||||||||

| (18) Taiwan (Peak in 2020) | |||||||||

| (19) Poland (Peak in 2018) | |||||||||

| (20) Sweden (Peak in 2013) | |||||||||

|

The 20 largest economies in the world including eurozone as a single entity, by nominal GDP (2020) at their peak level of GDP in billions US$. The values for EU members that are not also eurozone members are listed both separately and as part of the EU.[70] | |||||||||

Inflation

[edit]HICP figures from the ECB, overall index:[71]

|

|

|

|

|

Interest rates

[edit]Interest rates for the eurozone, set by the ECB since 1999.[72] Levels are in percentages per annum. Between June 2000 and October 2008, the main refinancing operations were variable rate tenders, as opposed to fixed rate tenders. The figures indicated in the table from 2000 to 2008 refer to the minimum interest rate at which counterparties may place their bids.[73]

Public debt

[edit]The following table states the ratio of public debt to GDP in percent for eurozone countries given by EuroStat.[74] The euro convergence criterion is to not exceed 60%.

| Country | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022[75] | 2023[76] | 2024[77] |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Eurozone | 64.9 | 69.6 | 80.2 | 85.7 | 87.6 | 91.0 | 93.0 | 93.1 | 91.2 | 90.4 | 87.9 | 85.8 | 83.8 | 97.2 | 95.6 | 94.2 | 89.9 | 87.4 |

| Austria | 64.7 | 68.7 | 79.7 | 82.7 | 82.4 | 81.9 | 81.3 | 84.0 | 84.9 | 82.8 | 78.5 | 74.1 | 70.6 | 83.3 | 82.8 | 82.7 | 78.2 | 81.8 |

| Belgium | 87.0 | 93.2 | 99.6 | 100.3 | 103.5 | 104.8 | 105.5 | 107.0 | 105.2 | 105.0 | 102.0 | 99.8 | 97.7 | 112.8 | 108.2 | 108.3 | 108.0 | 104.7 |

| Cyprus | 53.5 | 45.5 | 53.9 | 56.3 | 65.8 | 80.3 | 104.0 | 109.1 | 108.9 | 107.1 | 97.5 | 100.6 | 91.1 | 115.0 | 103.6 | 95.2 | 79.4 | 65.0 |

| Croatia | 37.2 | 39.1 | 48.4 | 57.3 | 63.7 | 69.4 | 80.3 | 83.9 | 83.3 | 79.8 | 76.7 | 73.3 | 71.1 | 87.3 | 79.8 | 74.3 | 64.4 | 57.6 |

| Estonia | 3.7 | 4.5 | 7.0 | 6.6 | 5.9 | 9.8 | 10.2 | 10.6 | 9.7 | 9.4 | 9.0 | 8.4 | 8.6 | 19.0 | 18.1 | 16.7 | 18.2 | 23.6 |

| Finland | 34.0 | 32.6 | 41.7 | 47.1 | 48.5 | 53.6 | 56.2 | 59.8 | 63.1 | 63.1 | 61.4 | 59.0 | 59.5 | 69.0 | 65.8 | 72.1 | 73.8 | 82.1 |

| France | 64.3 | 68.8 | 79.0 | 81.7 | 85.2 | 90.6 | 93.4 | 94.9 | 95.8 | 96.5 | 97.0 | 98.4 | 97.5 | 114.6 | 112.9 | 113.1 | 111.9 | 113.0 |

| Germany | 63.7 | 65.5 | 72.4 | 81.0 | 78.3 | 81.1 | 78.7 | 75.6 | 71.2 | 68.1 | 64.1 | 61.9 | 58.9 | 68.7 | 69.3 | 67.2 | 64.8 | 62.5 |

| Greece | 103.1 | 109.4 | 126.7 | 146.2 | 172.1 | 161.9 | 178.4 | 180.2 | 176.9 | 180.8 | 178.6 | 181.2 | 180.7 | 206.3 | 193.3 | 182.1 | 165.5 | 153.6 |

| Ireland | 23.9 | 42.4 | 61.8 | 86.8 | 109.1 | 119.9 | 119.9 | 104.2 | 93.8 | 72.8 | 68.0 | 63.6 | 57.2 | 58.4 | 56.0 | 51.4 | 43.6 | 40.9 |

| Italy | 99.8 | 106.2 | 112.5 | 115.4 | 116.5 | 126.5 | 132.5 | 135.4 | 132.7 | 132.0 | 131.8 | 134.8 | 134.3 | 155.3 | 150.8 | 150.2 | 140.6 | 135.3 |

| Latvia | 8.0 | 18.6 | 36.6 | 47.5 | 42.8 | 42.2 | 40.0 | 41.6 | 36.4 | 40.6 | 40.1 | 36.4 | 36.7 | 43.3 | 44.8 | 41.6 | 41.4 | 46.8 |

| Lithuania | 15.9 | 14.6 | 29.0 | 36.2 | 37.2 | 39.7 | 38.7 | 40.5 | 42.7 | 40.1 | 39.7 | 34.1 | 35.9 | 46.6 | 44.3 | 39.6 | 37.4 | 38.2 |

| Luxembourg | 7.7 | 15.4 | 16.0 | 20.1 | 19.1 | 22.0 | 23.7 | 22.7 | 21.4 | 20.8 | 23.0 | 21.0 | 22.3 | 24.8 | 24.4 | 25.4 | 25.7 | 26.3 |

| Malta | 62.3 | 61.8 | 67.8 | 67.6 | 69.9 | 65.9 | 65.8 | 61.6 | 63.9 | 57.6 | 50.8 | 45.8 | 40.7 | 53.4 | 57.0 | 55.1 | 49.3 | 47.4 |

| Netherlands | 42.7 | 54.7 | 56.5 | 59.0 | 61.7 | 66.3 | 67.7 | 67.9 | 65.1 | 61.8 | 56.7 | 52.4 | 48.5 | 54.3 | 52.1 | 50.9 | 45.9 | 43.3 |

| Portugal | 68.4 | 75.6 | 83.6 | 96.2 | 111.4 | 129.0 | 131.4 | 132.9 | 129.0 | 130.1 | 125.7 | 122.2 | 116.6 | 135.2 | 127.4 | 123.4 | 107.5 | 94.9 |

| Slovakia | 30.1 | 28.6 | 41.0 | 43.3 | 43.3 | 51.8 | 54.7 | 53.6 | 52.9 | 51.8 | 50.9 | 49.4 | 48.1 | 59.7 | 63.1 | 60.3 | 58.6 | 59.3 |

| Slovenia | 22.8 | 21.8 | 36.0 | 40.8 | 46.6 | 53.6 | 70.0 | 80.3 | 83.2 | 78.5 | 73.6 | 70.4 | 65.6 | 79.8 | 74.7 | 73.5 | 71.4 | 67.0 |

| Spain | 35.6 | 39.7 | 52.7 | 60.1 | 69.5 | 86.3 | 95.8 | 100.7 | 99.2 | 99.0 | 98.3 | 97.6 | 95.5 | 120.0 | 118.4 | 116.1 | 109.8 | 101.8 |

Fiscal policies

[edit].png)

The primary means for fiscal coordination within the EU lies in the Broad Economic Policy Guidelines which are written for every member state, but with particular reference to the 20 current members of the eurozone. These guidelines are not binding, but are intended to represent policy coordination among the EU member states, so as to take into account the linked structures of their economies.

For their mutual assurance and stability of the currency, members of the eurozone have to respect the Stability and Growth Pact, which sets agreed limits on deficits and national debt, with associated sanctions for deviation. The Pact originally set a limit of 3% of GDP for the yearly deficit of all eurozone member states; with fines for any state which exceeded this amount. In 2005, Portugal, Germany, and France had all exceeded this amount, but the Council of Ministers had not voted to fine those states. Subsequently, reforms were adopted to provide more flexibility and ensure that the deficit criteria took into account the economic conditions of the member states, and additional factors.

The Fiscal Compact[78][79] (formally, the Treaty on Stability, Coordination and Governance in the Economic and Monetary Union),[80] is an intergovernmental treaty introduced as a new stricter version of the Stability and Growth Pact, signed on 2 March 2012 by all member states of the European Union (EU), except the Czech Republic, the United Kingdom,[81] and Croatia (subsequently acceding the EU in July 2013). The treaty entered into force on 1 January 2013 for the 16 states which completed ratification prior of this date.[82] As of 1 April 2014, it had been ratified and entered into force for all 25 signatories.

Olivier Blanchard suggests that a fiscal union in the eurozone can mitigate devastating effects of the single currency on the eurozone peripheral countries. But he adds that the currency bloc will not work perfectly even if a fiscal transfer system is built, because, he argues, the fundamental issue about competitiveness adjustment is not tackled. The problem is, since the eurozone peripheral countries do not have their own currencies, they are forced to adjust their economies by decreasing their wages instead of devaluation.[83]

Bailout provisions

[edit]The 2008 financial crisis prompted several reforms in the eurozone. One was a U-turn on the eurozone's bailout policy that led to the creation of a specific fund to assist eurozone states in trouble. The European Financial Stability Facility (EFSF) and the European Financial Stability Mechanism (EFSM) were created in 2010 to provide, alongside the International Monetary Fund (IMF), a system and fund to bail out members. However, the EFSF and EFSM were temporary, small and lacked a basis in the EU treaties. Therefore, it was agreed in 2011 to establish a European Stability Mechanism (ESM) which would be much larger, funded only by eurozone states (not the EU as a whole as the EFSF/EFSM were) and would have a permanent treaty basis. As a result of that its creation involved agreeing an amendment to TEFU Article 136 allowing for the ESM and a new ESM treaty to detail how the ESM would operate. If both are successfully ratified according to schedule, the ESM would be operational by the time the EFSF/EFSM expire in mid-2013.

In February 2016, the UK secured further confirmation that countries that do not use the Euro would not be required to contribute to bailouts for eurozone countries.[84]

Peer review

[edit]In June 2010, a broad agreement was finally reached on a controversial proposal for member states to peer review each other's budgets prior to their presentation to national parliaments. Although showing the entire budget to each other was opposed by Germany, Sweden and the UK, each government would present to their peers and the Commission their estimates for growth, inflation, revenue and expenditure levels six months before they go to national parliaments. If a country was to run a deficit, they would have to justify it to the rest of the EU while countries with a debt more than 60% of GDP would face greater scrutiny.[85]

The plans would apply to all EU members, not just the eurozone, and have to be approved by EU leaders along with proposals for states to face sanctions before they reach the 3% limit in the Stability and Growth Pact. Poland has criticised the idea of withholding regional funding for those who break the deficit limits, as that would only impact the poorer states.[85] In June 2010 France agreed to back Germany's plan for suspending the voting rights of members who breach the rules.[86] In March 2011 was initiated a new reform of the Stability and Growth Pact aiming at straightening the rules by adopting an automatic procedure for imposing of penalties in case of breaches of either the deficit or the debt rules.[87][88]

Criticism

[edit]In 1997, Arnulf Baring expressed concern that the European Monetary Union would make Germans the most hated people in Europe. Baring suspected the possibility that the people in Mediterranean countries would regard Germans and the currency bloc as economic policemen.[89]

In 2001, James Tobin thought that the euro project would not succeed without making drastic changes to European institutions, pointing out the difference between the US and the eurozone.[90] Concerning monetary policies, the system of Federal Reserve banks in the US aims at both growth and reducing unemployment, while the ECB tends to give its first priority to price stability under the Bundesbank's supervision. As the price level of the currency bloc is kept low, the unemployment level of the region has become higher than that of the US since 1982.[90] Concerning fiscal policies, 12% of the US federal budget is used for transfers to states and local governments. The US government does not impose restrictions on state budget policies, whereas the Maastricht Treaty requires each eurozone member country to keep its budget deficit below 3% of its GDP.[90]

In 2008, a study by Alberto Alesina and Vincenzo Galasso found that the adoption of euro promoted market deregulation and market liberalization.[91][92] Furthermore, the euro was also linked to wage moderation, as wage growth slowed down in countries that adopted the new currency.[91] Oliver Hart, who received the Nobel Memorial Prize in Economic Sciences in 2016, criticized the euro, calling it a "mistake" and emphasising his opposition to monetary union since its inception.[93] He also expressed opposition to European integration, arguing that the European Union should instead focus on decentralisation as it has "gone too far in centralising power".[93] In 2018, a study based on DiD methodology found that the adoption of euro produced no systematic growth effects, as no growth-enhancing effects were found when compared to European economies outside the eurozone.[94]

The eurozone has also been criticized for deepening inequality in Europe, particularly between the richest and poorest countries.[95] According to a study by Bertelsmann Stiftung, countries such as Austria and the Netherlands benefited significantly from the common currency, while southern and eastern European members of the eurozone gained very little,[96] and some countries are considered to have suffered adverse effects from adopting the euro.[97] In an article for Politico, Joseph Stiglitz argues that "[t]he result for the eurozone has been slower growth, and especially for the weaker countries within it. The euro was supposed to usher in greater prosperity, which in turn would lead to renewed commitment to European integration. It has done just the opposite — increasing divisions within the EU, especially between creditor and debtor countries."[97] Matthias Matthijs believes that the euro resulted in a "winner-take-all" economy, as national income differences between eurozone members have widened further.[98] He argues that countries such as Austria and Germany have gained from the eurozone at the expense of southern countries like Italy and Spain.[98]

By adopting the euro and abandoning their national currencies, eurozone countries gave up their ability to conduct independent monetary policy; as such, monetary policies used to combat recession, such as monetary stimulus or currency devaluation, are no longer available.[98] During the European debt crisis, several eurozone countries (Greece, Italy, Portugal, Ireland, Spain, and Cyprus) were unable to repay their debt without third-party intervention by the European Central Bank and the International Monetary Fund.[99] In order to grant the bailout, the ECB and the IMF forced the affected countries to adopt strict austerity measures.[98] The European bailouts were largely about shifting exposure from banks onto European taxpayers,[100][101][102] and exacerbated issues such as high unemployment and poverty.[103][104]

In 2019, a study from the Centre for European Policy concluded that while some countries had gained from adopting the euro, several countries were poorer than they would have been had they not adopted it, with France and Italy being particularly affected.[105][106] The publication prompted a large number of reactions, pushing its authors to put out a statement clarifying some points.[107] In 2020, a study from the University of Bonn reached a different conclusion: the adoption of the euro made "some mild losers (France, Germany, Italy, and Portugal) and a clear winner (Ireland)".[108] Both studies used the synthetic control method to estimate what might have happened if the euro hadn't been adopted.

See also

[edit]- Capital Markets Union

- Economic and Monetary Union of the European Union

- European banking union

- Single Euro Payments Area

- List of acronyms associated with the eurozone crisis

- List of people associated with the eurozone crisis

- Sixpack (European Union law)

- Special territories of members of the European Economic Area

- Open Balkan

- Craiova Group

Notes

[edit]- ^ The self-declared Turkish Republic of Northern Cyprus is not recognised by the EU and uses the Turkish lira. However, the euro does circulate widely.[citation needed]

- ^ a b c French Pacific territories use the CFP franc, which is pegged to the euro at the rate of 1 franc to 0.00838 euro.

- ^ The European Union internally uses the code EL for Greece, a deviation from the ISO 3166-1 standard.

- ^ Aruba is part of the Kingdom of the Netherlands, but not of the EU. It uses the Aruban florin, which is pegged to the US dollar at the rate of 1 dollar to 1.79 florins.

- ^ a b Used the Netherlands Antillean guilder until the introduction of the Caribbean guilder on 31 March 2025, after the change was delayed several times. "CBCS wants to have the Caribbean guilder introduced by 2025". Curaçao Chronicle. 16 March 2022. Retrieved 2 August 2022. "Frequent Asked Questions". Centrale Bank Curaçao & Sint Maarten. Retrieved 2 August 2022. Both are pegged to the US dollar at the rate of 1 dollar to 1.79 guilders.

- ^ Uses the US dollar.

- ^ EZ is not assigned, but is reserved for this purpose, in ISO-3166-1.

References

[edit]- ^ Land cover overview by NUTS 2 regions Eurostat

- ^ "Population on 1 January". Eurostat.

- ^ a b "Gross domestic product at market prices (Current prices and per capita)". Eurostat. Retrieved 28 July 2016.

- ^ "ECB Cuts interest rates". 6 March 2025.

- ^ Euro area annual inflation and its main components - estimated Eurostat

- ^ Harmonised unemployment rate by gender – total Eurostat

- ^ "Eurozone Current Account Surplus Falls In December". 18 February 2022.

- ^ "Countries, languages, currencies". Interinstitutional style guide. the EU Publications Office. Retrieved 2 February 2009.The euro area Archived 6 August 2013 at the Wayback Machine, European Central Bank

- ^ "Why France and Germany's political chaos spells trouble for Europe's economy". Fast Company.

- ^ "Agreements on monetary relations (Monaco, San Marino, the Vatican and Andorra)". European Communities. 30 September 2004. Retrieved 12 September 2006.

- ^ "The government announces a contest for the design of the Andorran euros". Andorra Mint. 19 March 2013. Archived from the original on 22 August 2013. Retrieved 26 March 2013.

- ^ "Nouvelles d'Andorre" (in French). 1 February 2013. Archived from the original on 4 October 2013. Retrieved 2 February 2013.

- ^ "The euro outside the euro area". Europa (web portal). Retrieved 15 February 2021.

- ^ A glossary (Archived 14 May 2013 at the Wayback Machine) issued by the ECB defines "euro area", without mention of Monaco, San Marino, or the Vatican.

- ^ "Financial assistance to EU Member States | Fact Sheets on the European Union | European Parliament". www.europarl.europa.eu. 30 April 2024. Retrieved 30 August 2024.

- ^ "European countries don't actually use the Euro!". 9 April 2025.

- ^ "Who can join and when?". European Commission – European Commission. Retrieved 2 December 2020.

- ^ Strupczewski, Jan (4 June 2025). "EU gives Bulgaria green light to adopt euro from start of 2026". Reuters. Retrieved 18 June 2025.

- ^ Fox, Benjamin (1 February 2013). "Dutch PM: Eurozone needs exit clause". EUobserver.com. Retrieved 18 June 2013.

- ^ Cite error: The named reference

population_jan_2024was invoked but never defined (see the help page). - ^ "EU countries and the euro". European Commission. Retrieved 2 December 2022.

- ^ "GNI, Atlas method (current US$) | Data | Table (update date unknown)". Retrieved 2025-05-01.

- ^ a b c d e f g h i j k "COUNCIL DECISION of 3 May 1998 in accordance with Article 109j(4) of the Treaty". Official Journal of the European Union. L (139/30). 11 May 1998. Retrieved 27 October 2014.

- ^ "Council Decision (EU) 2022/1211 of 12 July 2022 on the adoption by Croatia of the euro on 1 January 2023". Official Journal of the European Union. L (187/31). 12 July 2022. Retrieved 2 January 2023.

- ^ "COUNCIL DECISION of 10 July 2007 in accordance with Article 122(2) of the Treaty on the adoption by Cyprus of the single currency on 1 January 2008". Official Journal of the European Union. L (186/29). 18 July 2007. Retrieved 27 October 2014.

- ^ "COUNCIL DECISION of 13 July 2010 in accordance with Article 140(2) of the Treaty on the adoption by Estonia of the euro on 1 January 2011". Official Journal of the European Union. L (196/24). 28 July 2010. Retrieved 27 October 2014.

- ^ "COUNCIL DECISION of 19 June 2000 in accordance with Article 122(2) of the Treaty on the adoption by Greece of the single currency on 1 January 2001". Official Journal of the European Union. L (167/19). 7 July 2000. Retrieved 27 October 2014.

- ^ "COUNCIL DECISION of 9 July 2013 on the adoption by Latvia of the euro on 1 January 2014". Official Journal of the European Union. L (195/24). 18 July 2013. Retrieved 27 October 2014.

- ^ "COUNCIL DECISION of 23 July 2014 on the adoption by Lithuania of the euro on 1 January 2015". Official Journal of the European Union. L (228/29). 31 July 2014. Retrieved 31 December 2014.

- ^ "COUNCIL DECISION of 10 July 2007 in accordance with Article 122(2) of the Treaty on the adoption by Malta of the single currency on 1 January 2008". Official Journal of the European Union. L (186/32). 18 July 2007. Retrieved 27 October 2014.

- ^ "COUNCIL DECISION of 8 July 2008 in accordance with Article 122(2) of the Treaty on the adoption by Slovakia of the single currency on 1 January 2009". Official Journal of the European Union. L (195/24). 24 July 2008. Retrieved 27 October 2014.

- ^ "COUNCIL DECISION of 11 July 2006 in accordance with Article 122(2) of the Treaty on the adoption by Slovenia of the single currency on 1 January 2007". Official Journal of the European Union. L (195/25). 15 July 2006. Retrieved 27 October 2014.

- ^ "Agreements on monetary relations (Monaco, San Marino, the Vatican and Andorra)". European Communities. 30 September 2004. Retrieved 12 September 2006.

- ^ a b "The euro outside the euro area". Europa (web portal). Retrieved 15 February 2021.

- ^ "European Foundation Intelligence Digest". Europeanfoundation.org. Archived from the original on 26 August 2007. Retrieved 30 May 2010.

- ^ "Euro used as legal tender in non-EU nations". International Herald Tribune. 1 January 2007. Archived from the original on 10 December 2008. Retrieved 22 November 2010.

- ^ "The eurozone's 13th member". BBC News. 11 December 2001. Retrieved 30 May 2010.

- ^ "Unilateral Euroization By Iceland Comes With Real Costs And Serious Risks". Lawofemu.info. 15 February 2008. Archived from the original on 14 March 2012. Retrieved 28 February 2015.

- ^ "New EU members to break free from euro duty". Euractiv.com. 13 September 2011. Retrieved 7 September 2013.

- ^ "Sverige sa nej till euron" (in Swedish). Swedish Parliament. 28 August 2013. Archived from the original on 19 September 2017. Retrieved 12 August 2014.

- ^ "Information on ERM II". European Commission. 22 December 2009. Retrieved 16 January 2010.

- ^ "Bulgaria, Croatia take vital step to joining euro". Reuters. 10 July 2020. Retrieved 11 July 2020.

- ^ Dougherty, Carter (1 December 2008). "Buffeted by financial crisis, countries seek euro's shelter". International Herald Tribune. Archived from the original on 22 December 2022. Retrieved 2 December 2008.

- ^ "Czechs, Poles cooler to euro as they watch debt crisis". Reuters. 16 June 2010. Retrieved 18 June 2010.

- ^ "Bulgaria meets criteria to join the euro area on 1 January 2026".

- ^ "Bulgaria prepares to join the euro — but Poland couldn't be less interested". 4 June 2025.

- ^ "Parliament endorses Bulgaria's adoption of the euro | News | European Parliament". 8 July 2025.

- ^ url=https://www.consilium.europa.eu/en/press/press-releases/2025/07/08/bulgaria-ready-to-use-the-euro-from-1-january-2026-council-takes-final-steps/

- ^ "Brussels: No one can leave the euro" Archived 24 December 2020 at the Wayback Machine by Leigh Phillips, EUobserver, 8 September 2011

- ^ a b "The Eurozone crisis – the final stage? Archived 1 July 2018 at the Wayback Machine" by Charles Proctor, Locke Lord, 15 May 2012

- ^ "Withdrawal and Expulsion from the EU and EMU : Some reflections Archived 20 January 2013 at the Wayback Machine" by Phoebus Athanassiou, Principal Legal Counsel with the Directorate-General for Legal Service, ECB, 2009

- ^ "German advisory council calls for exit option in the eurozone" Archived 5 December 2020 at the Wayback Machine by Daniel Tost, EurActiv, 29 July 2015

- ^ a b Text Archived 14 November 2020 at the Wayback Machine of response by Olli Rehn, European Commissioner for Economic and Monetary Affairs and the Euro, on behalf of the European Commission, to question submitted by Claudio Morganti, Member of the European Parliament, 22 June 2012

- ^ Text Archived 17 November 2020 at the Wayback Machine of message by Mario Draghi, ECB, to Claudio Morganti, Member of the European Parliament, 6 November 2012

- ^ Athanassiou, Phoebus (December 2009) Withdrawal and Expulsion from the EU and EMU, Some Reflections Archived 20 January 2013 at the Wayback Machine (PDF), European Central Bank. Retrieved 8 September 2011

- ^ Phillips, Leigh (7 September 2011). "EUobserver / Netherlands: Indebted states must be made 'wards' of the commission or leave euro". Euobserver.com. Retrieved 20 May 2014.

- ^ Dammann, Jens (10 February 2012). "The Right to Leave the Eurozone". U of Texas Law, Public Law Research Paper. 2013. 48 (2). SSRN 2262873.

- ^ Dammann, Jens (26 August 2015). "Paradise Lost: Can the European Union Expel Countries from the Eurozone". Vanderbilt Journal of Transnational Law. 2016. 49 (2). SSRN 2827699.

- ^ Treaty of Lisbon (Provisions specific to member states whose currency is the euro), EurLex Archived 27 March 2009 at the Wayback Machine

- ^ "An economic government for the eurozone?" (PDF). Federal Union. Archived from the original (PDF) on 17 July 2011. Retrieved 26 February 2011.

- ^ Protocols, Official Journal of the European Union

- ^ Elliott, Larry; Wearden, Graeme (17 August 2011). "Merkel and Sarkozy push for greater European co-operation". The Guardian. ISSN 0261-3077. Retrieved 30 August 2024.

- ^ a b Elitsa Vucheva (15 April 2008). "Eurozone countries should speak with one voice, Juncker says". EU Observer. Retrieved 26 February 2011.

- ^ "Commission wants single eurozone seat at IMF plan adopted by end of mandate" Archived 27 December 2017 at the Wayback Machine, Euractiv, 7 December 2017

- ^ "Macron is right — the eurozone needs a finance minister" Archived 7 November 2017 at the Wayback Machine, Financial Times, 28 September 2017

- ^ Europe should have its own economy and finance minister, says EC Archived 27 December 2017 at the Wayback Machine, theguardian 6 December 2017

- ^ "Large number of EU finance ministers want euro zone budget: Dijsselbloem" Archived 27 December 2017 at the Wayback Machine, Reuters, 6 November 2017

- ^ "Spain urges sweeping reforms on eurozone to correct flaws" Archived 27 December 2017 at the Wayback Machine, Financial Times, 14 June 2017

- ^ "Report for Selected Countries and Subjects". www.imf.org.

- ^ Figures from the October 2020 update of the International Monetary Fund's World Economic Outlook Database. [1] Archived 20 January 2021 at the Wayback Machine

- ^ "Annual average rate of change, neither seasonally nor working day adjusted". Archived from the original on 6 October 2022. Retrieved 23 August 2022.

- ^ "Official interest rates". European Central Bank. 8 June 2022. Retrieved 19 June 2022.

- ^ Key ECB interest rates Archived 11 August 2013 at the Wayback Machine, ECB

- ^ "General government gross debt – annual data (table code: teina225)". Eurostat. Retrieved 29 August 2022.

- ^ "Government debt down to 94.2% of GDP in euro area - European Union". Retrieved 12 January 2023.

- ^ Government debt down to 89.9% of GDP in euro area. 22 January 2024. Retrieved 26 January 2024.

- ^ "Government debt at 87.4% of GDP in euro area". 22 April 2025. Retrieved 13 May 2025.

- ^ Nicholas Watt (31 January 2012). "Lib Dems praise David Cameron for EU U-turn". The Guardian. London. Retrieved 5 February 2012.

- ^ "The fiscal compact ready to be signed". European Commission. 31 January 2012. Archived from the original on 22 October 2012. Retrieved 5 February 2012.

- ^ "Referendum to be held on Fiscal Treaty". RTÉ News. 28 February 2012.

- ^ "EU summit: All but two leaders sign fiscal treaty". BBC News. 2 March 2012. Retrieved 2 March 2012.

- ^ "Fiscal compact enters into force 21/12/2012 (Press: 551, Nr: 18019/12)" (PDF). European Council. 21 December 2012. Archived (PDF) from the original on 23 December 2012. Retrieved 21 December 2012.

- ^ Fiscal union will never fix a dysfunctional eurozone, warns ex-IMF chief Blanchard Archived 18 February 2018 at the Wayback Machine Mehreen Khan, The Daily Telegraph (London), 10 October 2015

- ^ "European Council meeting (18 and 19 February 2016) – Conclusions". European Commission. Retrieved 14 May 2016.

- ^ a b EU agrees controversial peer review of national budgets, EU Observer

- ^ Willis, Andrew (15 June 2010) Merkel: Spain can access aid if needed, EU Observer

- ^ "Council reaches agreement on measures to strengthen economic governance" (PDF). Archived (PDF) from the original on 25 August 2011. Retrieved 18 May 2011.

- ^ Jan Strupczewski (15 March 2011). "EU finmins adopt tougher rules against debt, imbalance". Uk.finance.yahoo.com. Yahoo! Finance. Archived from the original on 24 April 2023. Retrieved 18 May 2011.

- ^ This Prediction about the Euro Deserves a ‘Nostradamus Award’ Archived 8 December 2015 at the Wayback Machine W. Richter, Wolf Street, 16 July 2015

- ^ a b c J. Tobin, Policy Opinions, 31 (2001)

- ^ a b Alesina, Alberto; Galasso, Vincenzo; Ardagna, Silvia (May 2008). "The Euro and Structural Reforms" (PDF). NBER Working Paper. 1 (14479). doi:10.3386/w14479.

- ^ Belsie, Laurent (April 2009). "The Euro, Wages, and Prices". NBER. The Digest. Retrieved 26 February 2023.

- ^ a b Rodríguez, Carmen (December 2016). Sam Morgan (ed.). "Nobel economics prize winner: 'The euro was a mistake'". Euractiv. Retrieved 26 February 2023.

- ^ Ioannatos, Petros E. (June 2018). "Has the Euro Promoted Eurozone's Growth?" (PDF). Journal of Economic Integration. 33 (2): 1388–1411. doi:10.11130/jei.2018.33.2.1389. S2CID 158295739.

- ^ Karnitschnig, Matthew (22 April 2020). "The eurozone's problem country: Germany". Politico. Retrieved 27 February 2023.

- ^ Escritt, Thomas (8 May 2019). Gareth Jones (ed.). "Germany, wealthy regions are biggest winners of EU single market: report". Reuters. Retrieved 27 February 2023.

- ^ a b Stiglitz, Joseph (26 June 2018). "How to exit the eurozone". Politico. Retrieved 27 February 2023.

- ^ a b c d Matthijs, Matthias (2016). "The Euro's "Winner-Take-All" Political Economy: Institutional Choices, Policy Drift, and Diverging Patterns of Inequality". Politics & Society. 44 (3). SAGE Publications: 393–422. doi:10.1177/0032329216655317. S2CID 220681429.

- ^ Copelovitch, Mark; Frieden, Jeffry; Walter, Stefanie (14 March 2016). "The Political Economy of the Euro Crisis". Comparative Political Studies. 49 (7): 811–840. doi:10.1177/0010414016633227. ISSN 0010-4140. S2CID 18181290.

- ^ Featherstone, Kevin (23 March 2012). "Are the European banks saving Greece or saving themselves?". Greece@LSE. LSE. Retrieved 27 March 2012.

- ^ "Greek aid will go to the banks". Die Gazette. Presseurop. 9 March 2012. Archived from the original on 3 December 2012. Retrieved 12 March 2012.

- ^ Whittaker, John (2011). "Eurosystem debts, Greece, and the role of banknotes" (PDF). Lancaster University Management School. Archived from the original (PDF) on 25 November 2011. Retrieved 2 April 2012.

- ^ Cavero, Gonzalo; Cortés, Irene Martín (September 2013). "The true cost of austerity and inequality: Greece Case Study" (PDF). Oxfam Case Study. ISBN 9781780774046.

- ^ Coppola, Frances (31 August 2018). "The Terrible Human Cost Of Greece's Bailouts". Forbes. Archived from the original on 9 August 2022. Retrieved 27 February 2023.

- ^ Nicole Ng, "CEP study: Germans gain most from euro introduction", Deutsche Welle, 25 February 2019, accessed 05/03/19.

- ^ Gasparotti, Alessandro; Kullas, Matthias (February 2019). "20 Years of the Euro: Winners and Losers" (PDF). cepStudy. Archived (PDF) from the original on 19 November 2019.

- ^ "Statement on reactions to the study 20 years of euro". Centrum für europäische Politik. 19 December 2022. Archived from the original on 31 January 2023.

- ^ Gabriel, Ricardo Duque; Pessoa, Ana Sofia (1 December 2020). "Adopting the Euro: A Synthetic Control Approach". SSRN. doi:10.2139/ssrn.3563044. S2CID 219969338. SSRN 3563044.

External links

[edit]- Eurozone official portal (archived 9 June 2012)

- European Central Bank

- European Commission – Economic and Financial Affairs – Eurozone

Euro topics | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| General | |||||||||

| Administration | |||||||||

| Fiscal provisions | |||||||||

| Economy | |||||||||

| International status | |||||||||

| Denominations |

| ||||||||

| Coins by country with minting rights |

| ||||||||

| Adoption by country |

| ||||||||

| |||||||||

| History |

| ||||||||

| International | |

|---|---|

| National | |

| Other | |

Eurozone

View on GrokipediaEstablishment and Historical Development

Founding Treaties and Initial Launch

The Treaty on European Union, signed on 7 February 1992 in Maastricht, Netherlands, and entering into force on 1 November 1993, established the European Union and defined the framework for Economic and Monetary Union (EMU).[9][10] This treaty amended prior agreements, including the Treaty establishing the European Economic Community, and introduced convergence criteria—such as price stability, sound public finances, exchange rate stability, and convergence of long-term interest rates—that member states needed to satisfy for participation in the final stage of EMU.[11] The Maastricht Treaty also created the European Central Bank (ECB) and the European Monetary Institute as precursors to centralized monetary policy.[12] EMU progressed in three stages as outlined in the treaty. Stage One, from 1 July 1990 to 31 December 1993, focused on liberalizing capital movements, reducing exchange rate fluctuations, and enhancing economic policy coordination without a common currency.[13] Stage Two, from 1 January 1994 to 31 December 1998, involved the establishment of the European Monetary Institute to oversee monetary policy convergence and prepare for the single currency, while prohibiting monetary financing of public deficits.[14] During this period, the European Council assessed member states' readiness based on the convergence criteria. Stage Three commenced on 1 January 1999, marking the irrevocable conversion of national currencies to the euro for eleven initial member states: Belgium, Germany, Ireland, Spain, France, Italy, Luxembourg, the Netherlands, Austria, Portugal, and Finland.[15][16] The euro replaced the European Currency Unit (ECU) as the unit of account, enabling monetary union with the ECB assuming responsibility for setting interest rates and conducting foreign exchange operations, while national currencies remained in circulation for cash transactions until 2002.[17] Greece joined as the twelfth member on 1 January 2001 after meeting the criteria, preceding the physical introduction of euro notes and coins on 1 January 2002.[18] The United Kingdom and Denmark secured opt-outs from participation, allowing them to retain their national currencies indefinitely.[11]Early Enlargements and Opt-Outs

The Eurozone initially comprised 11 member states—Austria, Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal, and Spain—that satisfied the convergence criteria outlined in the Maastricht Treaty and adopted the euro for electronic transactions on 1 January 1999.[1] These countries transitioned to euro banknotes and coins as legal tender on 1 January 2002, replacing national currencies at fixed conversion rates.[16] Greece, having achieved the required criteria by late 2000 despite prior shortfalls in budget deficit and debt levels, became the 12th member on 1 January 2001, participating in the physical currency changeover a year later.[19] Subsequent revelations indicated that Greece had employed derivative swaps and other financial engineering to temporarily mask its fiscal deficits below the 3% GDP threshold during the assessment period, a practice later criticized for undermining the integrity of entry requirements.[20] Under the Maastricht Treaty of 1992, Denmark and the United Kingdom negotiated permanent opt-outs from the third stage of Economic and Monetary Union, exempting them from the obligation to adopt the euro despite EU membership. Denmark's exemption stemmed from a 1992 referendum rejecting the treaty, leading to the Edinburgh Agreement that preserved the opt-out while allowing participation in other EU policies; the country maintains the krone, pegged to the euro via the Exchange Rate Mechanism II.[21] The UK's opt-out became moot following its 2020 departure from the EU via Brexit. Sweden, which acceded to the EU in 1995 after the treaty's ratification, lacks a formal opt-out but has effectively deferred euro adoption since a 2003 referendum rejected it by 55.9%, with subsequent governments avoiding fulfillment of convergence criteria such as central bank independence and exchange rate stability.[22] The first enlargements beyond the founding group followed the EU's 2004 expansion, which added ten new members, several of whom pursued euro adoption. Slovenia, the smallest and first post-2004 entrant, met all convergence criteria and joined the Eurozone on 1 January 2007, converting from the tolar at a fixed rate of 239.640 tolar per euro.[23] Cyprus and Malta followed on 1 January 2008, increasing membership to 15; both satisfied inflation, deficit, debt, and interest rate benchmarks, with Cyprus transitioning from the pound and Malta from the lira.[24] These accessions emphasized adherence to the Stability and Growth Pact's fiscal rules, though early monitoring highlighted vulnerabilities in smaller economies' banking sectors and external dependencies.Major Crises and Institutional Responses

The European sovereign debt crisis emerged in late 2009 when Greece disclosed its budget deficit had reached 12.7% of GDP, far exceeding the Eurozone's 3% Stability and Growth Pact limit, revealing years of fiscal misrepresentation and high public debt levels around 127% of GDP. This triggered market panic, with Greek bond yields surging above 7% by early 2010, signaling default risk and prompting contagion to other peripheral economies like Ireland, Portugal, Spain, and Italy, where banking sector weaknesses and housing bubbles amplified vulnerabilities.[25] By mid-2012, Eurozone-wide GDP had contracted, unemployment peaked at 12% area-wide, and fears of euro disintegration intensified as interbank lending froze and capital flight from southern members accelerated.[26] Institutional responses began with ad hoc measures, including the European Commission's coordination of bilateral loans to Greece totaling €110 billion in May 2010, supported by IMF funding under a troika framework imposing structural reforms and austerity to restore fiscal sustainability. The temporary European Financial Stability Facility (EFSF) was established in June 2010 with €440 billion in lending capacity, later evolving into the permanent European Stability Mechanism (ESM) in October 2012, providing bailout funds conditional on macroeconomic adjustment programs for Ireland (€67.5 billion in 2010), Portugal (€78 billion in 2011), and others.[27] The European Central Bank (ECB) intervened decisively by expanding liquidity operations, including long-term refinancing operations (LTROs) disbursing over €1 trillion to banks in late 2011 and early 2012 to prevent credit crunches, while purchasing sovereign bonds on secondary markets under the Securities Markets Programme (SMP) starting in May 2010, totaling €218 billion by 2012.[26] A pivotal ECB action came in July 2012 when President Mario Draghi pledged to do "whatever it takes" to preserve the euro, leading to the outright monetary transactions (OMT) program, which promised conditional unlimited bond purchases for countries under ESM programs, restoring market confidence and lowering peripheral yields without significant actual purchases. Complementary reforms included the 2012 Treaty on Stability, Coordination and Governance (Fiscal Compact), ratified by 25 EU states including all Eurozone members, enforcing balanced budgets and automatic correction mechanisms.[27] The crisis also spurred the Banking Union, with the ECB assuming supervisory roles over major banks via the Single Supervisory Mechanism in November 2014, aiming to sever sovereign-bank loops exposed during the turmoil.[28] Subsequent shocks tested these mechanisms. The COVID-19 pandemic in 2020 prompted the ECB's €1.35 trillion Pandemic Emergency Purchase Programme (PEPP) from March 2020 to March 2022, alongside targeted longer-term refinancing operations, while the EU issued common debt through NextGenerationEU, raising €806.9 billion (in 2021 prices) for grants and loans to support recovery without violating no-bailout clauses.[29] The 2022 energy crisis, triggered by Russia's invasion of Ukraine, drove inflation to 10.6% Eurozone-wide by October 2022 and recession risks, eliciting ECB rate hikes from negative territory to 4.5% by late 2023 and activation of the Transmission Protection Instrument (TPI) in July 2022 to counter unwarranted yield fragmentation.[30] These responses highlighted evolving fiscal-monetary coordination, though debates persist on their sustainability given persistent debt ratios exceeding 90% of GDP in several members as of 2023.[26]Membership and Territorial Scope

Current Member States

The Eurozone, officially known as the euro area, consists of 20 member states as of October 2025, all of which are European Union countries that have adopted the euro as their official currency.[31] These states participate in the European Central Bank's monetary policy and use the euro for all transactions, having phased out their previous national currencies on specified adoption dates.[32] The member states, listed alphabetically with their euro adoption dates, are presented in the following table:| Country | Adoption Date |

|---|---|

| Austria | 1 January 1999 |

| Belgium | 1 January 1999 |

| Croatia | 1 January 2023 |

| Cyprus | 1 January 2008 |

| Estonia | 1 January 2011 |

| Finland | 1 January 1999 |

| France | 1 January 1999 |

| Germany | 1 January 1999 |

| Greece | 1 January 2001 |

| Ireland | 1 January 1999 |

| Italy | 1 January 1999 |

| Latvia | 1 January 2014 |

| Lithuania | 1 January 2015 |

| Luxembourg | 1 January 1999 |

| Malta | 1 January 2008 |

| Netherlands | 1 January 1999 |

| Portugal | 1 January 1999 |

| Slovakia | 1 January 2009 |

| Slovenia | 1 January 2007 |

| Spain | 1 January 1999 |

Territories and Non-Standard Inclusions

The Eurozone includes overseas territories and dependencies of member states where the euro functions as legal tender, reflecting their administrative integration with the parent country despite geographical distance from Europe. For France, the overseas departments and regions—Guadeloupe, Martinique, French Guiana, Réunion, and Mayotte—are classified as outermost regions of the EU, fully participating in the single market and monetary union since the euro's introduction in 1999 for electronic transactions and 2002 for cash. These territories, with a combined population exceeding 2.5 million as of 2023, contribute to France's Eurozone statistics on GDP and inflation, though their economies rely heavily on tourism, agriculture, and subsidies from the metropole. Similarly, Portugal's autonomous regions of the Azores and Madeira, and Spain's Canary Islands, operate within the Eurozone framework as EU outermost regions, adopting the euro upon its launch and benefiting from special fiscal adjustments under EU treaties to address their insular and remote status.[34][16] Certain territories exhibit non-standard status due to partial exclusions from EU competencies while still using the euro as integral parts of member states. Spain's autonomous cities of Ceuta and Melilla, located on the North African coast, have employed the euro since 2002 as Spanish sovereign territory, with residents holding EU citizenship; however, they fall outside the EU's customs territory, common commercial policy, and value-added tax regime per Spain's accession protocol, subjecting them to distinct trade arrangements with Morocco and tariff-free access to the EU for most goods. France's collectivity of Saint Pierre and Miquelon, situated off Canada's coast, transitioned to the euro on 1 January 2002, replacing a local franc pegged to the French currency, despite its designation as an overseas country and territory (OCT) excluded from the EU's internal market; its approximately 6,000 residents use euro notes and coins issued by France, with the territory maintaining close economic ties to North America. Similarly, Saint-Barthélemy, a French overseas collectivity in the Caribbean with around 10,000 residents, adopted the euro in 2002 as an OCT outside the EU proper, using euro currency issued by France. These smaller French OCTs are not included in official Eurozone population figures, which total approximately 353 million; their combined population under 20,000 is negligible in this context.[35][36] Non-EU microstates represent further non-standard inclusions through bilateral or multilateral monetary agreements enabling euro usage under ECB supervision, distinct from unilateral adopters. Monaco has used the euro since 1 January 2002 via a 2001 agreement with France, permitting limited coin minting; San Marino formalized its adoption in 2002 through agreements with Italy and the EU, issuing themed euro coins annually; Vatican City followed suit in 2004 with an EU accord, renowned for its collector euro issues; and Andorra entered a 2011 monetary agreement with the EU, officially adopting the euro on 1 April 2012 after decades of dual-currency use with the Spanish peseta and French franc. These arrangements, covering populations under 100,000 combined, ensure alignment with ECB monetary policy without full EU membership, including rights to produce commemorative coins subject to approval. In contrast, unilateral users such as Montenegro (since 2002) and Kosovo (de facto since 2002) circulate euro cash without formal agreements or minting privileges, operating outside official Eurozone governance.[37][16]Usage Outside EU Membership

The euro is used as legal tender in several non-EU sovereign entities through formal monetary agreements with the European Union, which grant these microstates the right to adopt the currency and, in limited cases, issue their own euro-denominated coins. Andorra formalized its use of the euro via a 2011 monetary agreement with the EU, following informal adoption since 2002, allowing it to mint collector coins but not circulating currency.[37] Monaco, San Marino, and Vatican City similarly operate under agreements dating to 2001–2012, integrated through ties to France and Italy respectively; these entities have adopted the euro since its launch in 2002 and possess limited coining rights, with Vatican City notably issuing euros featuring papal imagery under a special arrangement.[37] These agreements enable participation in the euro payments system but exclude these states from Eurozone decision-making bodies like the European Central Bank (ECB), meaning they lack influence over monetary policy while benefiting from the currency's stability.[37] In contrast, Montenegro and Kosovo employ the euro as a de facto currency without EU agreements, having unilaterally adopted it in 2002 amid post-Yugoslav transitions to replace unstable local tender.[37] Montenegro, with a population of approximately 620,000, declared the euro its sole legal tender by law in 2002, facilitating trade with Eurozone neighbors but exposing it to risks like inability to conduct independent monetary policy or access ECB liquidity during crises, as evidenced by its reliance on imported euros during the 2008–2009 financial downturn.[37] Kosovo, a partially recognized state with around 1.8 million residents, followed suit informally, using the euro for over 90% of transactions despite lacking formal recognition from the ECB; this has stabilized inflation but complicated fiscal autonomy, with no seigniorage revenue and vulnerability to external euro supply fluctuations.[37] Neither entity can mint euros, leading to dependence on cross-border inflows, and efforts to formalize status—such as Montenegro's EU accession push aiming for euro integration by 2028—remain stalled by broader membership hurdles.[37] The British Sovereign Base Areas (SBAs) of Akrotiri and Dhekelia on Cyprus, overseas territories under UK sovereignty comprising about 254 square kilometers and home to roughly 15,000 residents excluding military personnel, also use the euro as legal tender despite non-EU status post-Brexit.[38] Established in 1960 as military enclaves within EU-member Cyprus, the SBAs adopted the euro upon Cyprus's 2008 entry into the Eurozone, with transactions conducted in euros alongside British forces' use of pounds; this arrangement reflects geographic and economic integration rather than formal agreement, permitting euro circulation without UK or EU policy input.[38] Overall, these non-EU usages total under 3 million people and represent marginal euro circulation volume—estimated at less than 0.1% of the ECB's total—highlighting the currency's appeal for small economies seeking stability without full institutional alignment.[37]Prospects for Future Enlargement

As of October 2025, the Eurozone comprises 20 member states, with Bulgaria poised to become the 21st upon adopting the euro on January 1, 2026, following confirmation of its compliance with the Maastricht convergence criteria by the European Commission and European Central Bank in June 2025.[39] To join, non-euro EU states must satisfy requirements including price stability (inflation not exceeding 1.5 percentage points above the three best-performing EU states), sound public finances (budget deficit below 3% of GDP and public debt under 60% of GDP or declining toward it), exchange rate stability via at least two years in ERM II, and convergence of long-term interest rates (within 2 percentage points of the three best-performing states).[33] Political commitment and national legislative alignment are also prerequisites, though historical precedents like Greece's 2001 entry—despite marginal compliance—highlight risks of incomplete convergence leading to later imbalances.[39] Bulgaria entered ERM II in July 2020 and has maintained its currency board peg to the euro since 1997, facilitating steady progress. In its June 2025 convergence assessment, the ECB noted Bulgaria's 12-month average inflation at 2.1% (below the reference value of 2.6%), budget deficit at 2.8% of GDP, and public debt at 24.1% of GDP, all meeting criteria; interest rates converged at 2.3% and exchange rates showed no tensions.[39] Legislative approvals followed in July 2025, with the lev's fixed rate set at 1.95583:1 euro, enabling a smooth transition despite public concerns over potential price hikes.[33] Romania, which joined ERM II in 2024, faces delays due to persistent inflation exceeding 5% in 2024 assessments and public debt rising to 52.3% of GDP amid fiscal pressures. The European Commission reported in June 2024 that while exchange rate and interest rate criteria were broadly met, price stability and fiscal sustainability required further reforms, with no firm adoption date set; projections suggest possible entry no earlier than 2030 if structural deficits persist. Among remaining non-euro EU states, Denmark holds a permanent treaty opt-out and maintains no adoption plans, citing sovereignty preferences despite meeting economic criteria. Sweden lacks an opt-out but has indefinitely postponed entry since a 2003 referendum rejected it, with current policy requiring parliamentary approval absent, and inflation divergence noted in 2024 reviews. Poland, Czechia, and Hungary show varying political hurdles: Poland's government has expressed intent to target eventual adoption but cites high public debt (49.5% of GDP in 2024) and inflation as barriers, with no timeline; Czechia and Hungary similarly lag on fiscal convergence and exhibit euroskeptic resistance, potentially delaying entry beyond 2030 without policy shifts.| Country | ERM II Entry | Key Barriers | Projected Timeline |

|---|---|---|---|

| Bulgaria | July 2020 | None (criteria met) | January 2026[39] |

| Romania | 2024 | Inflation >5%, rising debt | 2030 or later |

| Sweden | None | No political mandate post-2003 referendum | Indefinite |

| Poland | None | Fiscal deficits, political debate | Post-2030 possible |

| Czechia | None | Exchange rate volatility | Post-2030 possible |

| Hungary | None | Euroskeptic government, deficits | Indefinite |

| Denmark | None (opt-out) | Treaty exemption | None planned |

Monetary and Fiscal Institutions

European Central Bank and Monetary Policy

The European Central Bank (ECB) was established on June 1, 1998, as the central institution responsible for conducting the monetary policy of the euro area, following the institutional provisions of the Maastricht Treaty and the launch of Economic and Monetary Union (EMU) stage three.[40] Its primary mandate, enshrined in Article 127(1) of the Treaty on the Functioning of the European Union, is to maintain price stability, defined as achieving a symmetric inflation rate of 2% over the medium term, measured by the Harmonised Index of Consumer Prices (HICP).[41] [42] Without prejudice to this objective, the ECB supports the general economic policies of the European Union, promoting sustainable growth and employment, though price stability remains hierarchically primary to avoid fiscal-monetary policy conflicts.[41] The ECB operates within the Eurosystem, comprising the ECB and the national central banks of euro area member states, with monetary policy decisions taken by the Governing Council, which includes the ECB Executive Board and the governors of national central banks.[43] This structure ensures a supranational approach to policy, independent from national governments and EU institutions, with the ECB's capital subscribed by national central banks to insulate it from direct fiscal influence.[43] The ECB's legal independence, prohibiting monetary financing of public deficits and requiring policy justification through transparent communication, has been credited with anchoring inflation expectations, though critics argue that prolonged low-interest environments post-2008 encouraged fiscal indiscipline in high-debt states without corresponding structural reforms. [44] Standard monetary policy implementation relies on a framework of interest rate corridors, open market operations, standing facilities, and minimum reserve requirements to steer short-term money market rates and influence broader economic conditions.[45] The key policy rate, the main refinancing operations rate, guides liquidity provision through weekly auctions, while standing facilities provide overnight access to funds at penalty rates to bound market volatility.[45] Forward guidance on future policy paths complements these tools, signaling intent to maintain accommodative conditions as needed to meet the inflation target.[46] In response to the 2008 global financial crisis and the ensuing sovereign debt crisis, the ECB deployed unconventional measures, including enhanced liquidity provision via longer-term refinancing operations and, from January 2015, large-scale asset purchase programs (quantitative easing, or QE) totaling over €2.6 trillion by 2018, aimed at lowering long-term yields and easing credit conditions.[47] [48] These interventions, including targeted longer-term refinancing operations (TLTROs) and negative deposit facility rates introduced in 2014, supported bank lending and stabilized markets but raised concerns over balance sheet expansion—peaking at €8.8 trillion by 2022—and potential distortions to asset prices without addressing underlying competitiveness divergences across member states.[46] [49] Empirical analyses indicate QE reduced sovereign bond spreads by 50-100 basis points in stressed economies, though transmission varied by country due to banking sector fragmentation.[50] Facing inflation surges exceeding 10% in 2022 driven by energy shocks and supply disruptions, the ECB reversed course with aggressive rate hikes, lifting the deposit facility rate from -0.5% in July 2022 to 4% by September 2023, marking the fastest tightening cycle in its history to restore price stability.[51] By July 2025, headline inflation had moderated toward the 2% target, prompting stabilization of rates amid balanced risks, with projections indicating sustained convergence barring renewed shocks.[52] [42] The 2025 strategy review reaffirmed the symmetric 2% target while emphasizing flexibility in response to volatile geopolitical and supply-side factors, underscoring the ECB's commitment to data-dependent decisions over rigid rules.[42] Despite effectiveness in curbing inflation, debates persist on whether one-size-fits-all policy adequately accommodates divergent national cycles, with evidence of uneven transmission in smaller open economies.[53]Eurogroup and Intergovernmental Coordination